A Notice of Non-Renewal Due to Material Misrepresentation is a legal notification issued when a policyholder provides false information that impacts risk assessment. Discover how these inaccuracies lead to policy termination and learn the essential steps for formal communication. Understanding these requirements ensures compliance and clarity for all parties involved. Below are some ready to use templates.

Image cover: Formal Notice of Lease Non-Renewal: Material Misrepresentation Template

Letter Samples List

- Notice of Non-Renewal Due to Material Misrepresentation Letter

- Notice of Cancellation for Non-Payment of Premium Letter

- Notice of Policy Reinstatement Letter

- Notice of Claim Denial Letter

- Acknowledgment of Claim Receipt Letter

- Request for Additional Underwriting Information Letter

- Notice of Premium Rate Increase Letter

- Policy Renewal Confirmation Letter

- Notice of Mid-Term Policy Cancellation Letter

- Lapse in Coverage Notification Letter

- Reservation of Rights Letter

- Notice of Change in Policy Terms Letter

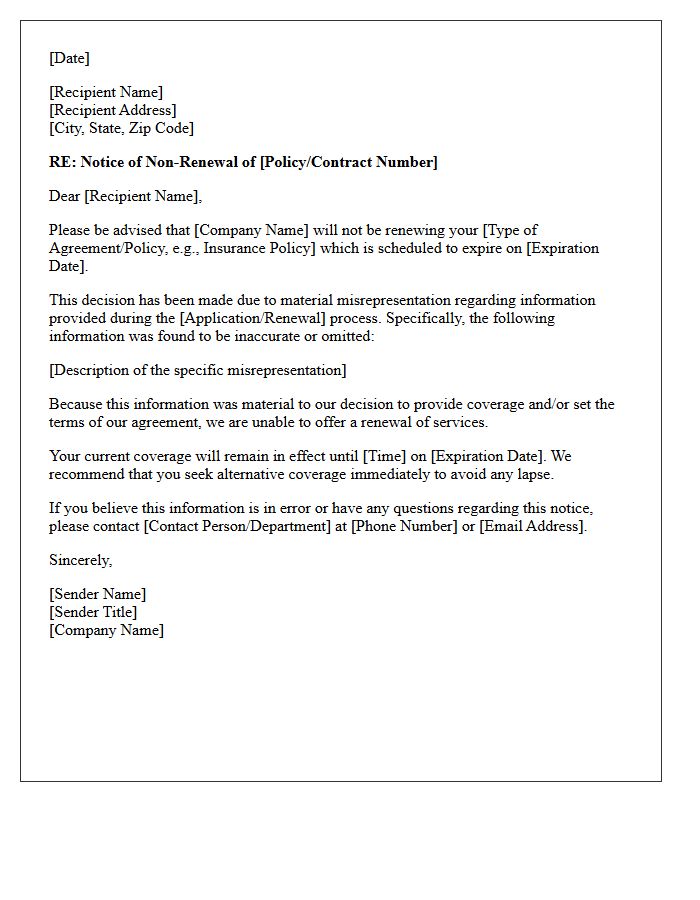

Notice of Non-Renewal Due to Material Misrepresentation Letter

A Notice of Non-Renewal Due to Material Misrepresentation is a legal document informing a policyholder that their coverage will end because they provided false or omitted information on an insurance application. This material misrepresentation occurs when a client fails to disclose facts that would have altered the insurer's original decision to offer coverage or set specific premiums. Receiving this letter indicates that the insurance company has discovered the dishonesty or error, leading to a permanent cancellation of the policy at the end of the current term to mitigate further risk.

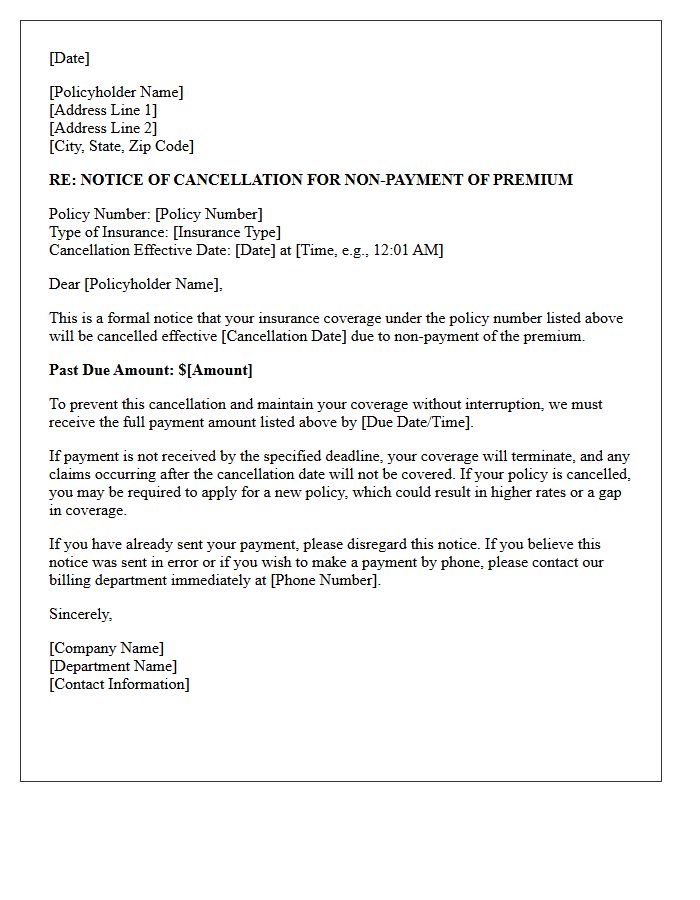

Notice of Cancellation for Non-Payment of Premium Letter

A Notice of Cancellation for Non-Payment of Premium is a formal legal document issued by an insurance carrier when a policyholder fails to pay their bill. This highlighted notification serves as a final warning that coverage will terminate on a specific date unless the outstanding balance is settled. It is crucial to act immediately during the grace period to avoid a lapse in coverage, which can lead to higher future rates, financial liability, and legal penalties. Always verify the termination date to ensure continuous protection for your assets.

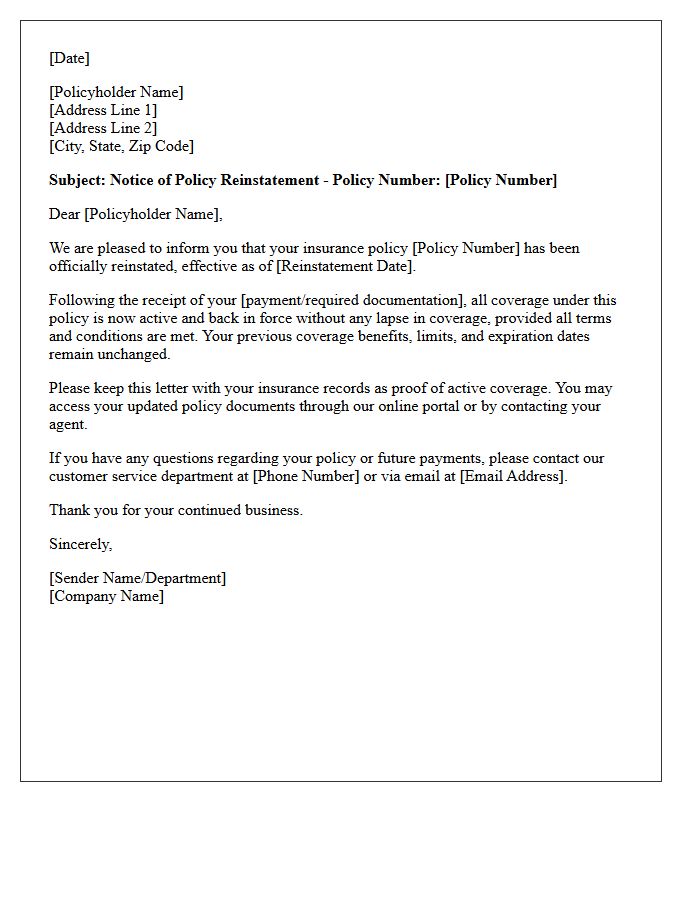

Notice of Policy Reinstatement Letter

A Notice of Policy Reinstatement Letter confirms that your previously canceled or lapsed insurance coverage is active again. It is essential to verify the effective date of restoration to ensure no gaps in protection exist. This formal document typically outlines any outstanding premiums paid and confirms that all contractual terms remain unchanged. Always keep this letter as legal proof of continuous coverage, as it protects your financial interests and ensures your policy benefits are fully restored following a payment or compliance issue.

Notice of Claim Denial Letter

A Notice of Claim Denial Letter is a formal document issued by an insurance company or government agency stating that your request for benefits has been rejected. It is crucial to review the specific reasons for denial listed in the letter to understand which policy terms or legal requirements were not met. This notice also outlines your right to an administrative appeal, including strict filing deadlines you must follow to challenge the decision. Acting quickly and providing additional evidence is essential for a successful reconsideration of your claim.

Acknowledgment of Claim Receipt Letter

An Acknowledgment of Claim Receipt Letter serves as formal confirmation that an insurance provider or company has officially received your filed claim. This essential document establishes a documented timeline for the processing period and typically includes a unique claim number for tracking. It provides the contact details of the assigned adjuster and may list additional required documentation needed to proceed. Retaining this letter is crucial for your records, as it acts as legal proof that the notification process has begun, ensuring accountability throughout the evaluation phase.

Request for Additional Underwriting Information Letter

A Request for Additional Underwriting Information Letter is a formal inquiry from an insurer seeking clarification to evaluate your risk profile accurately. This document typically requests missing financial data, medical records, or specific details regarding potential liabilities. It is the most critical step in the risk assessment process, as your response directly influences policy approval and premium costs. Providing prompt and precise documentation ensures transparency, helping underwriters determine the appropriate coverage terms while preventing delays or potential application denials during the evaluation phase.

Notice of Premium Rate Increase Letter

A Notice of Premium Rate Increase Letter is a formal document from your insurance provider announcing a hike in your policy costs. It is crucial to review the effective date and the specific reason for the adjustment, such as inflation, increased claims, or updated risk assessments. Always compare the new rate against your current coverage limits. To manage costs, you should evaluate alternative plans, increase your deductible, or check for available discounts before the renewal deadline to ensure your insurance remains affordable and comprehensive.

Policy Renewal Confirmation Letter

A Policy Renewal Confirmation Letter is a formal document verifying the extension of your insurance coverage. It serves as legal proof that your protection remains active for a new term. Key details include the updated premium amount, coverage limits, and effective dates. Always review this letter to ensure all personal information is accurate and that no unintended changes have been made to your policy terms. Retain this confirmation for your records to avoid any potential gaps in liability or future claims disputes.

Notice of Mid-Term Policy Cancellation Letter

A Notice of Mid-Term Policy Cancellation is a formal document issued by an insurer to terminate coverage before the scheduled expiration date. It is crucial to understand that companies must provide a specific notice period, typically 30 days, as required by state laws. Common reasons for mid-term termination include non-payment of premiums, material misrepresentation, or a significant increase in risk. Receiving this letter requires immediate action to secure alternative protection and avoid a coverage gap, which could lead to legal penalties or financial loss.

Lapse in Coverage Notification Letter

A Lapse in Coverage Notification Letter is a formal notice from an insurance provider stating that your policy is no longer active. This document typically results from unpaid premiums or a failure to renew, leaving you without financial protection. It is crucial to address this immediately to avoid legal penalties, higher future rates, or out-of-pocket costs for claims. To resolve the issue, contact your insurer to discuss reinstatement options or a grace period, as continuous coverage is essential for maintaining your driving privileges and financial security.

Reservation of Rights Letter

A Reservation of Rights Letter is a formal notice sent by an insurance provider to a policyholder. It indicates that while the insurer is investigating a claim or providing a defense, they maintain the right to deny coverage later based on policy exclusions. Receiving this document does not mean your claim is rejected, but it signals potential legal coverage disputes. It is essential to review the specific clauses cited, as you may need independent counsel to protect your interests and ensure the insurer fulfills its contractual obligations under the policy terms.

Notice of Change in Policy Terms Letter

A Notice of Change in Policy Terms is a formal document sent by insurers to inform policyholders of modifications to their existing coverage. It is crucial to review these updates immediately, as they often detail reductions in benefits, premium increases, or new exclusions. These changes typically take effect upon renewal. Understanding the specific amendments ensures you maintain adequate protection and allows you to seek alternative options if the new terms no longer meet your financial or legal requirements. Always keep this notice with your original policy documentation for future reference.

What is a Notice of Non-Renewal Due to Material Misrepresentation?

A Notice of Non-Renewal due to material misrepresentation is a formal legal notification from an insurance provider stating that they will not extend coverage past the current policy expiration date because the policyholder provided false, incomplete, or misleading information during the application or claims process.

What counts as a "Material Misrepresentation" on an insurance policy?

Material misrepresentation refers to any false statement or omitted fact that is significant enough to have altered the insurer's decision to issue the policy, the premium rate charged, or the terms of coverage. Common examples include failing to disclose previous accidents, undisclosed residents in a household, or lying about how a property is used.

Can I appeal a non-renewal notice for misrepresentation?

Yes, most states allow policyholders to contest a non-renewal. To appeal, you must provide evidence that the information in question was accurate at the time of filing, that the error was clerical rather than intentional, or that the misrepresented fact was not "material" to the risk being insured.

How does a non-renewal for misrepresentation affect my ability to get future insurance?

A non-renewal for material misrepresentation is often flagged in industry databases like CLUE or LexisNexis. This can make it difficult to secure standard coverage, as other insurers may view you as a high-risk client, potentially leading to higher premiums or the need to seek coverage through a surplus lines or high-risk insurance pool.

What is the difference between policy cancellation and non-renewal for misrepresentation?

Cancellation occurs mid-term and terminates coverage immediately or within a short grace period, often requiring the insurer to prove fraud. Non-renewal occurs at the end of the policy term, where the insurer simply chooses not to "re-up" the contract; however, citing material misrepresentation as the reason still carries significant legal and financial implications for the insured.

Comments