A Notice of Non-Renewal Due to Unacceptable Driving Record is a formal document issued by insurance companies when a policyholder's motor vehicle report reveals excessive violations or accidents. This notice explains that coverage will terminate at the end of the current term because the risk no longer meets underwriting guidelines. To help you navigate this process, below are some ready to use template.

Image cover: Notice of Non-Renewal: Unacceptable Driving Record Templates and Guide

Letter Samples List

- Standard Auto Insurance Non-Renewal Letter

- Notice of Non-Renewal Letter for Multiple Traffic Violations

- DUI Conviction Policy Non-Renewal Letter

- Excessive At-Fault Accidents Non-Renewal Letter

- Commercial Fleet Driver Unacceptable Record Non-Renewal Letter

- License Suspension Insurance Non-Renewal Letter

- High-Risk Driver Classification Non-Renewal Letter

- DMV Points Accumulation Policy Non-Renewal Letter

- Severe Driving Infraction Non-Renewal Letter

- Notice of Non-Renewal Letter Due to Excessive Speeding Citations

- Unacceptable Motor Vehicle Report Non-Renewal Letter

- Final Notice of Policy Expiration Letter for Poor Driving History

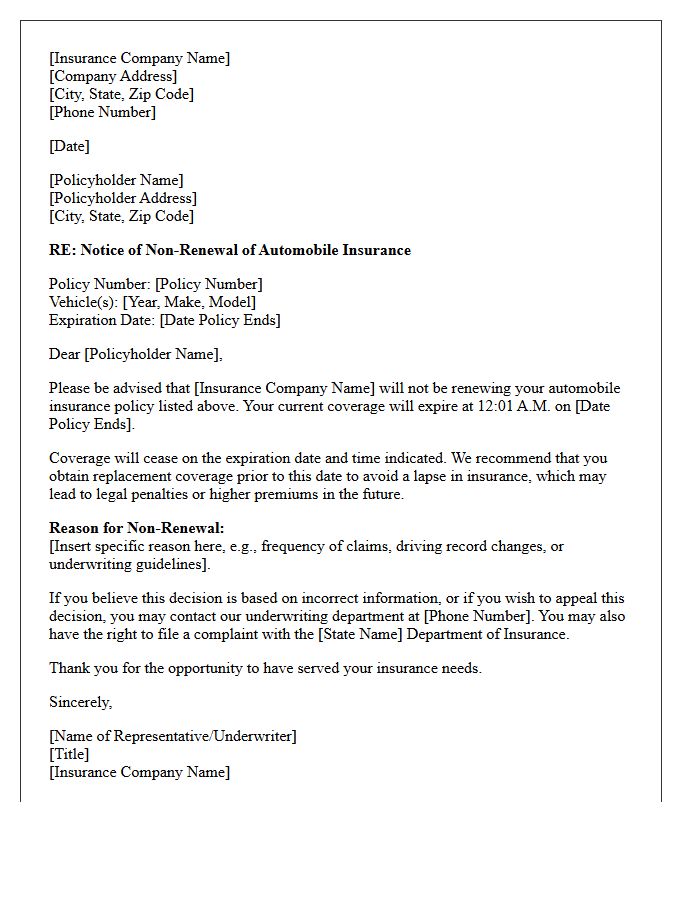

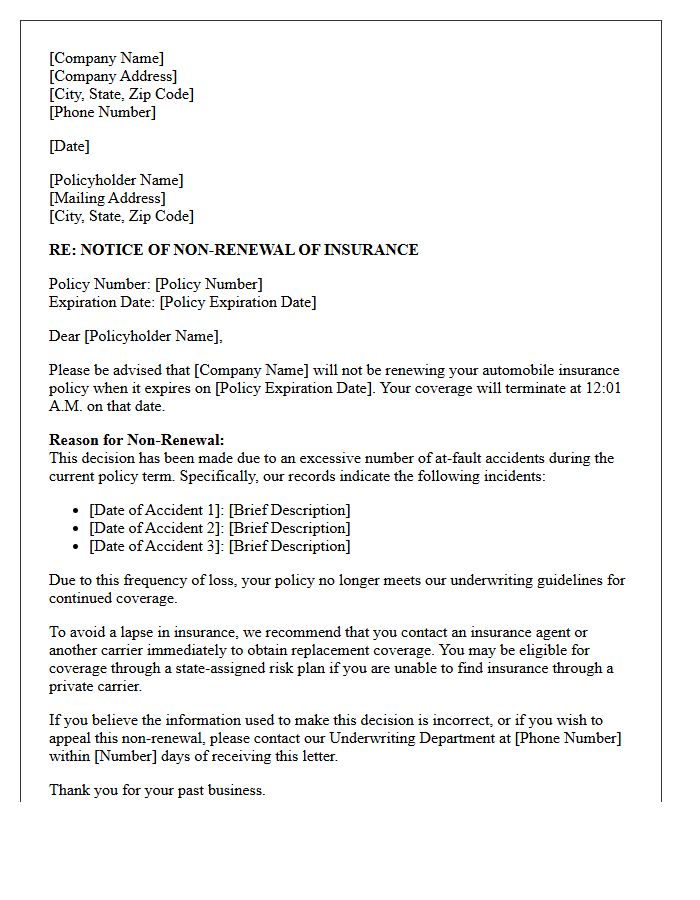

Standard Auto Insurance Non-Renewal Letter

A standard auto insurance non-renewal letter is a formal notice that your insurer will not extend your coverage past its expiration date. Unlike cancellation, this occurs at the end of a policy term. The most important thing to check is the underlying reason for the decision, which companies must legally disclose. You should also pay close attention to the effective expiration date to ensure you secure new coverage in time, avoiding a risky lapse that could lead to higher future premiums or legal penalties.

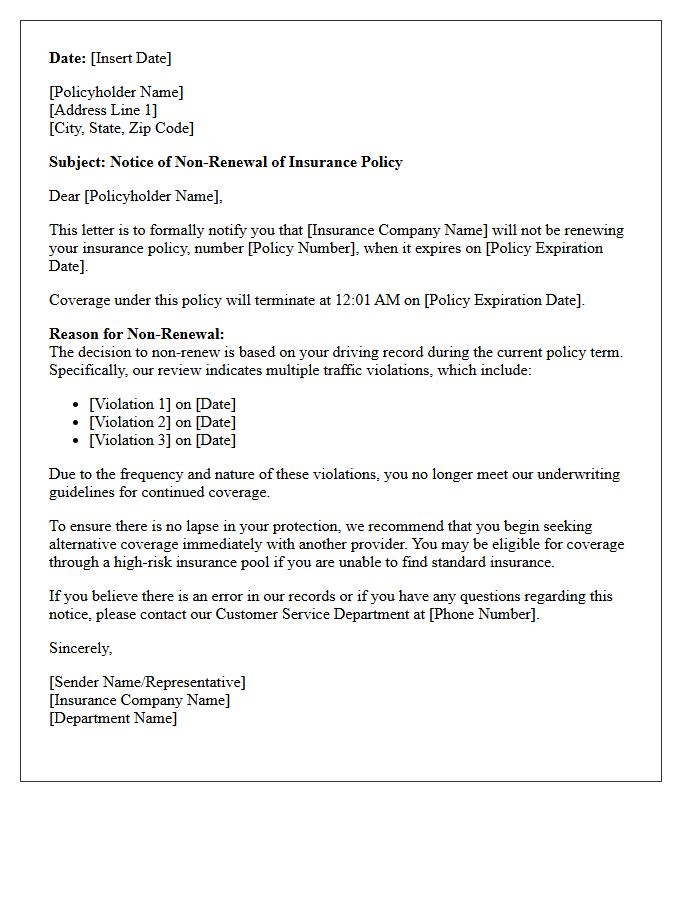

Notice of Non-Renewal Letter for Multiple Traffic Violations

A Notice of Non-Renewal for multiple traffic violations is a formal communication from your insurer stating they will not extend your coverage. Receiving this means your driving history has exceeded the company's risk threshold due to frequent infractions. It is crucial to immediately seek alternative insurance to avoid a legal lapse in coverage. This action differs from cancellation, as it occurs at the end of the policy term. Drivers should request their CLUE report to verify accuracy and explore high-risk providers or state-assigned risk plans to maintain road legality.

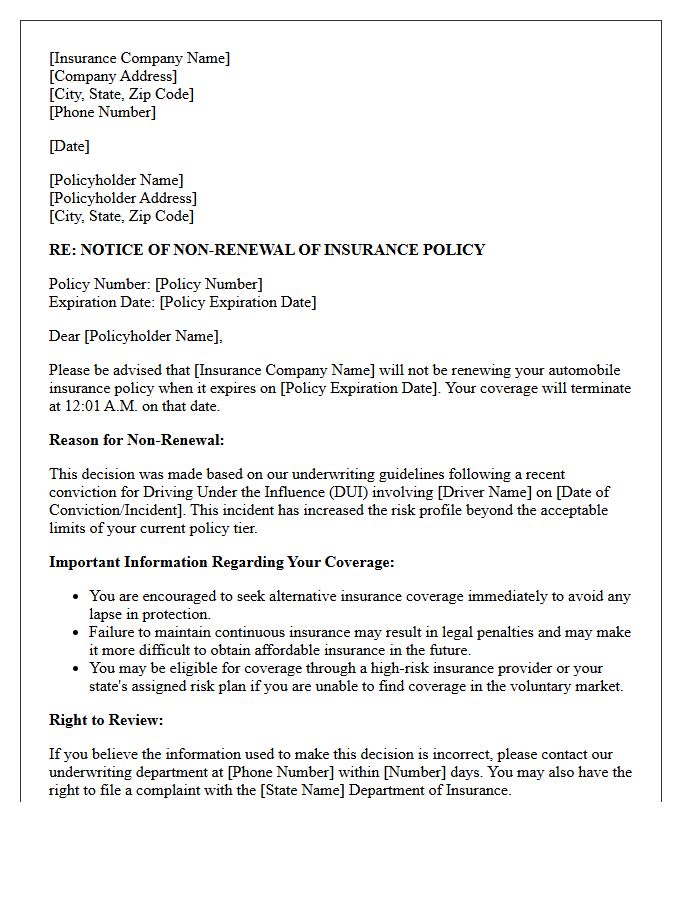

DUI Conviction Policy Non-Renewal Letter

Receiving a non-renewal letter after a DUI conviction signifies that your insurance provider has deemed you a high-risk driver and will terminate your policy at the end of the term. This formal notice is mandatory, often requiring the company to provide 30 to 60 days of advance warning. To maintain legal driving status, you must immediately seek non-standard insurance providers that specialize in high-risk coverage. You will likely need to file an SR-22 certificate to prove financial responsibility and reinstate your driving privileges with the state.

Excessive At-Fault Accidents Non-Renewal Letter

Receiving an Excessive At-Fault Accidents Non-Renewal Letter means your insurance provider has decided not to renew your policy due to a high frequency of preventable collisions. Insurers view multiple claims within a specific policy term as a sign of high risk. This notice typically arrives 30 to 60 days before expiration. To maintain coverage, you must quickly compare quotes from high-risk auto insurers. Improving your driving record and attending safety courses can eventually help you return to standard market rates and secure more affordable premiums.

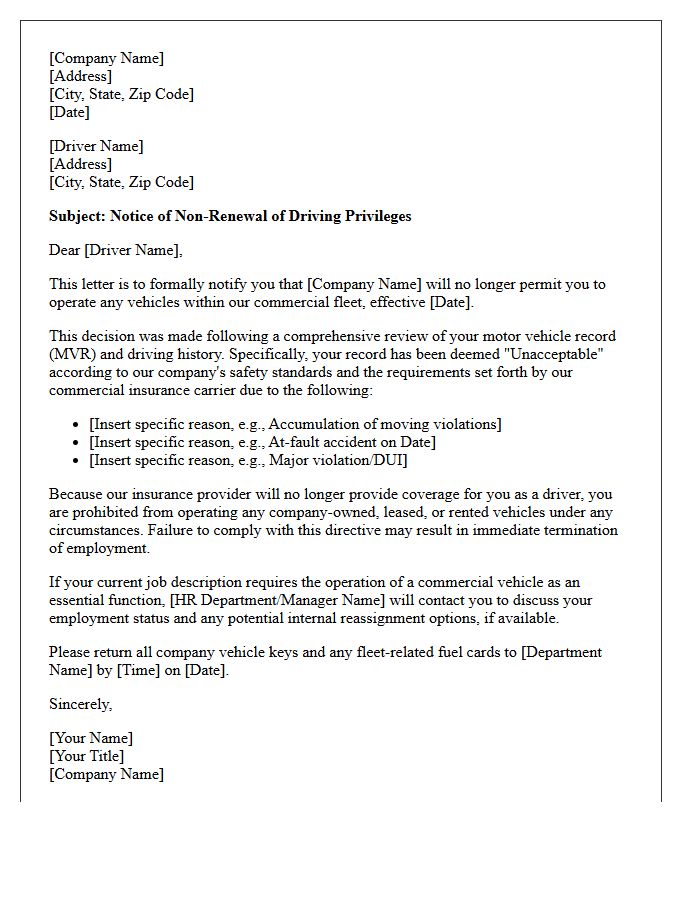

Commercial Fleet Driver Unacceptable Record Non-Renewal Letter

A Commercial Fleet Driver Unacceptable Record Non-Renewal Letter notifies a policyholder that a specific driver's motor vehicle record no longer meets underwriting standards. This formal notice typically results from excessive traffic violations or major accidents. To maintain overall fleet coverage, the carrier may require the exclusion of the high-risk driver. Promptly addressing these letters is critical to avoid a total policy cancellation. Employers should review the cited violations and consult with their agent to provide documentation or seek alternative risk management solutions to preserve their commercial insurance standing.

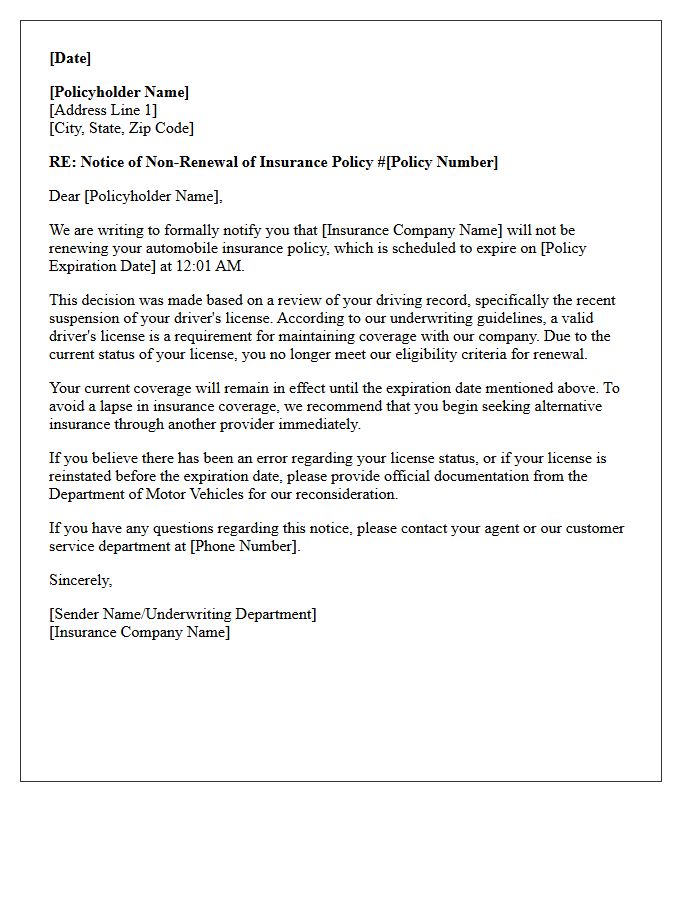

License Suspension Insurance Non-Renewal Letter

Receiving a non-renewal letter due to a license suspension means your insurer has decided to terminate your coverage at the end of the policy term. This typically occurs because a suspended license classifies you as a high-risk driver. It is crucial to address the underlying legal issues immediately to reinstate your driving privileges. You should quickly seek alternative coverage, such as SR-22 insurance, to avoid a lapse in protection. Failing to secure new insurance can lead to higher premiums and further legal complications with the Department of Motor Vehicles.

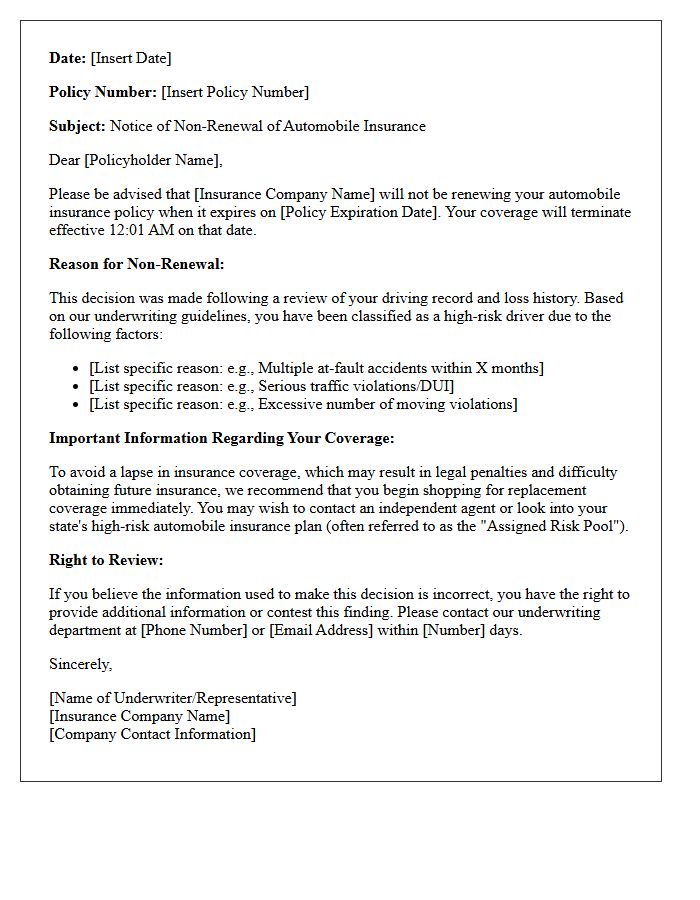

High-Risk Driver Classification Non-Renewal Letter

Receiving a non-renewal letter due to high-risk classification means your insurance provider will terminate coverage at the policy's end date. This typically occurs after multiple at-fault accidents, serious traffic violations, or a pattern of filing excessive claims. It is not a cancellation but a refusal to extend terms. To maintain legal compliance, you must immediately seek a non-standard insurance provider specializing in high-risk drivers. Acting quickly prevents a lapse in coverage, which could lead to significantly higher premiums or future eligibility issues with other competitive carriers.

DMV Points Accumulation Policy Non-Renewal Letter

Receiving a non-renewal letter indicates your insurance provider will terminate coverage at the end of the current term. This action is typically triggered by excessive DMV points accumulated from traffic violations or accidents. High point totals signal increased risk, making you ineligible for standard policies. To maintain legal driving status, you must urgently seek alternative coverage or high-risk insurance. Always review your driving record for accuracy, as these points directly impact your premiums and long-term eligibility for affordable protection.

Severe Driving Infraction Non-Renewal Letter

A severe driving infraction non-renewal letter is a formal notice from an insurer terminating your auto insurance policy at the end of its term. This typically occurs due to major violations like DUIs, reckless driving, or multiple at-fault accidents. Receiving this letter means the company views you as a high-risk driver. To maintain legal coverage, you must immediately seek alternative providers or specialized high-risk insurance pools. Acting quickly is essential to avoid a lapse in coverage, which can lead to further penalties and significantly higher future premiums.

Notice of Non-Renewal Letter Due to Excessive Speeding Citations

Receiving a Notice of Non-Renewal indicates your auto insurance provider will not extend coverage past the current policy expiration. When triggered by excessive speeding citations, the insurer views you as a high-risk driver. This formal legal document outlines the specific termination date, requiring you to secure a new policy immediately to avoid a coverage lapse. To minimize future premiums, maintain a clean driving record and compare quotes from carriers specializing in high-risk motorists, as your driving history directly impacts eligibility and rates.

Unacceptable Motor Vehicle Report Non-Renewal Letter

An Unacceptable Motor Vehicle Report Non-Renewal Letter is a formal notice from an insurance carrier stating they will not extend coverage due to adverse driving records. This decision is typically triggered by serious violations, such as DUIs, excessive speeding, or multiple at-fault accidents, which exceed the insurer's risk threshold. Receiving this letter means you must secure new insurance before the current policy expires to avoid a coverage lapse. You have a legal right to review the report and dispute any inaccuracies with the reporting agency to restore your insurability status.

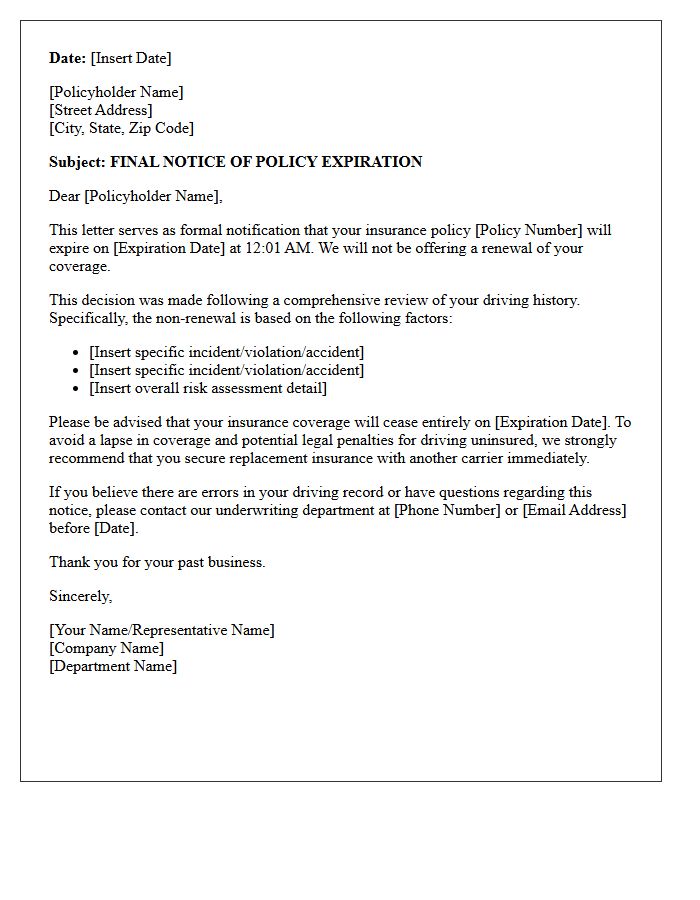

Final Notice of Policy Expiration Letter for Poor Driving History

A final notice of policy expiration indicates that your auto insurance coverage will cease on a specific date due to high-risk behavior. For drivers with a poor driving history, this letter often serves as a non-renewal notification triggered by multiple accidents or traffic violations. It is critical to secure a new policy immediately to avoid a coverage lapse, which can lead to higher premiums or legal penalties. Act quickly to explore specialized high-risk carriers and maintain continuous protection on the road.

What is a Notice of Non-Renewal due to an unacceptable driving record?

A Notice of Non-Renewal is a formal communication from an insurance carrier stating that they will not extend your policy beyond its current expiration date because your recent driving history no longer meets their underwriting safety standards.

What factors contribute to an "unacceptable" driving record?

Insurance companies typically classify a driving record as unacceptable if it contains multiple moving violations, at-fault accidents, or major infractions such as a DUI/DWI, reckless driving, or driving with a suspended license within a three to five-year period.

Can I appeal a non-renewal decision based on my driving history?

Yes, you can request a review if there is an error on your Motor Vehicle Report (MVR) or CLUE report. If the violations listed are incorrect or have been expunged, providing official court documentation to your insurer may lead them to rescind the non-renewal notice.

How long will an unacceptable driving record affect my insurance eligibility?

Most insurance providers look back at your driving history for three to five years. While a non-renewal stays on your internal insurance record, your eligibility for standard rates usually improves as older violations and accidents fall off your state motor vehicle report.

What should I do if my insurance is not renewed due to my driving habits?

If you receive a non-renewal notice, you should immediately begin shopping for "non-standard" or "high-risk" auto insurance. It is crucial to secure a new policy before your current one expires to avoid a lapse in coverage, which can lead to even higher premiums and legal penalties.

Comments