Many seniors seek financial flexibility without committing to a reverse mortgage. Exploring Retiree Reverse Mortgage Alternatives, such as home equity lines of credit, downsizing, or leaseback programs, can preserve your legacy while providing necessary cash flow. This guide examines smart financial strategies to help you leverage home equity safely. To assist your planning, below are some ready to use template.

Image cover: Smart Financial Options: Letter Templates for Reverse Mortgage Alternatives

Letter Samples List

- Downsizing Your Home as a Reverse Mortgage Alternative Letter

- Unlocking Home Equity Through a Traditional Property Sale Letter

- Relocating to a Lower Cost of Living Area Letter

- Leasing Your Current Property for Steady Retirement Income Letter

- Selling and Renting a Luxury Senior Apartment Letter

- Transitioning to a Low-Maintenance Condominium Letter

- Exploring Multi-Generational Living Real Estate Options Letter

- Selling Your Estate to Fund a Comfortable Retirement Letter

- Purchasing an Accessible Turnkey Property Letter

- Trading Your Large Family Home for a Smaller Residence Letter

- Liquidating Real Estate Assets for Long-Term Wealth Letter

- Selling and Relocating to a Dedicated Retirement Community Letter

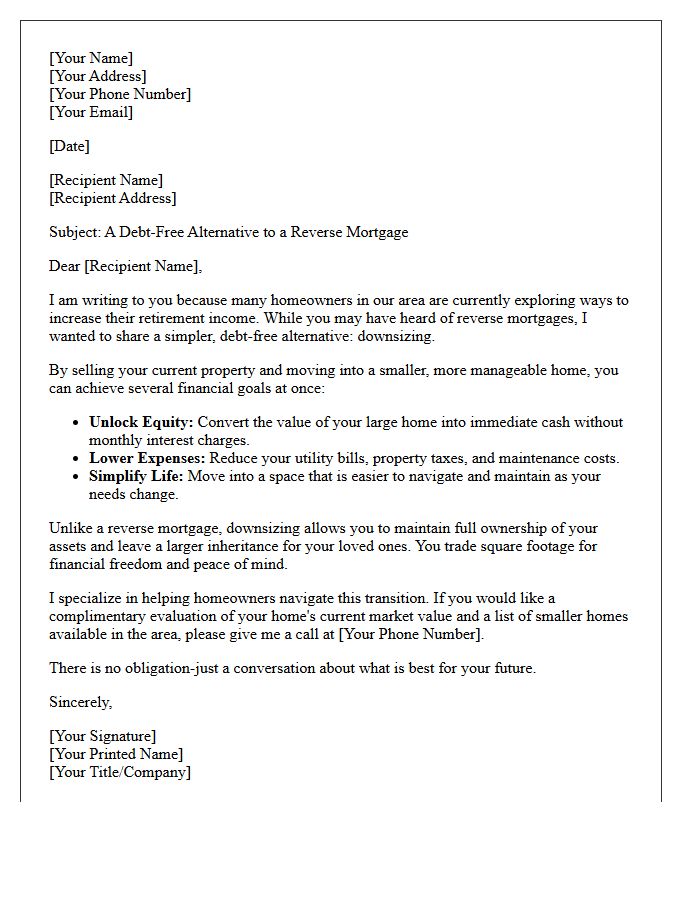

Downsizing Your Home as a Reverse Mortgage Alternative Letter

Downsizing offers a strategic reverse mortgage alternative for homeowners seeking financial freedom. By selling a large property and moving to a smaller residence, you can unlock home equity without incurring loan interest or monthly fees. This transition eliminates debt obligations while significantly reducing ongoing maintenance costs and utility expenses. Choosing to downsize provides immediate liquidity and simplifies your lifestyle, making it a powerful equity management tool. Always compare the long-term appreciation potential of your current home against the immediate cash flow benefits of relocation to ensure the best retirement outcome.

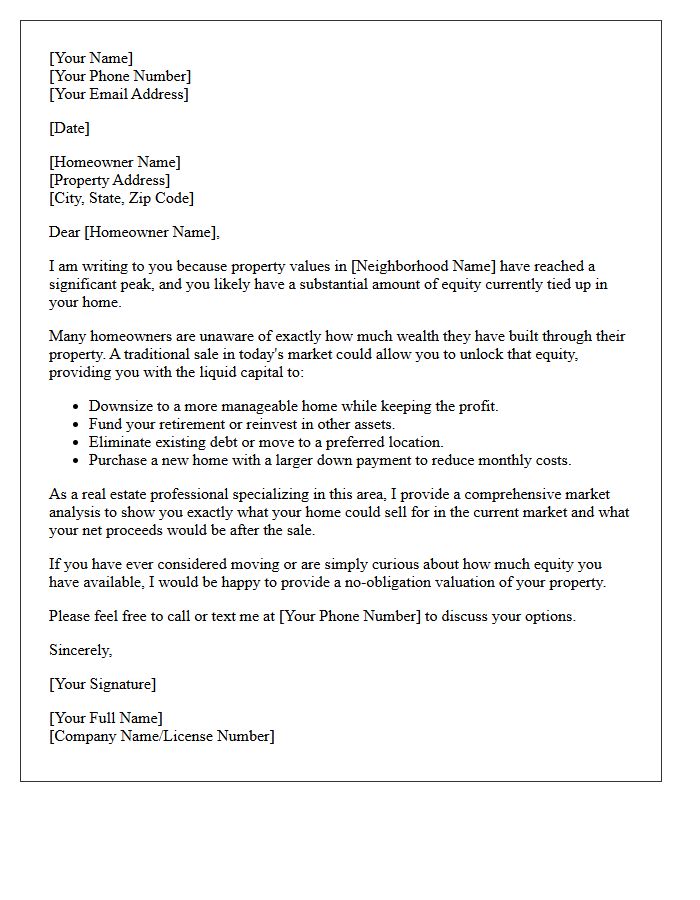

Unlocking Home Equity Through a Traditional Property Sale Letter

A traditional property sale letter is a strategic tool for unlocking home equity by directly connecting with motivated buyers. To maximize your financial return, the letter must highlight the property's unique value and prime location. Market timing and professional presentation are essential to attract competitive offers. By bypassing some intermediary steps, homeowners can streamline the divestment process and access liquid capital efficiently. Crafting a compelling narrative ensures you capture the maximum market value of your investment, turning physical real estate into accessible wealth for future opportunities.

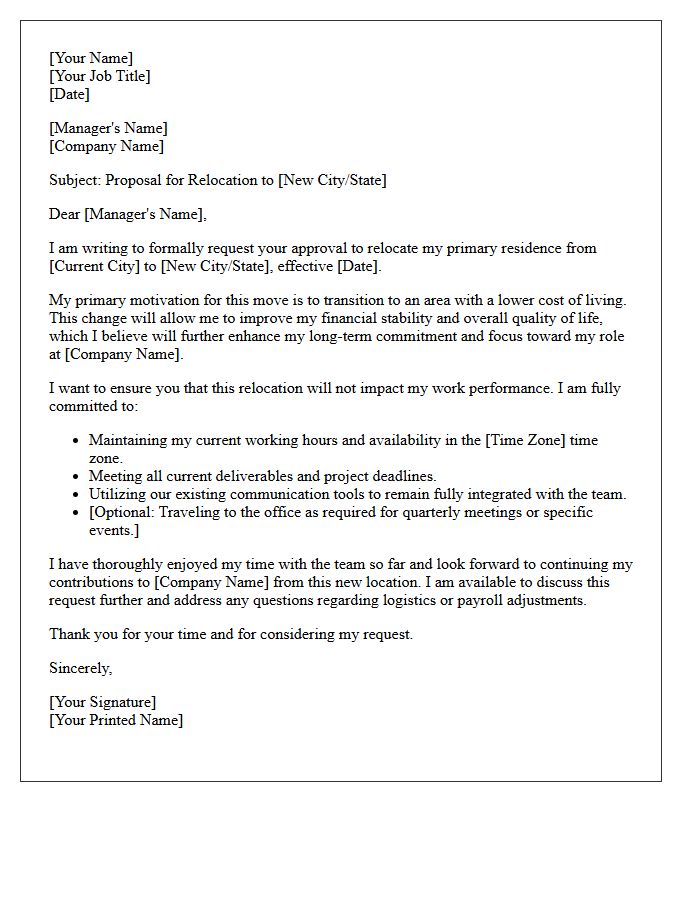

Relocating to a Lower Cost of Living Area Letter

A Relocating to a Lower Cost of Living Area Letter is a formal request to maintain your current salary while moving to a more affordable region. The most critical element is demonstrating that your productivity and value remain consistent regardless of geography. Clearly outline your transition plan, emphasizing how remote work benefits the company through continued excellence. Highlighting your commitment to long-term retention and professional reliability helps justify why a downward salary adjustment is unnecessary, ensuring your financial gain from the move is preserved.

Leasing Your Current Property for Steady Retirement Income Letter

Retiring property owners can secure steady passive income by transitioning their current residence into a long-term rental. A formal letter to a management company or tenant should emphasize reliable cash flow and long-term stability. This strategy provides a consistent financial cushion without liquidating valuable real estate assets. Highlighting property maintenance and clear lease terms ensures financial security during retirement years. Converting equity into monthly revenue is an effective way to maintain your lifestyle while preserving generational wealth through continued property ownership and market appreciation.

Selling and Renting a Luxury Senior Apartment Letter

When drafting a letter for luxury senior apartments, focus on highlighting exclusive amenities and personalized care services. Clearly outline the upscale lifestyle, including gourmet dining and wellness programs, to appeal to discerning residents. Ensure the tone is professional yet warm, addressing both financial transparency and the emotional transition involved in relocating. Providing a clear call to action for private tours is essential for converting prospects. Emphasize how your community offers superior comfort and security, making it the premier choice for sophisticated retirement living and long-term investment.

Transitioning to a Low-Maintenance Condominium Letter

A Transitioning to a Low-Maintenance Condominium Letter serves as formal notification to residents regarding shifts in property management responsibilities. It clearly outlines which landscaping, exterior repairs, and snow removal tasks move from individual owners to the association. Key details should include the effective date, updated fee structures, and specific service boundaries. This document ensures operational transparency, helping homeowners understand their reduced maintenance obligations while maintaining community aesthetic standards. Providing direct contact information for the new service providers is essential for a smooth administrative handover.

Exploring Multi-Generational Living Real Estate Options Letter

When drafting a Multi-Generational Living inquiry, emphasize your need for flexible layouts like accessory dwelling units or dual-master suites. Clearly state your desire for shared equity and functional privacy to accommodate aging parents or adult children. Highlighting these specific spatial requirements helps agents identify properties with zoning potential. Focusing on inclusive design ensures the home supports long-term accessibility and comfort for every family member across different life stages.

Selling Your Estate to Fund a Comfortable Retirement Letter

Drafting a formal letter to sell your estate is a strategic step toward securing a comfortable retirement. This document should clearly outline your intent to liquidate assets, such as real estate or collectibles, to ensure financial liquidity. It is essential to provide a detailed inventory and professional valuations to attract serious buyers. By articulating your long-term goals, you establish a transparent framework for a smooth transition, allowing you to convert your hard-earned legacy into a reliable income stream for your future lifestyle needs.

Purchasing an Accessible Turnkey Property Letter

A Purchasing an Accessible Turnkey Property Letter is a formal document used to express interest in a move-in-ready home that meets specific ADA compliance or mobility standards. It highlights the buyer's intent to secure a barrier-free residence without needing further renovations. This letter often includes proof of funds and emphasizes the necessity of features like universal design, ramps, and widened doorways. Clearly stating these requirements ensures a smooth transaction for buyers seeking immediate independent living solutions in a competitive real estate market.

Trading Your Large Family Home for a Smaller Residence Letter

A downsizing letter helps homeowners secure a smaller residence by personalizing their offer to sellers. It is essential to explain why you are trading your large family home for a manageable lifestyle, emphasizing your financial readiness and commitment to the property. Highlighting your transition from a sprawling estate to a compact living space builds rapport and trust. Clearly stating your intent and flexible closing dates can make your proposal stand out in competitive markets, ensuring a smooth move into a more efficient, right-sized home better suited for your current needs.

Liquidating Real Estate Assets for Long-Term Wealth Letter

A Liquidating Real Estate Assets for Long-Term Wealth Letter is a strategic document used to initiate the conversion of property into liquid capital. Its primary goal is to facilitate portfolio rebalancing by selling underperforming holdings to fund more stable, high-yield investments. This process is essential for maintaining financial liquidity and ensuring sustainable growth. By formalizing the intent to sell, investors can optimize tax strategies and secure diversified wealth for the future. Clear communication in this letter ensures all stakeholders understand the transition toward long-term fiscal security.

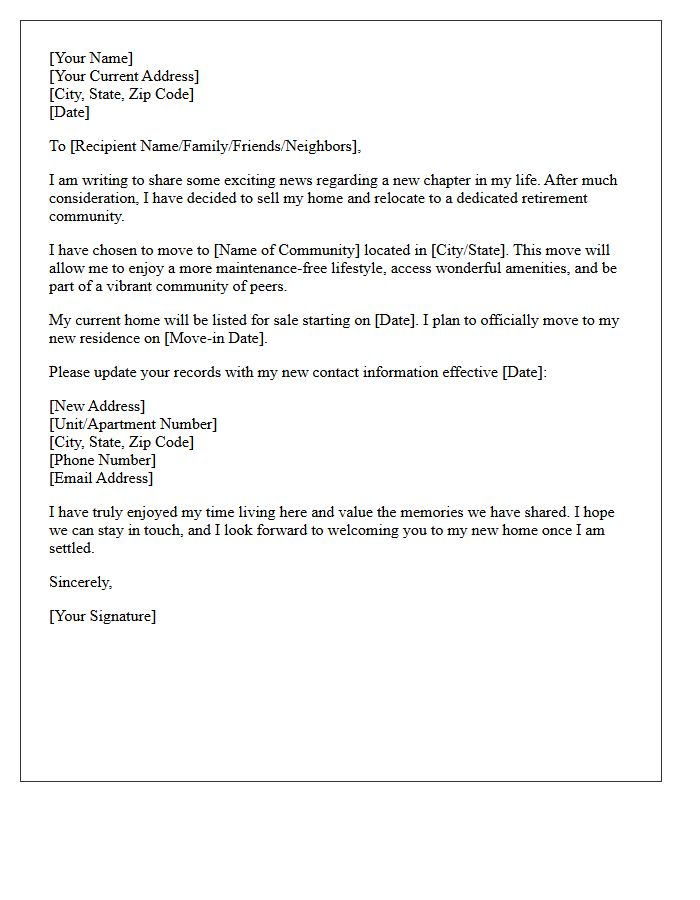

Selling and Relocating to a Dedicated Retirement Community Letter

A relocation letter notifies your network and professional services about your transition to a dedicated retirement community. It is essential to highlight your new contact information and the effective move date to ensure uninterrupted mail delivery and support. Clearly communicating your home sale status and downsizing plans helps streamline the logistical shift. Providing these details early allows family and service providers to adjust their records, ensuring a smooth transition into your new lifestyle while maintaining vital social and professional connections throughout the moving process.

What are the primary alternatives to a reverse mortgage mentioned in the retiree letter?

The primary alternatives include downsizing to a more affordable home, entering into a home equity sharing agreement, applying for a traditional Home Equity Line of Credit (HELOC), or exploring state-sponsored property tax deferral programs.

Can I access my home equity without taking out a new loan?

Yes, you can access equity without a loan through a sale-leaseback arrangement. This allows you to sell your home to an investor or specialized company and remain in the property as a tenant, providing immediate liquidity without monthly mortgage payments.

How does a Home Equity Investment (HEI) differ from a reverse mortgage?

Unlike a reverse mortgage, a Home Equity Investment (HEI) is not a loan and has no interest rates or monthly payments. Instead, an investor provides a lump sum in exchange for a share of the future appreciation of your home's value.

Are there government assistance programs for retirees to avoid debt?

Many local governments offer property tax exemptions or deferrals for seniors, which can significantly reduce monthly expenses. Additionally, the Section 504 Home Repair program provides grants to elderly homeowners to modernize their homes without moving.

Is downsizing a more cost-effective option than a reverse mortgage?

Downsizing is often more cost-effective because it eliminates the high closing costs and compounding interest associated with reverse mortgages. By selling a larger home and buying a smaller one in cash, retirees can eliminate debt and lower their ongoing maintenance and utility costs.

Comments