The final step of your real estate journey requires careful preparation to ensure a smooth transition. To avoid delays, you must organize your identification, financial documents, and keys before meeting your legal representative. Understanding Closing Day Instructions helps you manage expectations and complete the transaction successfully. To simplify your process, below are some ready to use template.

Image cover: The Ultimate Closing Day Checklist: Essential Documents, Templates, and Readiness Guide

Letter Samples List

- Closing Day Instruction Letter

- Valid Government Issued Photo Identification

- Certified Funds For Closing Costs

- Proof Of Active Homeowners Insurance

- Bank Wire Transfer Confirmation Receipt

- Personal Checkbook For Minor Incidental Fees

- Secondary Form Of Official Identification

- Final Property Walkthrough Approval Form

- Notarized Power Of Attorney Documents

- Original Executed Sales Contract Documents

- Required Spouse Or Co-Borrower Attendance

- Real Estate Agent Contact Information

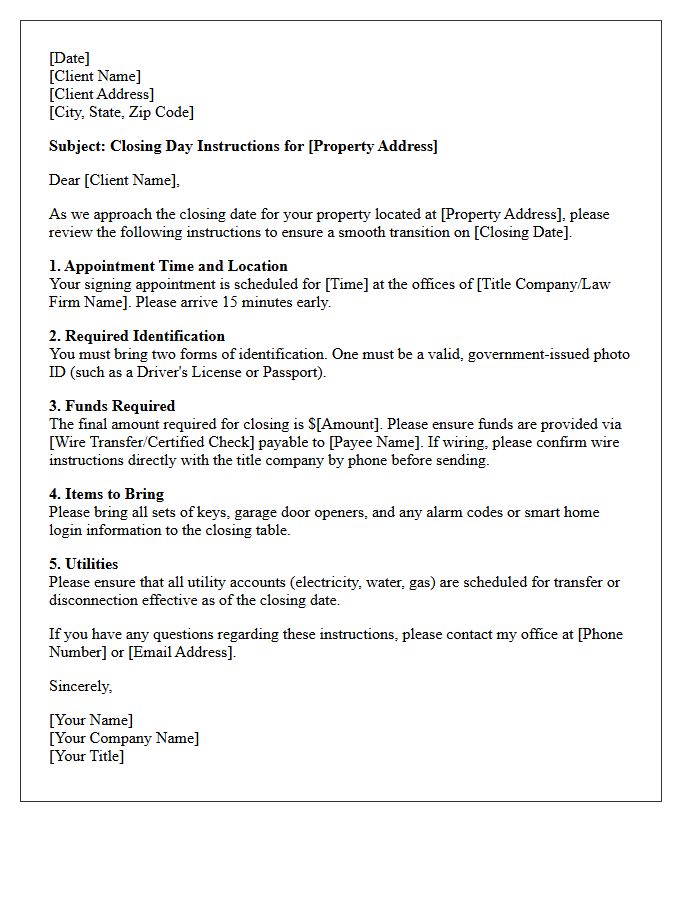

Closing Day Instruction Letter

The Closing Day Instruction Letter is a vital document outlining the final steps for completing a real estate transaction. It specifies wire transfer details, key pickup times, and mandatory identification requirements for all parties. Carefully reviewing these directives ensures the legal transfer of title occurs without delays. Buyers must strictly follow the provided financial protocols to prevent fraud and confirm the successful delivery of funds. Understanding these instructions is essential for a smooth settlement and the official handover of the property.

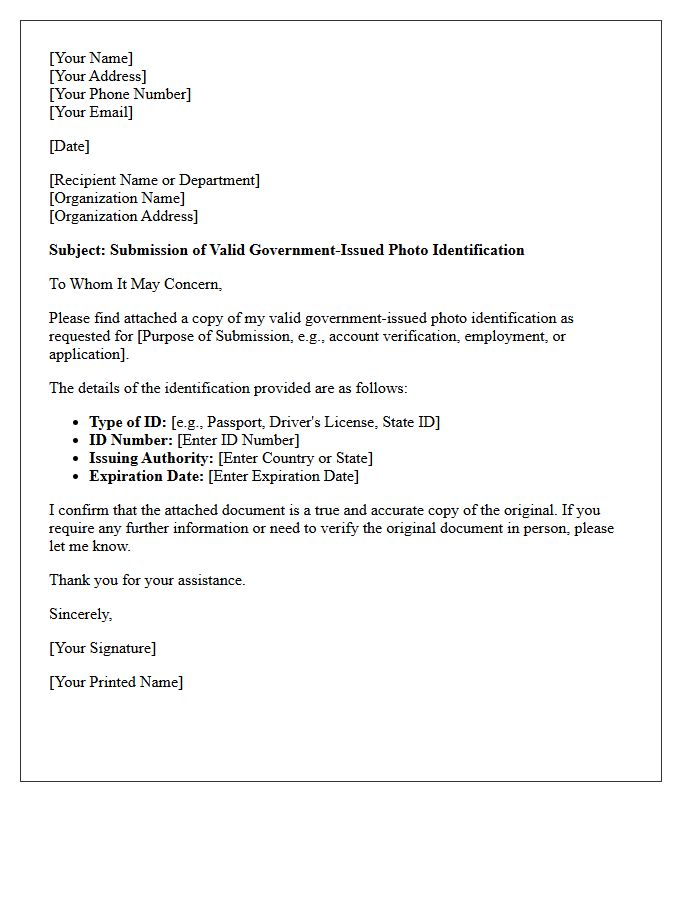

Valid Government Issued Photo Identification

A Valid Government Issued Photo Identification is an essential document used to verify your identity and legal status. To be considered valid, the ID must be current, unexpired, and issued by an authorized federal, state, or local government agency. Common examples include passports, driver's licenses, and military IDs. These documents must feature a clear, recognizable photograph and your full legal name. Maintaining a valid ID is critical for traveling, accessing restricted buildings, opening bank accounts, and completing official legal transactions securely.

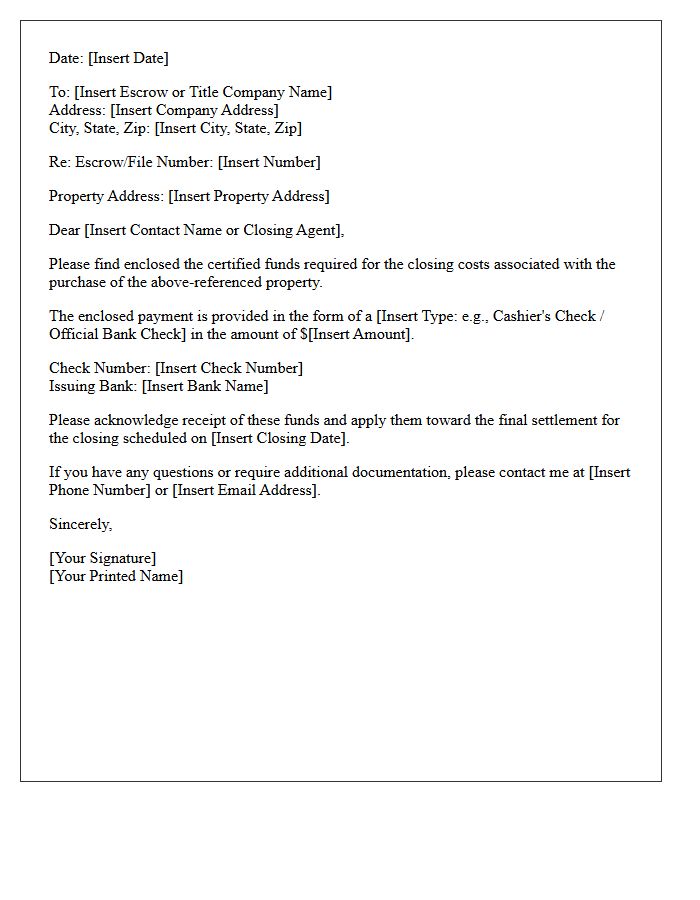

Certified Funds For Closing Costs

When finalizing a real estate transaction, you must provide certified funds to cover closing costs. These are guaranteed payment methods, such as a cashier's check or a wire transfer, verified by a financial institution to ensure the money is available. Unlike personal checks, these funds offer immediate security to the title company or escrow agent. It is crucial to confirm exact amounts and wiring instructions directly with your agent to avoid delays or potential fraud. Having these cleared funds ready ensures a smooth transfer of property ownership on your scheduled closing date.

Proof Of Active Homeowners Insurance

Providing Proof of Active Homeowners Insurance is a critical requirement for mortgage lenders to protect their financial interest in your property. This documentation, typically presented as an insurance declarations page, confirms that your policy is current and meets the minimum coverage standards. It verifies protection against hazards like fire, theft, and liability. Failure to maintain continuous coverage can result in force-placed insurance, which is often more expensive. Always ensure your lender is listed as the mortgagee on the policy to guarantee seamless compliance and financial security for your home.

Bank Wire Transfer Confirmation Receipt

A Bank Wire Transfer Confirmation Receipt serves as legal proof that a payment has been initiated. It contains critical details such as the SWIFT/BIC code, routing numbers, and the unique Federal Reference Number. This document is essential for tracking funds, resolving disputes, and notifying the recipient that capital is in transit. Always verify that the beneficiary's account information is accurate before finalizing the transaction, as wire transfers are often irreversible once processed by the financial institution.

Personal Checkbook For Minor Incidental Fees

Maintaining a personal checkbook for minor incidental fees ensures you are prepared for unexpected cash-only situations. While digital payments dominate, small costs like school activities, local permits, or documented reimbursements often require physical checks for proper record-keeping. Carrying a dedicated register helps you track these low-cost transactions accurately, preventing overdrafts and maintaining a clear paper trail for personal budgeting or tax purposes. Having a checkbook available remains a reliable backup for professional and organized handling of small, recurring financial obligations in environments that lack electronic payment infrastructure.

Secondary Form Of Official Identification

A secondary form of official identification is used to verify identity when a primary photo ID is unavailable or requires additional validation. Common examples include social security cards, birth certificates, utility bills, or voter registration cards. These documents are essential for administrative processes like opening bank accounts or applying for government services. While they often lack a photograph, they provide supplemental proof of name, address, or legal status. Always ensure these records are valid and issued by a recognized government body to satisfy compliance requirements during official verification procedures.

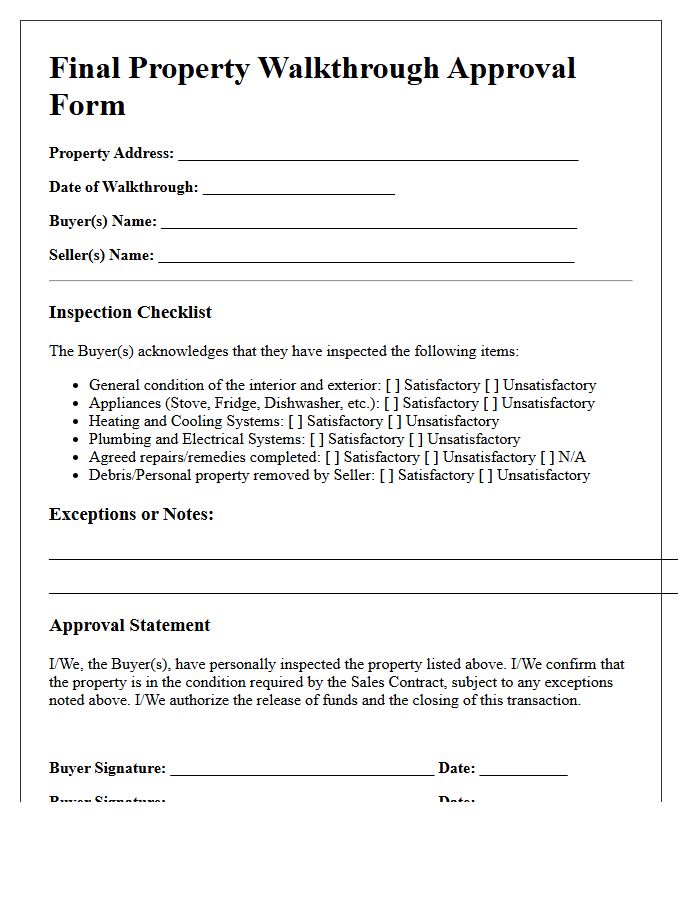

Final Property Walkthrough Approval Form

The Final Property Walkthrough Approval Form is a critical legal document used to confirm that a real estate asset remains in its agreed-upon condition before closing. Buyers use this form to verify that requested repairs are complete, no new damage exists, and all included fixtures are present. Signing this document signifies final acceptance of the property's state, often waiving the right to future claims. It ensures a transparent transition of ownership and protects both parties by formalizing the satisfactory inspection of the premises prior to the final fund transfer.

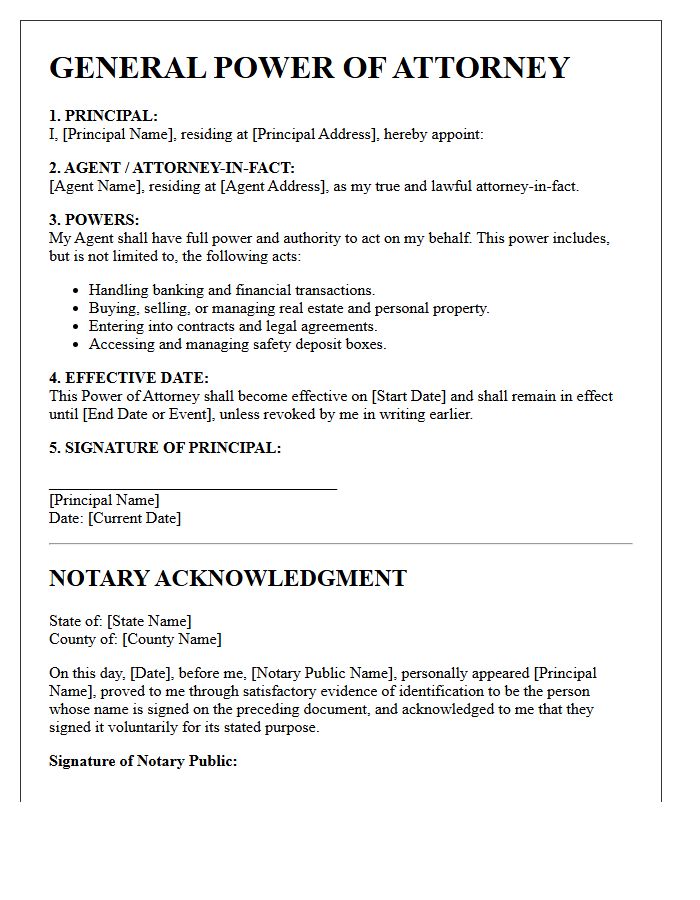

Notarized Power Of Attorney Documents

A Notarized Power of Attorney is a legal document granting an agent authority to act on a principal's behalf. To ensure its legal validity and prevent fraud, a notary public must verify the signer's identity and witness the signature. This process confirms the document was signed voluntarily and without duress. Requirements vary by jurisdiction, but notarization is often mandatory for financial and real estate transactions. Properly notarized documents provide security, ensuring that institutions recognize the agent's power to manage essential legal or medical affairs effectively.

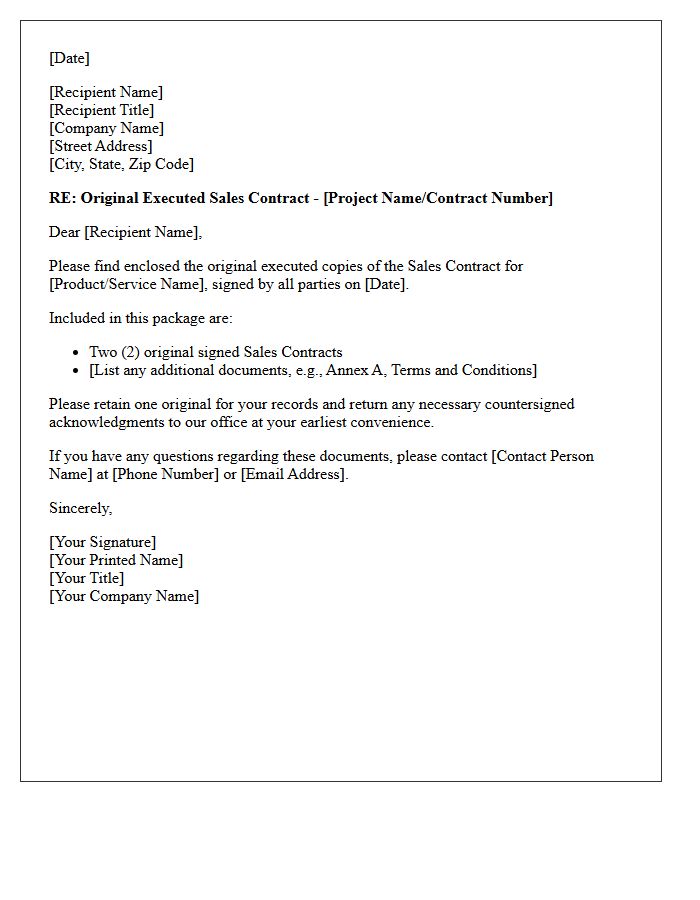

Original Executed Sales Contract Documents

The Original Executed Sales Contract is the primary legal instrument establishing a binding agreement between parties. It must feature authentic signatures from all stakeholders to be enforceable in court. Maintaining the physical or verified digital original is critical for evidentiary purposes during audits or disputes. This document outlines finalized terms, pricing, and obligations, superseding all prior verbal negotiations. Proper records management ensures that these definitive versions are securely stored, preserving their integrity as the ultimate legal reference for the transaction's lifecycle and compliance requirements.

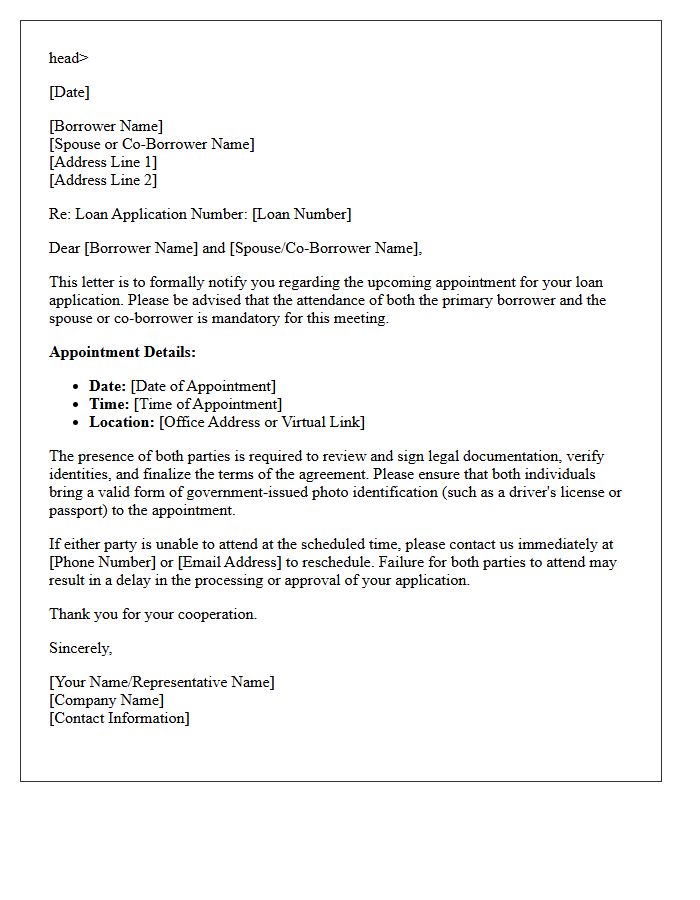

Required Spouse Or Co-Borrower Attendance

When applying for a mortgage or loan, spouse or co-borrower attendance is typically mandatory during the final signing session. Legal regulations often require all parties listed on the title or loan documents to be present to verify identities and execute binding contracts. If a co-signer cannot attend in person, a formal Power of Attorney (POA) must be approved by the lender in advance. Ensuring everyone is available prevents funding delays and guarantees that all ownership rights and financial obligations are legally acknowledged by both parties.

Real Estate Agent Contact Information

When searching for property, verify a Real Estate Agent's license number to ensure legal compliance. Reliable contact information must include their full legal name, registered brokerage, and a professional email address. Always confirm their identity through official agency websites before sharing sensitive data or making payments. This verification prevents fraud and guarantees you are working with a qualified professional. Keep a digital record of all correspondence to maintain clear communication transparency during the buying or selling process.

What documents do I need to bring to my real estate closing?

You must bring a valid government-issued photo ID (such as a driver's license or passport) and any outstanding paperwork requested by your lender or title company. If you are married, check with your escrow officer to see if your spouse is required to attend and sign documents as well.

How should I provide the funds required for my closing costs and down payment?

Most title companies require funds to be provided via a wire transfer or a certified cashier's check. Personal checks and cash are typically not accepted for closing costs. Ensure you confirm the exact amount and wiring instructions with your closing agent at least 24 hours in advance to avoid delays.

What happens during the final walkthrough before closing?

The final walkthrough usually takes place 24 to 48 hours before closing. This is your opportunity to verify that the property is in the agreed-upon condition, that all negotiated repairs were completed, and that the seller has vacated the premises while leaving behind any items included in the sale contract.

Who is required to attend the closing meeting?

Typically, all buyers listed on the mortgage and title must be present to sign the legal documents. Depending on your location, the meeting may also include your real estate agent, a representative from the title company or an escrow officer, and sometimes an attorney or the sellers.

What can I expect during the actual closing appointment?

During the appointment, you will review and sign a variety of legal documents, including the Closing Disclosure, the mortgage note, and the deed of trust. Once the paperwork is signed and the lender funds the loan, you will receive the keys and legal possession of your new home.

Comments