Lenders must inform borrowers when Flood Insurance Mandatory Purchase requirements apply to a property in a Special Flood Hazard Area. This essential notification ensures compliance with federal law and protects homeowners from financial loss during disasters. Understanding your legal obligations and timing requirements is critical for a smooth loan closing process. Below are some ready to use template.

Image cover: Essential Templates and Samples for Mandatory Flood Insurance Notifications

Letter Samples List

- Initial Mandatory Flood Insurance Purchase Notification Letter

- Second Request for Mandatory Flood Insurance Purchase Letter

- Final Warning of Mandatory Flood Insurance Requirement Letter

- Special Flood Hazard Area Designation Notification Letter

- Lender Required Flood Insurance Placement Letter

- Force-Placed Flood Insurance Impending Action Letter

- Proof of Flood Insurance Coverage Request Letter

- Notice of Insufficient Flood Insurance Coverage Letter

- National Flood Insurance Program Compliance Letter

- Private Flood Insurance Policy Evaluation Letter

- Mandatory Flood Insurance Policy Renewal Reminder Letter

- Flood Insurance Requirement Acknowledgment Letter

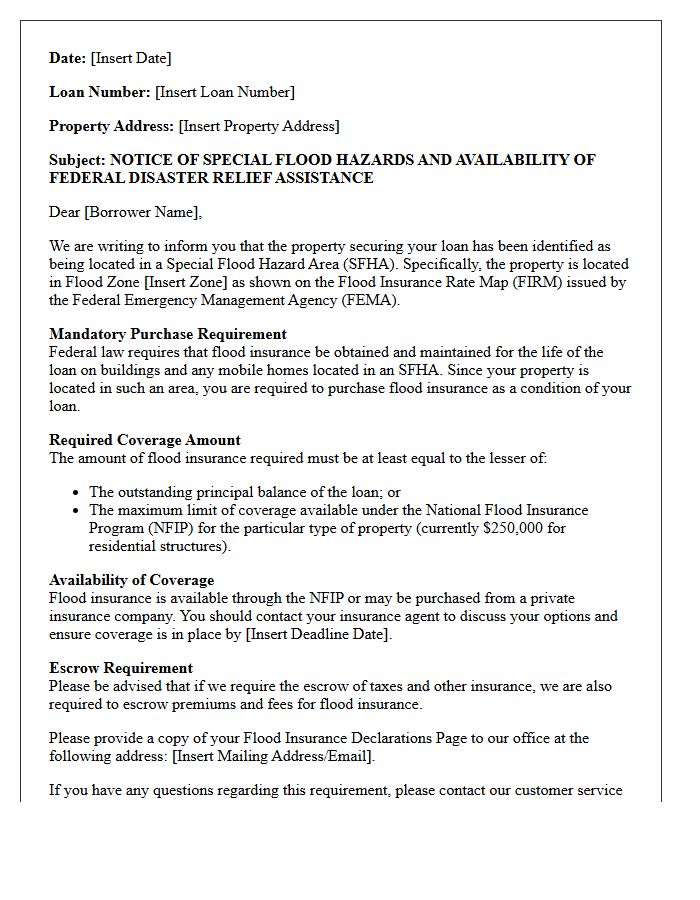

Initial Mandatory Flood Insurance Purchase Notification Letter

The Initial Mandatory Flood Insurance Purchase Notification Letter is a critical legal document sent by lenders to borrowers. It serves as formal notice that a property is located in a Special Flood Hazard Area (SFHA). Under federal law, homeowners must obtain and maintain adequate coverage to secure or maintain their mortgage. This letter outlines the compliance requirements, the amount of insurance needed, and the timeline for providing proof of policy. Failure to act may result in the lender force-placing insurance at the borrower's expense to protect the collateral.

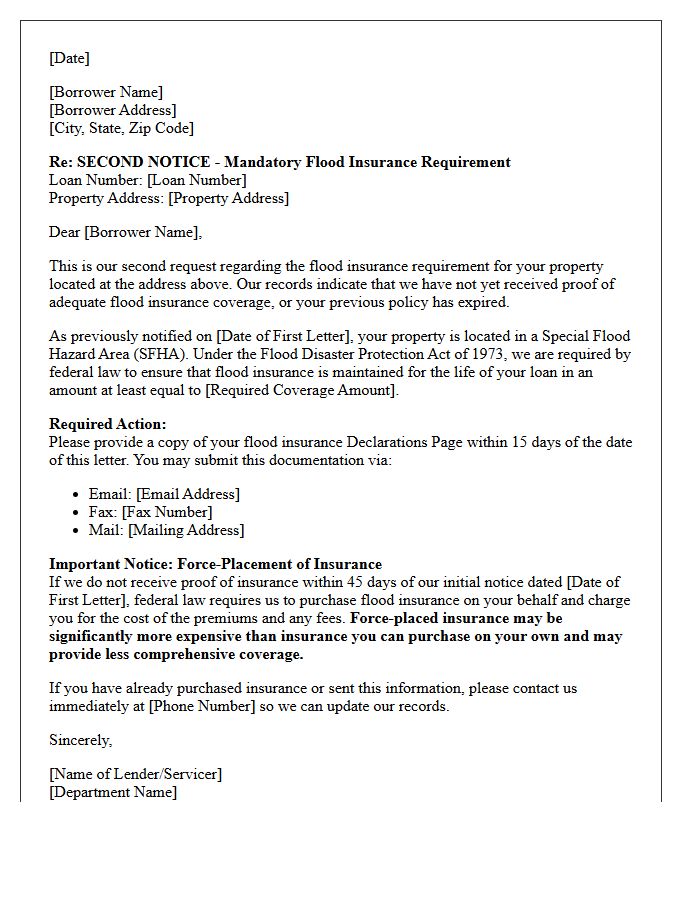

Second Request for Mandatory Flood Insurance Purchase Letter

A Second Request for Mandatory Flood Insurance Purchase Letter is a critical notification from your mortgage lender. It serves as a final warning that your property is located in a high-risk Special Flood Hazard Area and lacks required coverage. Failure to provide proof of flood insurance within the specified timeframe-typically 45 days-allows the lender to force-place a policy at your expense. These lender-placed policies are often significantly more expensive and provide less protection than private coverage. Prompt action is essential to maintain compliance and protect your financial interests.

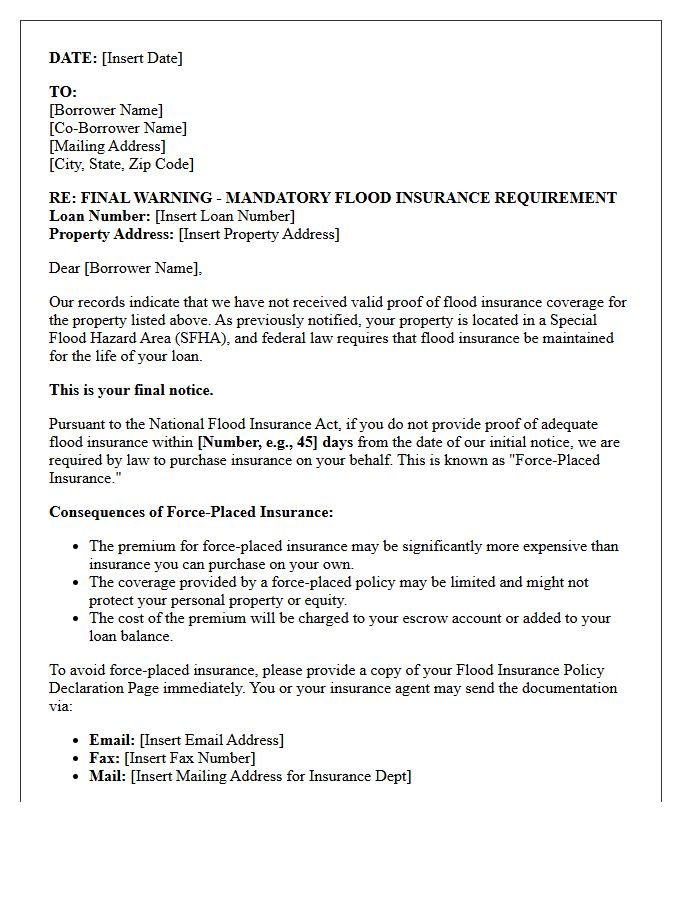

Final Warning of Mandatory Flood Insurance Requirement Letter

A Final Warning of Mandatory Flood Insurance Requirement Letter is a critical notice from your mortgage lender. It states that your property is in a Special Flood Hazard Area and lacks required coverage. Federal law mandates this insurance to protect the loan collateral. If you fail to provide proof of a policy within 45 days, the lender will force-place insurance, which is often significantly more expensive and offers limited protection. You must submit your policy declarations page immediately to ensure compliance and avoid costly, automatic premiums added to your mortgage.

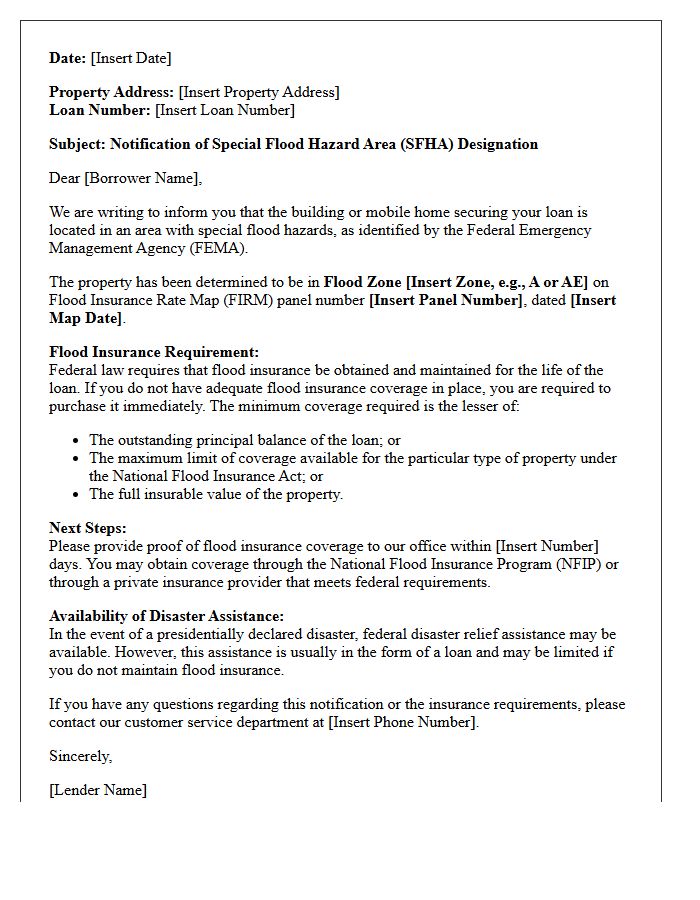

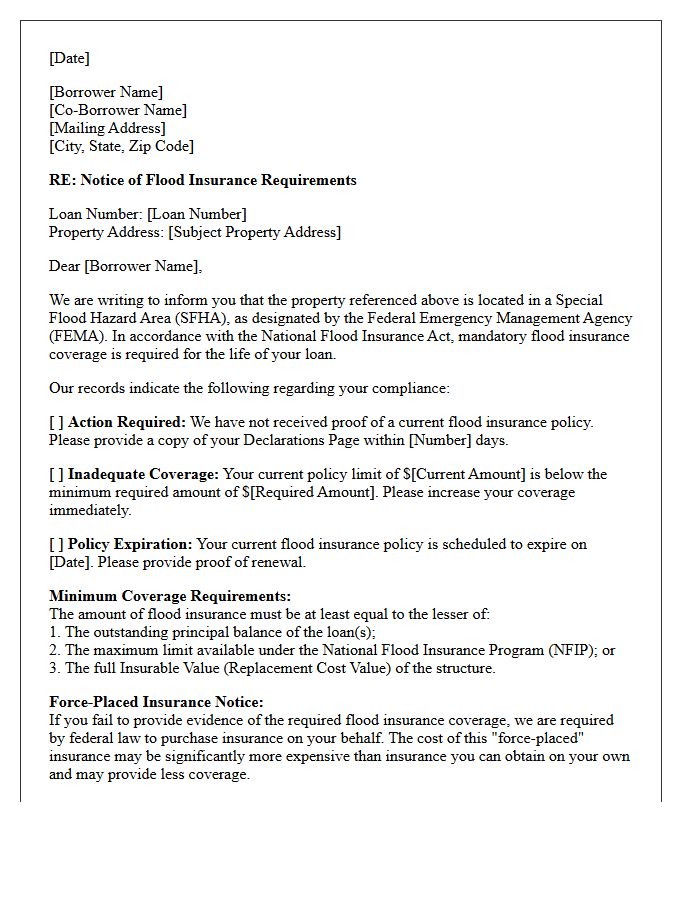

Special Flood Hazard Area Designation Notification Letter

A Special Flood Hazard Area Designation Notification Letter informs property owners that their building is located in a high-risk flood zone. This official notice indicates that mandatory flood insurance is required by federal law for federally backed mortgages. Receiving this document means your property has a 1% or greater annual chance of flooding according to FEMA maps. It is crucial to review your elevation certificate and insurance premiums immediately, as this designation directly impacts your property's financial obligations, safety requirements, and overall market value.

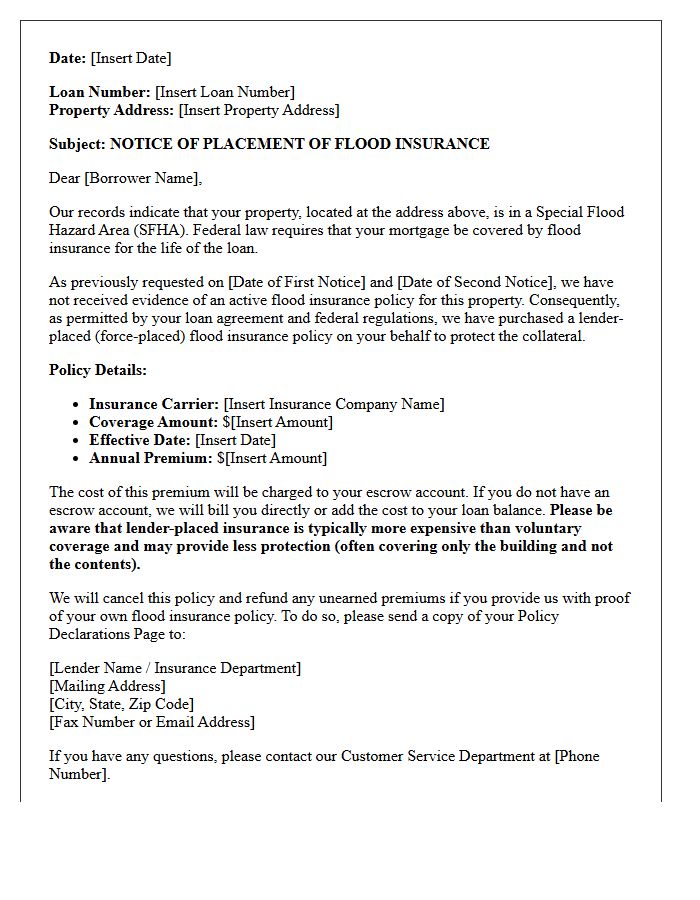

Lender Required Flood Insurance Placement Letter

A lender-required flood insurance placement letter is a formal notice sent when a property lacks mandatory flood coverage. If a borrower fails to maintain a policy in high-risk zones, the lender will force-place insurance to protect their financial interest. This coverage is often significantly more expensive and provides limited protection compared to private policies. It is crucial to provide proof of insurance immediately to avoid these costs. Borrowers should act quickly to secure their own voluntary policy to ensure comprehensive property protection and lower annual premiums.

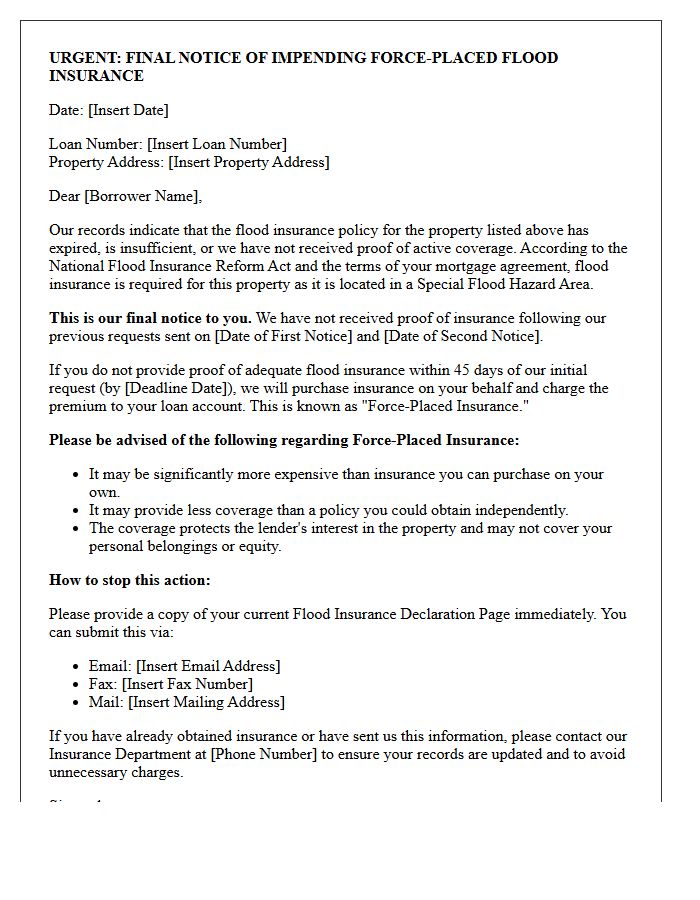

Force-Placed Flood Insurance Impending Action Letter

A Force-Placed Flood Insurance Impending Action Letter is a formal notice sent by your mortgage lender when your property lacks required flood coverage. It serves as a final warning that you have 45 days to provide proof of insurance. If you fail to act, the lender will legally purchase a policy on your behalf and charge you the premiums. This coverage is often significantly more expensive and provides less protection than private policies. To avoid these high costs, immediately provide your policy declarations page to your lender to prove active coverage.

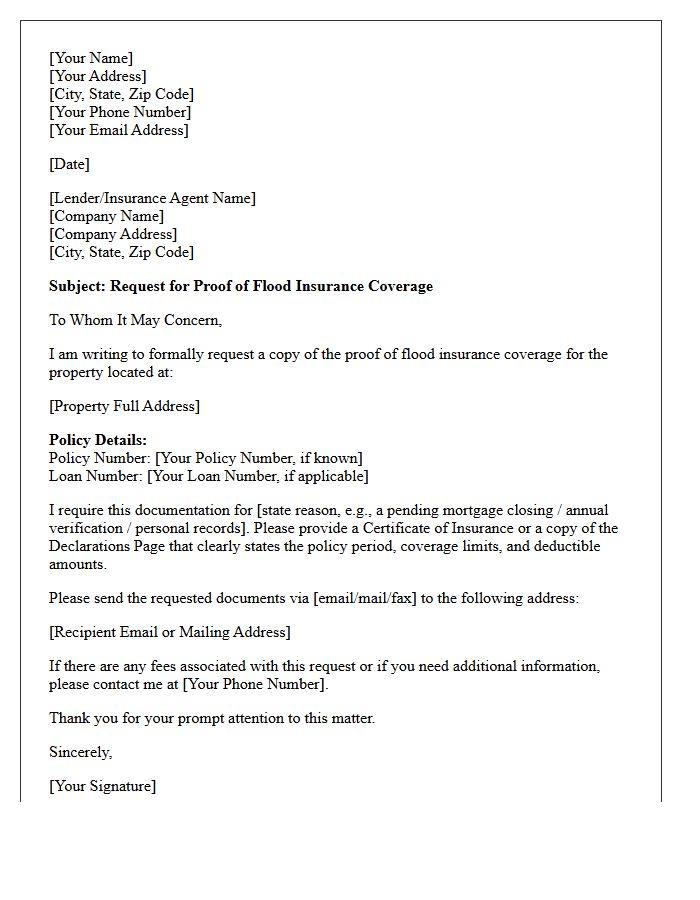

Proof of Flood Insurance Coverage Request Letter

A Proof of Flood Insurance Coverage Request Letter is a formal document sent to an insurance provider to verify active protection against water damage. It is essential for mortgage lenders to ensure the property meets compliance requirements and federal mandates. The letter must include the policy number, property address, and coverage limits. Providing this official certification prevents delays in loan processing and protects your financial investment from unexpected natural disasters. Always confirm the Declaration Page is attached to satisfy legal and lending obligations efficiently.

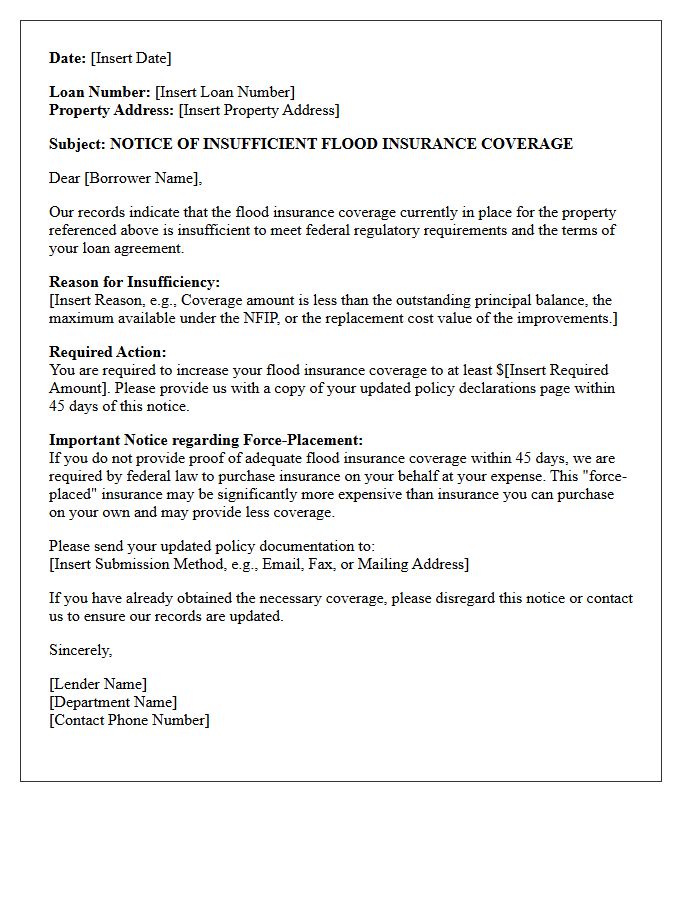

Notice of Insufficient Flood Insurance Coverage Letter

A Notice of Insufficient Flood Insurance Coverage is a critical legal alert from your lender stating that your current policy does not meet federal mandatory purchase requirements. This typically occurs if your coverage limits are lower than your outstanding loan balance or the property's replacement cost. Upon receiving this letter, you have a 45-day grace period to increase your coverage. Failure to comply allows the lender to force-place a policy, which is often significantly more expensive and provides less protection than private insurance or NFIP plans.

National Flood Insurance Program Compliance Letter

A National Flood Insurance Program (NFIP) Compliance Letter is a formal document verifying that a property adheres to federal floodplain management regulations. Lenders often require this to ensure the structure meets minimum elevation standards and safety requirements within high-risk zones. Obtaining this letter confirms your eligibility for NFIP coverage and helps determine accurate insurance premiums. It serves as essential proof for mortgage approval and long-term flood risk mitigation, protecting both the property owner and the lender from potential financial loss due to environmental hazards.

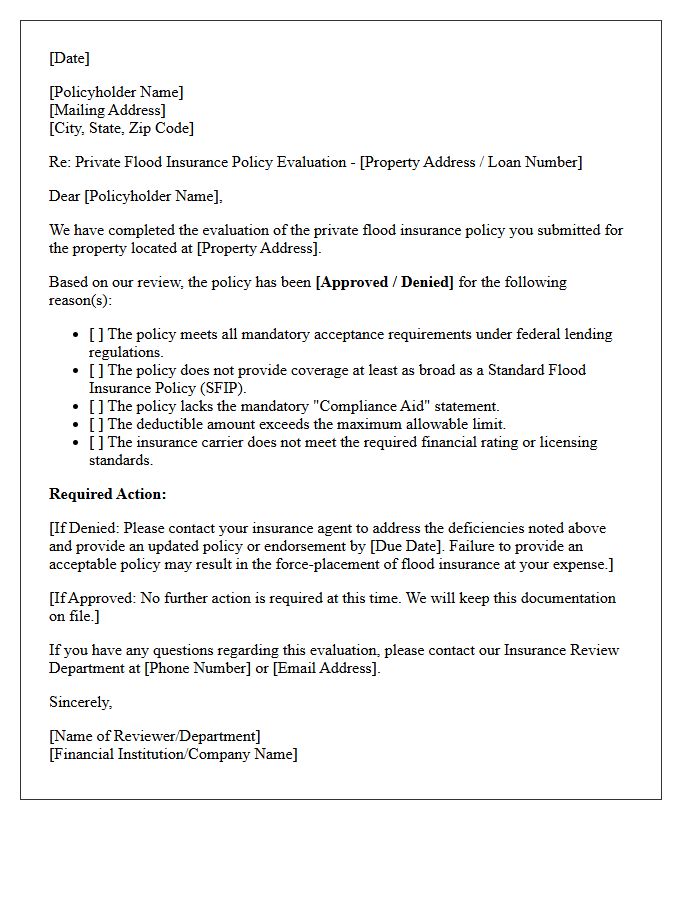

Private Flood Insurance Policy Evaluation Letter

A Private Flood Insurance Policy Evaluation Letter is a formal document issued by lenders to confirm that a non-NFIP policy meets federal mandatory purchase requirements. This assessment ensures the coverage provides compliance with statutory standards, such as being at least as broad as a standard government policy. For homeowners, this letter is critical for loan approval, as it verifies that the private insurer has the financial strength and specific provisions necessary to protect the property against water damage in high-risk zones.

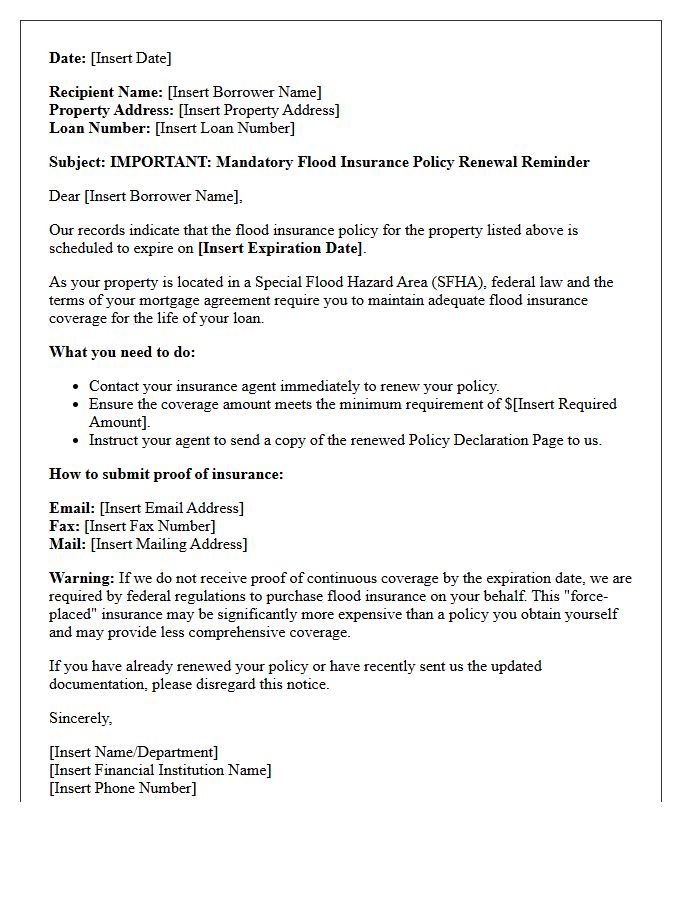

Mandatory Flood Insurance Policy Renewal Reminder Letter

Receiving a Mandatory Flood Insurance Policy Renewal Reminder Letter is critical for maintaining financial protection. This notice confirms that your property resides in a high-risk zone where coverage is a legal requirement for federally backed mortgages. Failure to renew by the expiration date can lead to a lapse in coverage, potential force-placed insurance by your lender, and loss of eligibility for disaster assistance. Always review your premium details and renewal deadlines immediately to ensure continuous protection against rising water damage and to comply with your loan agreement.

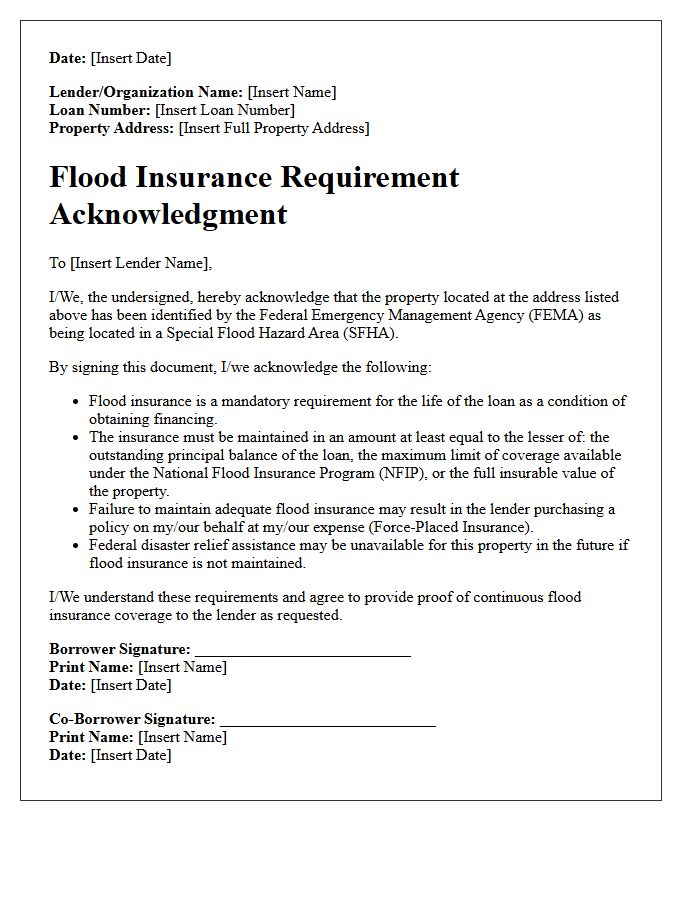

Flood Insurance Requirement Acknowledgment Letter

A Flood Insurance Requirement Acknowledgment Letter is a mandatory document confirming that a borrower understands their property is in a Special Flood Hazard Area. Lenders require this signed disclosure to ensure compliance with federal law before closing a mortgage. It serves as formal proof that the homeowner is aware of the mandatory coverage obligations and the financial risks associated with potential flooding. Failing to maintain this insurance policy can lead to lender-placed coverage or loan default, making this acknowledgment a critical component of the real estate closing process.

What is a Flood Insurance Mandatory Purchase Notification?

A Flood Insurance Mandatory Purchase Notification is a formal notice sent by a lender to a borrower informing them that their property is located in a Special Flood Hazard Area (SFHA) and that federal law requires them to obtain and maintain flood insurance as a condition of their mortgage.

When is flood insurance mandatory for a property?

Flood insurance is mandatory when a property is located in a high-risk flood zone (labeled with 'A' or 'V' on FEMA maps) and the loan is secured by a federally regulated lender or government-sponsored enterprise like Fannie Mae or Freddie Mac.

How long do I have to purchase flood insurance after receiving the notification?

Typically, property owners have 45 days from the date of the notification to provide proof of adequate flood insurance coverage. If coverage is not obtained within this timeframe, the lender is legally required to "force-place" a policy at the borrower's expense.

Does a Mandatory Purchase Notification mean my property will definitely flood?

The notification does not predict a specific event but indicates that the property is in a high-risk zone with at least a 1% annual chance of flooding. Statistically, there is a 26% chance of flooding over the course of a 30-year mortgage in these designated areas.

Can I appeal the mandatory flood insurance requirement?

If you believe your property was incorrectly mapped into a high-risk zone, you can apply for a Letter of Map Amendment (LOMA) through FEMA. However, you must continue to pay for flood insurance until the lender receives an official determination document from FEMA removing the requirement.

Comments