Protect your high-value assets by formally updating your insurance coverage. A Scheduled Personal Property Alteration Letter allows you to add, remove, or adjust the appraised value of specific items like jewelry, art, or electronics on your policy. Using a professional request ensures your specialized endorsements remain accurate and valid. To simplify this process, below are some ready to use template.

Image cover: Official Templates: Requesting Changes to Your Scheduled Personal Property Coverage

Letter Samples List

- Scheduled Personal Property Item Addition Letter

- Scheduled Personal Property Item Removal Letter

- Scheduled Personal Property Appraisal Update Letter

- Scheduled Personal Property Value Adjustment Letter

- Scheduled Personal Property Coverage Limit Alteration Letter

- Scheduled Personal Property Item Substitution Letter

- Scheduled Personal Property Description Amendment Letter

- Scheduled Personal Property Endorsement Confirmation Letter

- Scheduled Personal Property Newly Acquired Item Letter

- Scheduled Personal Property Sold Item Cancellation Letter

- Scheduled Personal Property Premium Recalculation Letter

- Scheduled Personal Property Location Change Letter

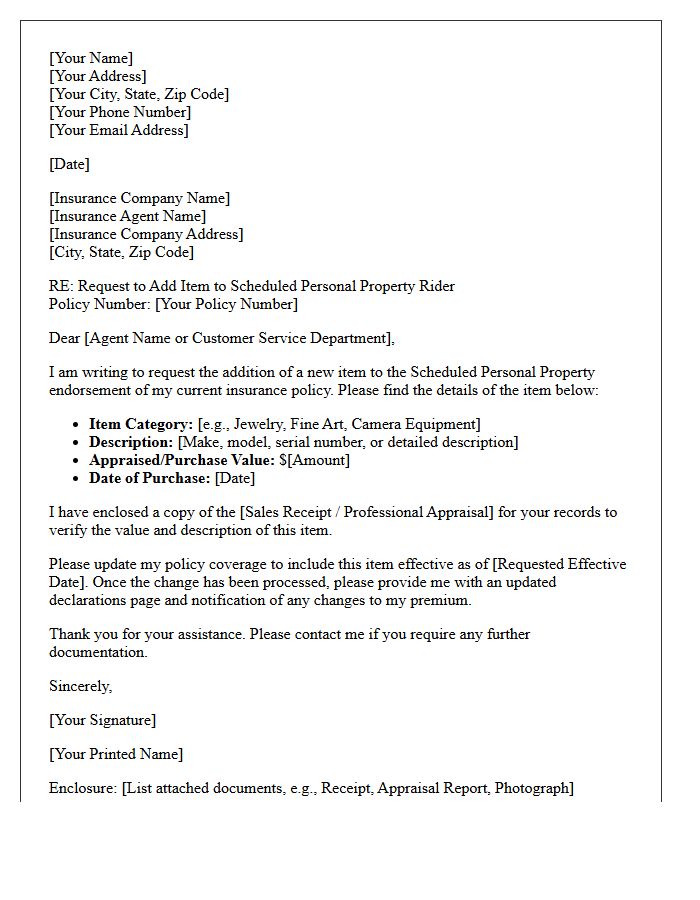

Scheduled Personal Property Item Addition Letter

A Scheduled Personal Property Item Addition Letter is a formal request to your insurer to include high-value assets under a Scheduled Personal Property endorsement. This document ensures specific items like jewelry, art, or electronics receive extended coverage beyond standard policy limits. You must provide a detailed description and a professional appraisal to verify the current market value. By submitting this letter, you protect your investment against broader risks, such as accidental loss or theft, with zero deductible options typically applied to the listed valuables.

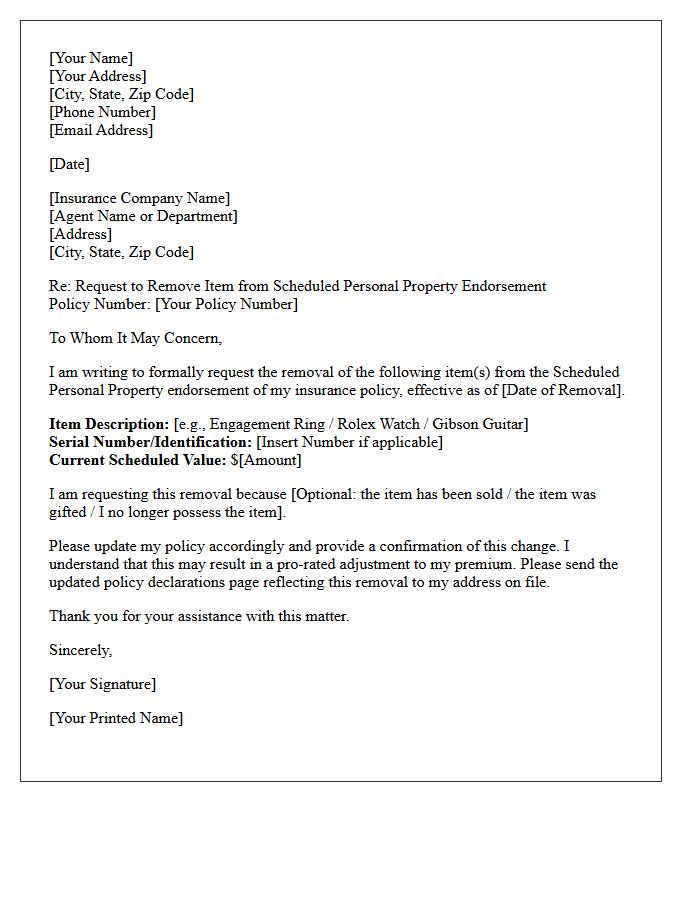

Scheduled Personal Property Item Removal Letter

A Scheduled Personal Property Item Removal Letter is a formal request to your insurance provider to exclude a specific high-value asset from your policy. Use this document to terminate coverage for items you no longer own or wish to insure separately, such as jewelry, art, or electronics. Providing the item description and effective date ensures your premiums are adjusted correctly. This update helps maintain an accurate inventory and prevents paying unnecessary costs for protection you no longer require. Always request a written confirmation to verify the policy endorsement has been processed.

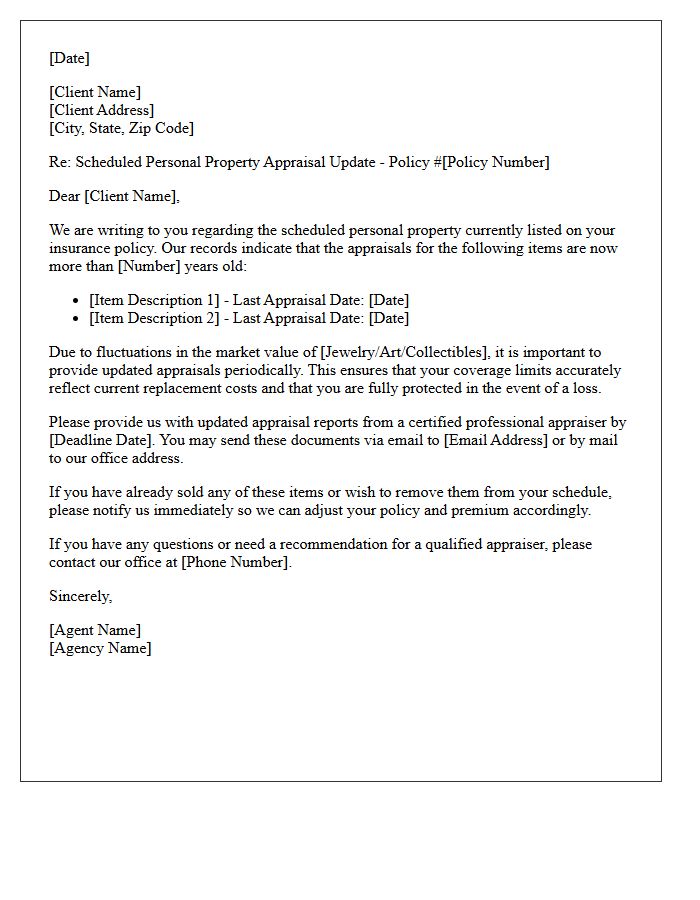

Scheduled Personal Property Appraisal Update Letter

A Scheduled Personal Property Appraisal Update Letter is a crucial document used to maintain accurate insurance coverage for high-value items like jewelry, art, or collectibles. Since market values fluctuate, insurers require periodic appraisal updates to ensure your policy reflects current replacement costs. Failing to submit these updates can lead to significant underinsurance in the event of a loss. By proactively providing certified valuations, you protect your financial investment and guarantee that your specialized endorsements remain valid and sufficient to cover the full worth of your most prized possessions.

Scheduled Personal Property Value Adjustment Letter

A Scheduled Personal Property Value Adjustment Letter notifies policyholders of changes to the insured value of high-value items like jewelry or fine art. Over time, market prices fluctuate, requiring periodic appraisals to ensure coverage remains accurate. Reviewing this document is essential to prevent underinsurance, as it adjusts your premiums based on current replacement costs. Always verify these updates to maintain financial protection against loss or damage, ensuring your most prized possessions are fully covered at their true market worth without unexpected out-of-pocket expenses during a claim.

Scheduled Personal Property Coverage Limit Alteration Letter

A Scheduled Personal Property Coverage Limit Alteration Letter is a formal notification used to adjust the insured value of high-value items like jewelry, art, or electronics. This document ensures your policy limits reflect current market appraisals, preventing underinsurance during a claim. It is essential to submit this letter alongside updated professional valuations to guarantee full financial protection. By explicitly listing individual assets, you bypass standard sub-limits found in basic homeowners policies, securing comprehensive coverage for your most significant investments.

Scheduled Personal Property Item Substitution Letter

A Scheduled Personal Property Item Substitution Letter is a formal request sent to an insurance provider to update your policy. This document ensures continuous coverage when replacing high-value assets like jewelry or electronics. It is vital to include the appraisal and a detailed description of the new item to maintain accurate protection. Promptly notifying your insurer via this letter prevents gaps in liability and ensures that your agreed value reflects your current inventory. Always keep a confirmed copy of this substitution for your financial records and claims processing.

Scheduled Personal Property Description Amendment Letter

A Scheduled Personal Property Description Amendment Letter is a formal document used to update insurance coverage for specific high-value items. This letter ensures that jewelry, fine art, or electronics are accurately described to reflect their current value or condition. By submitting this written request, policyholders guarantee that their most prized possessions are fully protected under a scheduled floater, bypassing standard policy limits. It is an essential step for maintaining comprehensive financial protection against loss or damage for unique assets that require individual valuation and specialized endorsement.

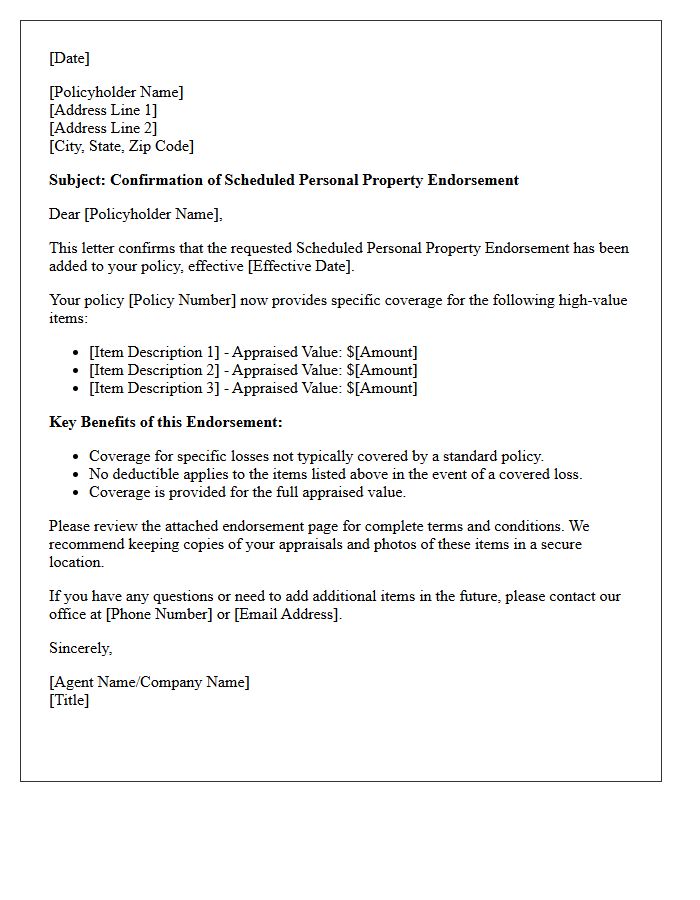

Scheduled Personal Property Endorsement Confirmation Letter

A Scheduled Personal Property Endorsement provides broader coverage for high-value items like jewelry or electronics. Receiving a confirmation letter is essential, as it verifies that specific assets are protected beyond standard policy limits. This document confirms agreed-upon valuations and often eliminates deductibles for the listed items. Always review your letter to ensure descriptions and appraisal values are accurate, ensuring comprehensive financial protection against loss, theft, or accidental damage that basic homeowners insurance might exclude.

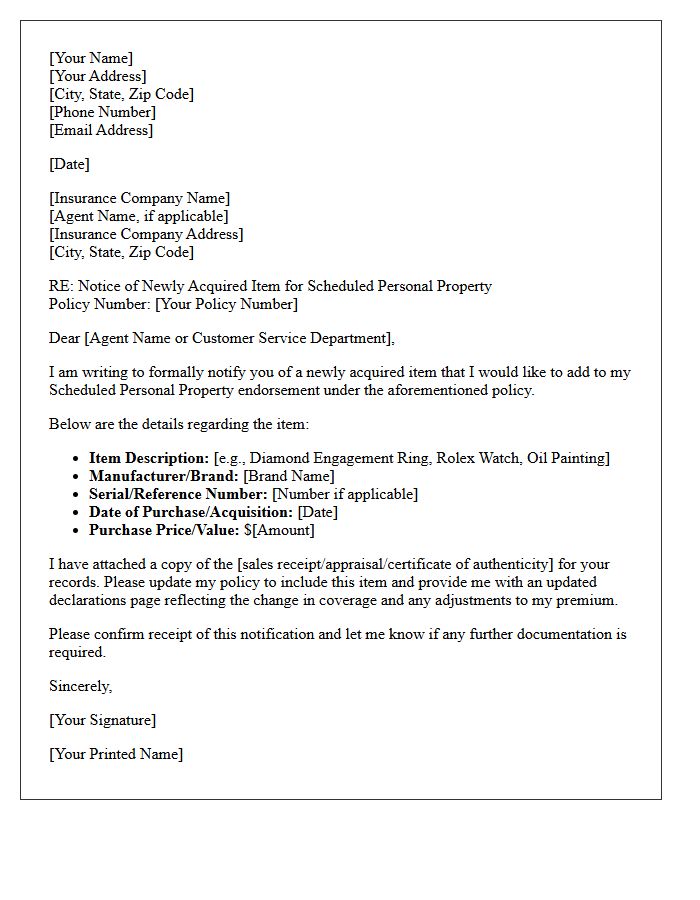

Scheduled Personal Property Newly Acquired Item Letter

A Scheduled Personal Property Newly Acquired Item Letter is a formal notification to your insurance provider regarding a high-value purchase. To ensure continuous coverage for luxury goods like jewelry, fine art, or cameras, you must report these items within a specific grace period, typically 30 to 90 days. Sending this letter promptly guarantees that your new investment is protected against loss or theft under your policy's scheduled floater. Always include a professional appraisal or sales receipt to verify the replacement value and secure your financial interests immediately.

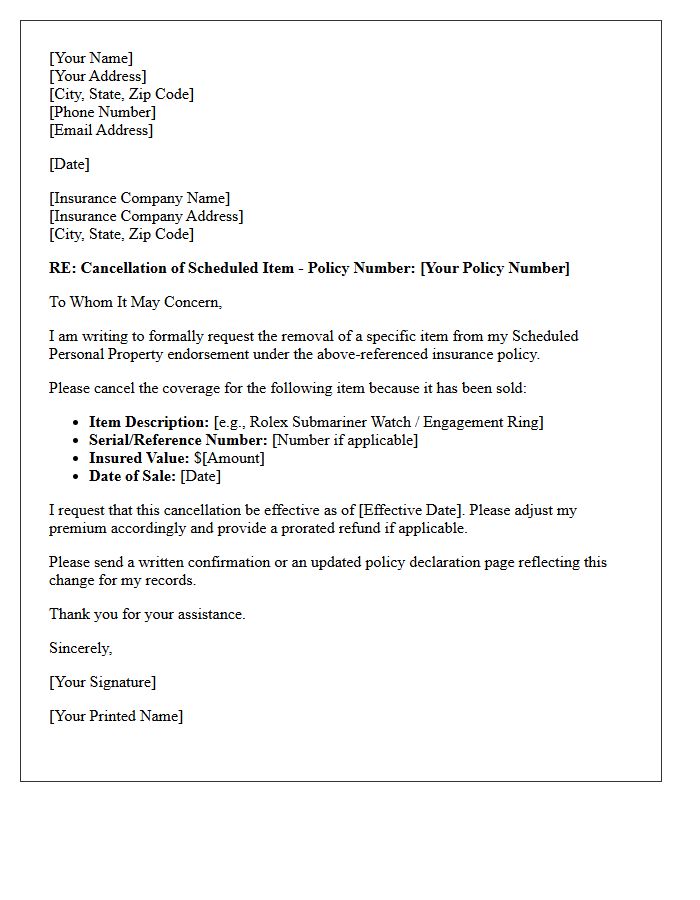

Scheduled Personal Property Sold Item Cancellation Letter

A Scheduled Personal Property Sold Item Cancellation Letter is a formal request to remove a specific high-value asset from your insurance policy after its sale. Clearly state the item's description, serial number, and the exact date of disposal to ensure accurate premium adjustments. This document serves as legal proof to stop coverage and trigger a pro-rata refund for any unused premiums. Always request written confirmation from your insurer to verify that the schedule has been updated and the liability for that specific item has officially terminated.

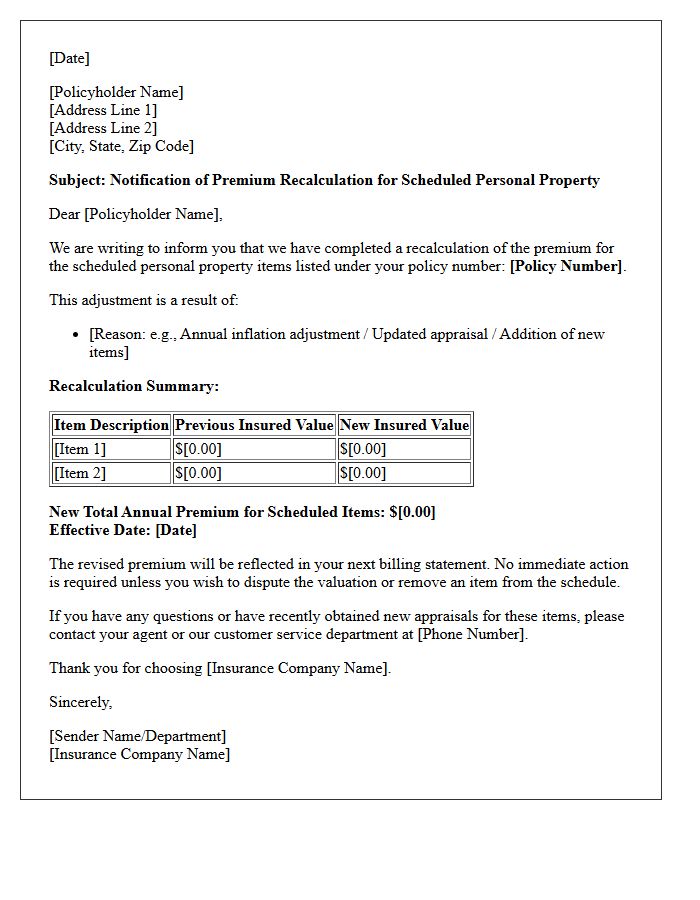

Scheduled Personal Property Premium Recalculation Letter

A Scheduled Personal Property Premium Recalculation Letter informs you of a cost adjustment for high-value items like jewelry or electronics. This notice occurs when scheduled endorsements are updated based on new appraisals or inflation protection adjustments. It ensures your replacement cost coverage reflects current market values. Reviewing this letter is essential to confirm that your specific assets remain fully insured against loss or damage, as the premium change directly impacts your policy's total premium and benefit limits for individual valuables.

Scheduled Personal Property Location Change Letter

A Scheduled Personal Property Location Change Letter is a formal notification to your insurance provider regarding the permanent relocation of high-value items. It is crucial to update your policy whenever jewelry, art, or equipment moves to a new residence to ensure continuous coverage. Providing the new physical address prevents potential claim denials due to inaccurate location data. This document maintains the integrity of your floater policy, guaranteeing that specific endorsements remain valid under the risk profile of your current environment and protective security measures.

What is a Scheduled Personal Property Alteration Letter?

A Scheduled Personal Property Alteration Letter is a formal request sent to an insurance provider to modify, add, or remove specific high-value items-such as jewelry, art, or electronics-listed on an existing insurance policy endorsement.

When should I send an alteration letter for scheduled items?

You should send an alteration letter immediately following the purchase of a new luxury item, after receiving a professional reappraisal that changes an item's value, or when you sell an item and wish to remove it from your coverage.

What information must be included in a property alteration request?

The letter should include your policy number, a detailed description of the item (make, model, serial number), the current appraised value, the effective date of the change, and any supporting documentation like sales receipts or certified appraisals.

Does an alteration letter guarantee immediate coverage for new items?

While the letter initiates the process, coverage is typically finalized once the insurer acknowledges the request and adjusts the premium. It is recommended to obtain written confirmation or a revised declarations page to ensure the alteration is active.

How does a scheduled property alteration affect my insurance premium?

Modifying your scheduled personal property will likely change your premium; adding items or increasing appraised values usually results in a premium increase, while removing items or decreasing values will lower the total cost of the endorsement.

Comments