Inform your insurance provider about recent upgrades or renovations to ensure your residence remains fully protected. Sending a formal Property Addition to Homeowners Policy Letter guarantees that your coverage limits reflect the true value of your improved home, preventing financial gaps during claims. Secure your investment by documenting structural changes today; below are some ready to use template options to simplify the process.

Image cover: Formal Request Templates for Adding Property to Your Homeowners Insurance Policy

Letter Samples List

- Property Addition to Homeowners Policy Letter

- Confirmation of Property Addition Letter

- Scheduled Personal Property Addition Letter

- High-Value Item Appraisal Request Letter

- Premium Adjustment Notification Letter

- New Structure Coverage Addition Letter

- Home Renovation Coverage Update Letter

- Policy Endorsement Declaration Letter

- Coverage Limit Increase Acknowledgment Letter

- Updated Homeowners Policy Declaration Letter

- Newly Acquired Property Notification Letter

- Valuable Items Insurance Rider Letter

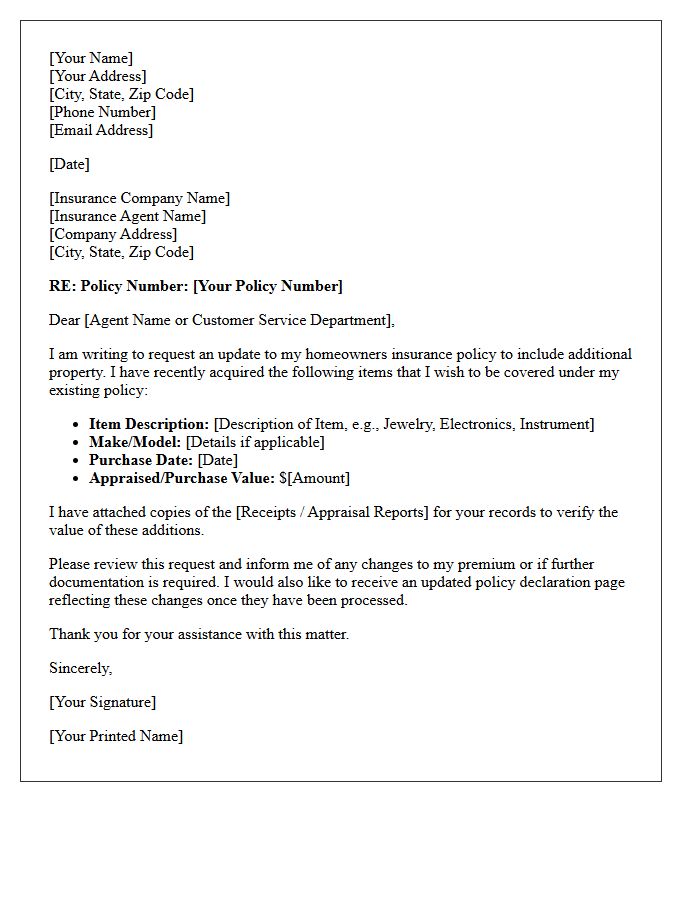

Property Addition to Homeowners Policy Letter

A property addition letter serves as formal notification to your insurance provider regarding significant home improvements. It is essential to document structural changes, such as new rooms or decks, to ensure your replacement cost reflects the home's current value. This letter initiates a policy endorsement, preventing potential coverage gaps during a claim. By updating your records, you guarantee that your investment remains fully protected under your homeowners policy. Always include receipts and photos to verify the increased property value and maintain adequate financial protection against unforeseen losses.

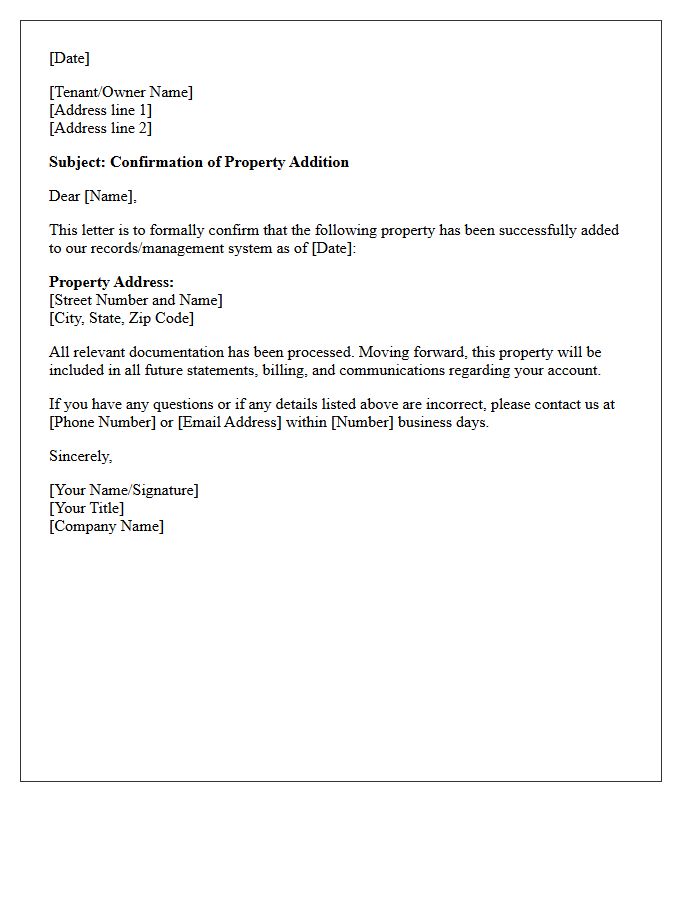

Confirmation of Property Addition Letter

A Confirmation of Property Addition Letter serves as formal legal verification that a specific asset has been officially included in a real estate portfolio, insurance policy, or trust. This document is essential for maintaining accurate ownership records and ensuring comprehensive liability coverage. It typically details the property address, effective date, and any adjusted policy terms. Retaining this letter is crucial for risk management and serves as vital evidence during property disputes, tax assessments, or insurance claims to prove the asset is recognized and protected by the governing entity.

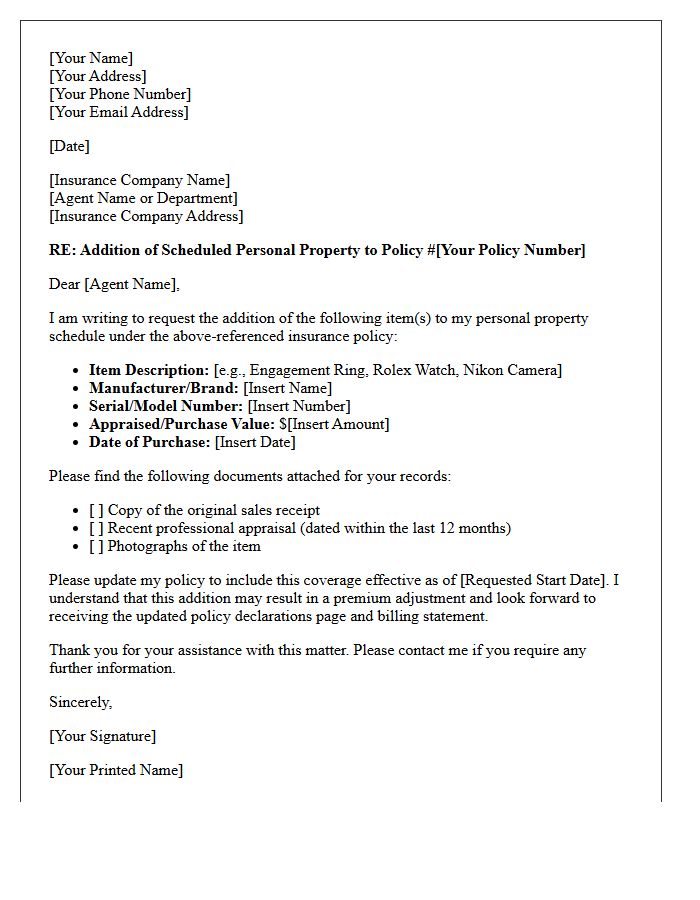

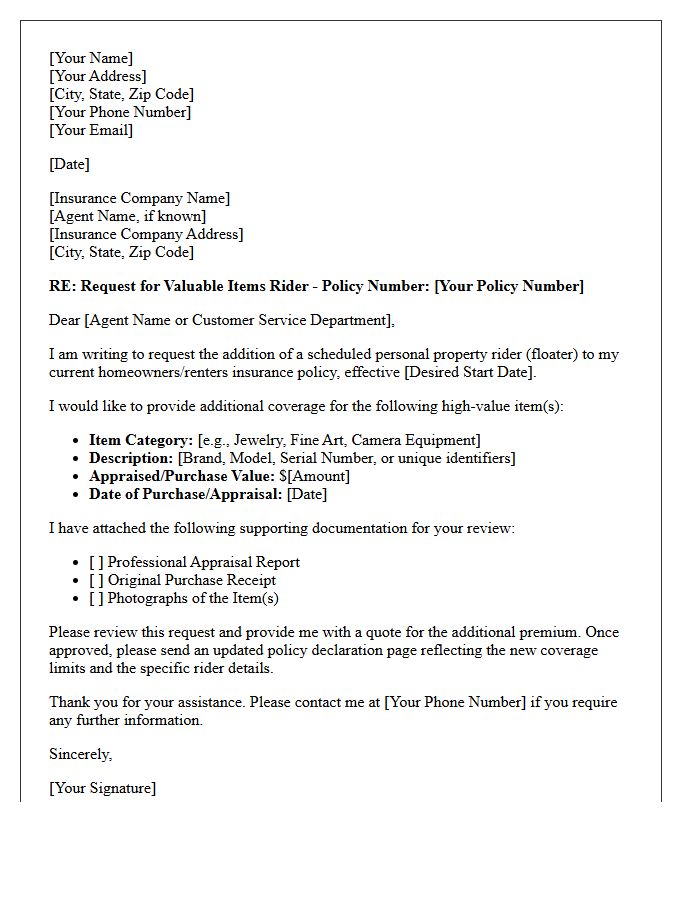

Scheduled Personal Property Addition Letter

A Scheduled Personal Property Addition Letter is a formal request to expand your insurance coverage for high-value items. This document ensures that high-ticket possessions like jewelry, fine art, or electronics are protected beyond standard policy limits. By providing a professional appraisal or detailed receipt, you establish a guaranteed replacement value. This process eliminates deductibles for specific items and provides broader protection against accidental loss or damage, ensuring your most prized assets are fully indemnified under a specialized floater or endorsement.

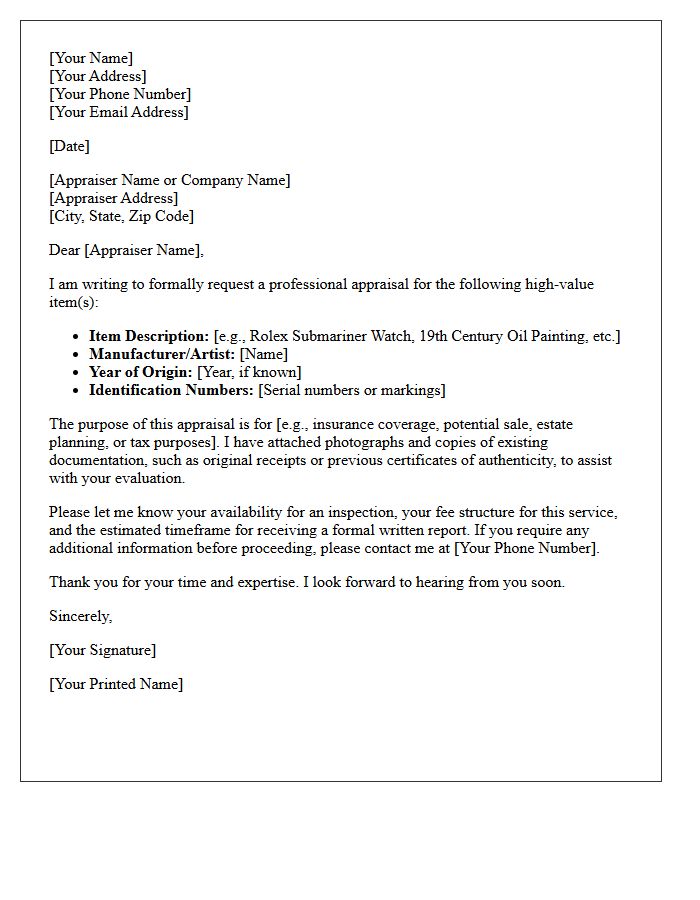

High-Value Item Appraisal Request Letter

A High-Value Item Appraisal Request Letter is a formal document sent to a certified appraiser to establish the replacement value or fair market price of luxury assets. It should clearly identify the object, its provenance, and the purpose of the valuation, such as insurance coverage, estate planning, or tax documentation. Providing detailed descriptions and photographs helps ensure an accurate assessment. This letter serves as a critical first step in protecting your financial interests and ensuring legal compliance during the professional evaluation of jewelry, art, or rare collectibles.

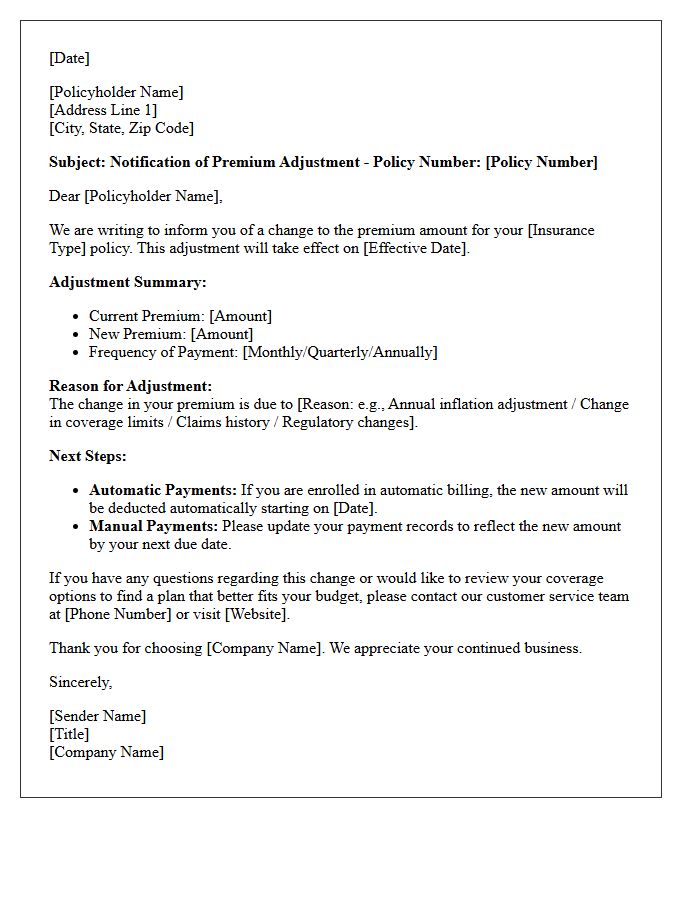

Premium Adjustment Notification Letter

A Premium Adjustment Notification Letter is a formal document sent by insurance providers to inform policyholders of changes in their coverage costs. It typically outlines the new billing amount, the effective date of the change, and the specific reasons for the adjustment, such as inflation, updated risk assessments, or plan enhancements. Reviewing this notice is essential for maintaining continuous coverage and ensuring your financial planning aligns with updated premium obligations. Always verify the details to understand how these modifications affect your policy's overall value and your budget.

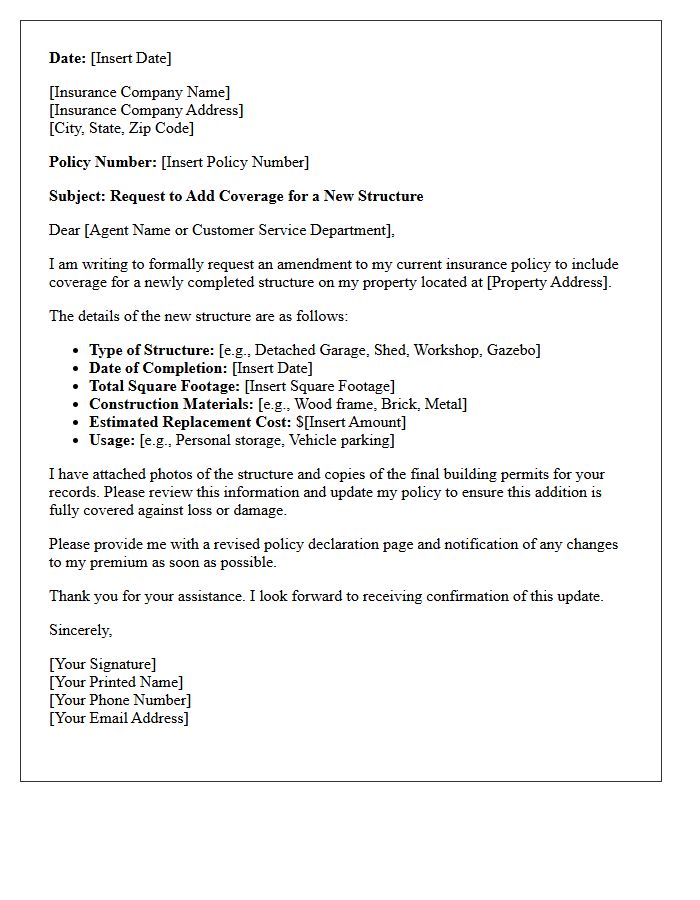

New Structure Coverage Addition Letter

A New Structure Coverage Addition Letter is a formal document notifying your insurer about a newly constructed building on your property. This letter is essential to ensure the uninterrupted extension of your existing policy to include the new asset. Providing accurate details, such as the structure's purpose, dimensions, and materials, helps adjust your replacement cost and liability limits. Failing to submit this notification promptly could leave the structure uninsured against risks like fire or theft. Always request a written endorsement to confirm your policy has been updated correctly.

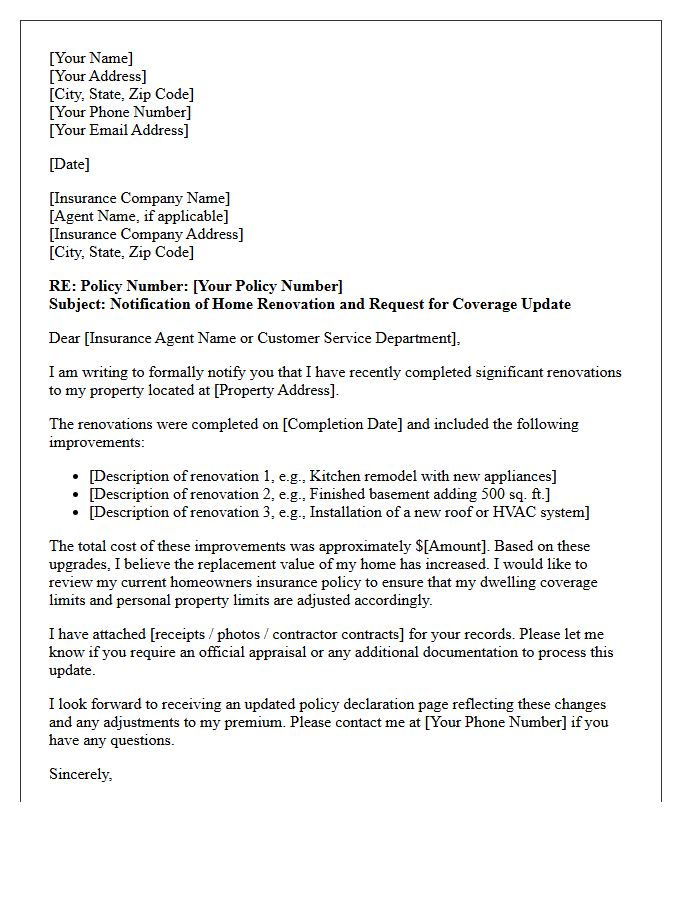

Home Renovation Coverage Update Letter

A Home Renovation Coverage Update Letter is a vital document sent to your insurance provider to ensure your policy reflects current property values. Significant structural changes or high-end upgrades can leave you underinsured if not formally documented. This notice protects your investment by adjusting coverage limits to match the new replacement cost. Failing to provide this update may result in denied claims or financial gaps after a loss. Always include receipts and permit details to maintain comprehensive protection for your newly improved home and personal assets.

Policy Endorsement Declaration Letter

A Policy Endorsement Declaration Letter is a formal legal document issued by an insurer to confirm specific amendments made to an existing insurance contract. It serves as official proof that terms, coverage limits, or premium amounts have been updated. This letter is crucial for maintaining accurate records and ensuring that any claims are processed based on the most current policy details. Always review this declaration to verify that all requested changes are correctly reflected, as it supersedes previous agreements within the policy period.

Coverage Limit Increase Acknowledgment Letter

A Coverage Limit Increase Acknowledgment Letter is a formal document confirming a policyholder's request to raise their insurance protection. This letter serves as legal proof of the adjustment, detailing the new maximum payout amounts and the effective date. It ensures that both parties agree on the enhanced financial security provided by the updated terms. Reviewing this document is essential to verify that the liability thresholds meet your current needs, as it directly impacts premium costs and the scope of your indemnification in the event of a future claim.

Updated Homeowners Policy Declaration Letter

An updated homeowners policy declaration letter is a legal summary of your current insurance coverage. It highlights essential details such as policy limits, deductibles, and annual premiums. Homeowners must review this document to ensure the dwelling protection reflects current rebuilding costs and that all endorsements are accurate. This letter serves as official proof of insurance for mortgage lenders and confirms your coverage dates. Always verify that your personal information and liability amounts are correct to avoid gaps in financial protection during a claim.

Newly Acquired Property Notification Letter

A Newly Acquired Property Notification Letter is a formal document sent to an insurance provider to secure coverage for a recent purchase. It is essential to submit this notice within the specific reporting window, typically 30 days, to ensure continuous protection. The letter should include the acquisition date, property value, and location details. Failure to provide timely notification may result in a coverage gap, leaving the new asset uninsured against potential risks or damages under the existing policy framework.

Valuable Items Insurance Rider Letter

A Valuable Items Insurance Rider is a critical policy endorsement that extends coverage for high-value assets like jewelry, fine art, or collectibles. Standard homeowners' policies often have low sub-limits for these items, leaving you underinsured. By providing a professional appraisal and a formal request letter, you ensure these belongings are protected at their full appraised value against loss, theft, or damage. This additional layer of protection typically eliminates deductibles for the scheduled items, offering comprehensive financial security for your most prized personal possessions.

What is a property addition notice for a homeowners policy?

A property addition notice is a formal letter or communication sent to your insurance provider to inform them of new structures, high-value purchases, or significant home improvements that need to be included under your existing coverage.

When should I send a letter to add property to my insurance?

You should notify your insurer immediately after completing a home renovation, building an accessory dwelling unit (ADU), or acquiring luxury items like jewelry or electronics to ensure these assets are protected against loss or damage.

What information is required in a property addition letter?

The letter should include your policy number, a detailed description of the new property, the date of acquisition or completion, the estimated replacement cost or appraised value, and any relevant receipts or professional appraisals.

Does adding property to my homeowners policy increase my premium?

Yes, increasing your coverage limits to account for new property or structural additions typically results in a premium adjustment, as the insurance company is assuming a higher financial risk for the total replacement value of your home.

Can I add a home office or shed through a standard property addition letter?

Yes, detached structures like sheds, garages, or home offices can be added to your policy; however, you must specify if the space will be used for business purposes, as this may require additional liability endorsements.

Comments