Facing mortgage default requires proactive steps to protect your home. This article explores how to initiate Good Faith Communication to negotiate a Forbearance Agreement with your lender. Learn how to demonstrate financial hardship and commitment to repayment to secure temporary payment relief and avoid foreclosure. To help you start the process, below are some ready to use template.

Image cover: Professional Forbearance Request Templates: Initiating Good Faith Mortgage Resolution

Letter Samples List

- Initial Proposal Letter for Mortgage Forbearance Agreement

- Good Faith Letter Proposing Temporary Mortgage Payment Forbearance

- Legal Counsel Letter Requesting Mortgage Default Forbearance

- Borrower Hardship Letter Proposing Mortgage Forbearance Agreement

- Good Faith Settlement Letter for Mortgage Default Forbearance

- Law Firm Representation Letter Proposing Forbearance Resolution

- Mortgage Arrears Forbearance Proposal Letter

- Pre-Foreclosure Good Faith Letter Proposing Forbearance

- Mutual Forbearance Agreement Proposal Letter

- Financial Hardship Explanation Letter Proposing Mortgage Forbearance

- Good Faith Negotiation Letter for Default Forbearance Terms

- Counsel to Counsel Letter Proposing Mortgage Forbearance Agreement

- Secured Property Forbearance Agreement Request Letter

- Mortgage Default Remediation Letter Proposing Forbearance

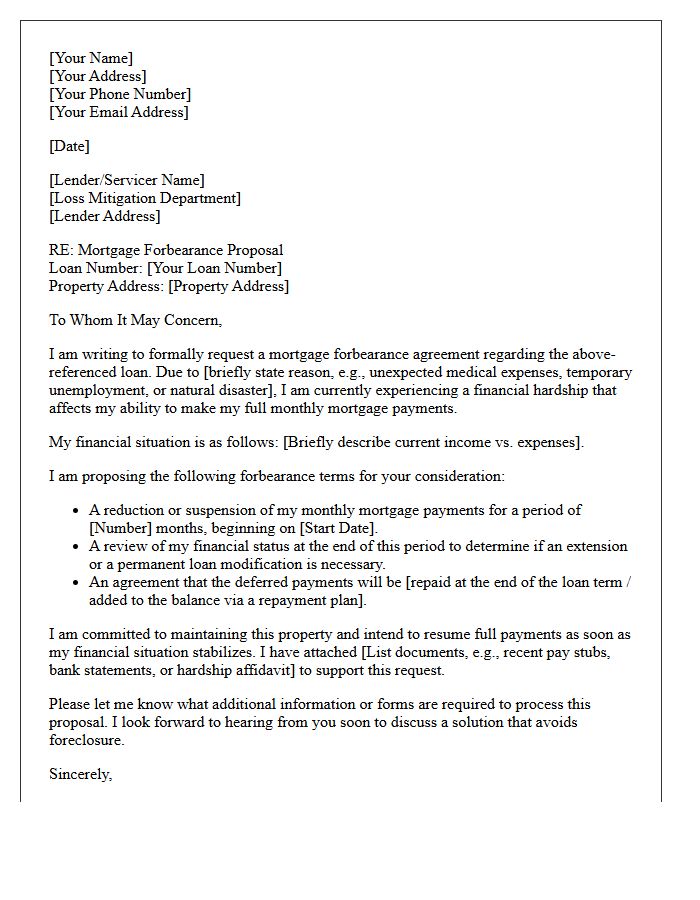

Initial Proposal Letter for Mortgage Forbearance Agreement

An Initial Proposal Letter for a mortgage forbearance agreement is a formal request sent to your lender to temporarily pause or reduce payments during financial hardship. This document should clearly state the reason for your distress, such as illness or job loss, and specify your requested terms and expected duration. Including supporting financial documentation demonstrates transparency and a commitment to future stability. Properly drafting this letter is the first step toward securing a legal agreement that prevents foreclosure while you work toward long-term financial recovery.

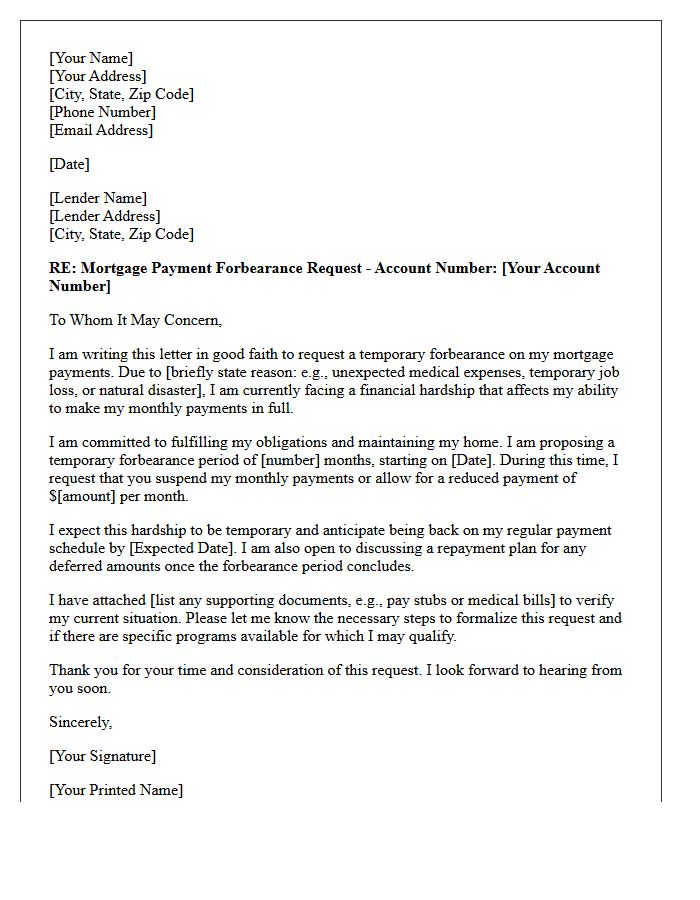

Good Faith Letter Proposing Temporary Mortgage Payment Forbearance

A Good Faith Letter is a formal request sent to lenders when facing financial hardship. It proposes a temporary mortgage payment forbearance to prevent immediate foreclosure. The document must clearly explain your situation, provide proof of reduced income, and outline a realistic plan for future repayment. By demonstrating a sincere intent to honor the debt, you open negotiations for a short-term grace period. This proactive communication is essential for maintaining a positive relationship with your creditor while seeking financial relief and long-term housing stability during unexpected crises.

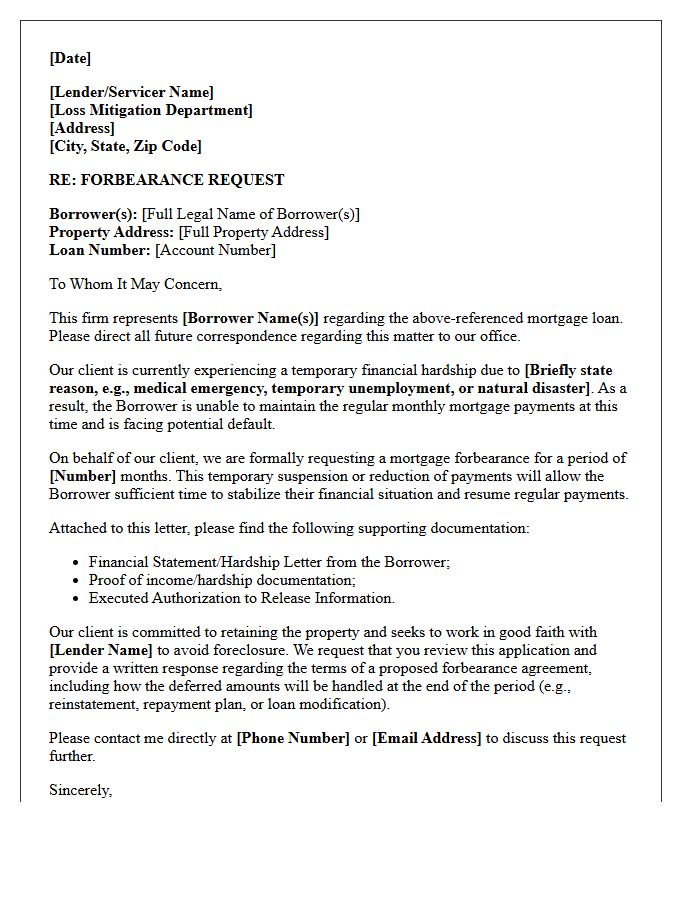

Legal Counsel Letter Requesting Mortgage Default Forbearance

A legal counsel letter requesting mortgage default forbearance is a formal hardship application drafted by an attorney to prevent foreclosure. This document highlights the borrower's financial instability while proposing a temporary repayment suspension or reduction. By leveraging legal expertise, the letter ensures all consumer protection rights are asserted under federal and state laws. It provides documented evidence of the intent to cure the default, encouraging lenders to negotiate a loan modification or formal forbearance agreement rather than pursuing costly legal action against the homeowner.

Borrower Hardship Letter Proposing Mortgage Forbearance Agreement

A borrower hardship letter is a formal request for mortgage forbearance, explaining financial distress like job loss or illness. To succeed, clearly outline your involuntary hardship, provide supporting documentation, and propose a specific timeline for reduced payments. Emphasize your commitment to reinstatement or a repayment plan once stability returns. Lenders prioritize transparent communication to evaluate eligibility for temporary relief. Keep the tone professional and concise to demonstrate a sincere intent to avoid default and maintain homeownership through an official forbearance agreement.

Good Faith Settlement Letter for Mortgage Default Forbearance

A Good Faith Settlement Letter is a formal proposal sent to lenders to resolve mortgage defaults. It demonstrates a sincere intent to cure arrears by offering a lump-sum payment or a structured repayment plan. This document is crucial for initiating forbearance, as it shows financial transparency and a commitment to avoid foreclosure. By outlining your hardship and a viable recovery strategy, you can negotiate temporary relief or permanent loan modifications. Providing clear financial evidence within this letter increases the likelihood of securing a mutually beneficial agreement with your servicer.

Law Firm Representation Letter Proposing Forbearance Resolution

A law firm representation letter proposing a forbearance resolution serves as a formal legal request to temporarily suspend or reduce payments. It signals that a debtor has retained professional counsel to negotiate a stay of enforcement or foreclosure actions. This document outlines the hardship, proposes a specific repayment timeline, and seeks to avoid litigation through a mutual agreement. Properly drafted, it protects the client's rights while providing a structured framework to restore financial stability and prevent immediate asset seizure or default judgments during the specified grace period.

Mortgage Arrears Forbearance Proposal Letter

A mortgage arrears forbearance proposal letter is a formal request to your lender for temporary payment relief. It must clearly outline your financial hardship, provide a detailed repayment plan, and demonstrate your commitment to long-term stability. Including a realistic income and expenditure breakdown is essential for approval. This document serves as a proactive step to prevent foreclosure by initiating negotiations for a formal forbearance agreement. Always send this letter early to show transparency and preserve your credit standing while seeking a manageable solution for your mortgage delinquency.

Pre-Foreclosure Good Faith Letter Proposing Forbearance

A pre-foreclosure good faith letter is a formal proposal sent to a lender to prevent foreclosure proceedings. Its primary purpose is to request forbearance, which allows a homeowner to temporarily pause or reduce mortgage payments during financial hardship. This document should clearly outline the cause of the delinquency and provide a realistic plan to resume full payments. Demonstrating transparency and a commitment to debt resolution increases the likelihood of approval. Acting early is essential to protect your credit and secure a workout agreement that keeps you in your home.

Mutual Forbearance Agreement Proposal Letter

A Mutual Forbearance Agreement Proposal Letter is a formal request sent to a lender to temporarily suspend or reduce loan payments during financial hardship. This document outlines a specific repayment plan to settle deferred amounts once the period ends. It serves as a critical negotiation tool to avoid foreclosure or default while maintaining a positive relationship with creditors. Clearly stating the hardship cause and proposing a viable timeline ensures both parties mitigate risks, providing financial stability without legal action or immediate asset loss.

Financial Hardship Explanation Letter Proposing Mortgage Forbearance

A financial hardship explanation letter is a formal document used to request mortgage forbearance by detailing specific circumstances impacting your ability to pay. To be effective, the letter must clearly outline the root cause of distress, such as job loss, medical emergency, or divorce. It should provide a specific timeline for recovery and propose a temporary suspension or reduction of payments. Maintaining a professional tone and attaching supporting evidence like bank statements or layoff notices increases the likelihood that your servicer will approve a temporary relief plan to avoid foreclosure.

Good Faith Negotiation Letter for Default Forbearance Terms

A Good Faith Negotiation Letter is a critical document used to initiate forbearance discussions when a borrower defaults. It serves as formal notice of the intent to resolve financial distress through cooperative restructuring rather than litigation. To be effective, the letter must clearly outline the hardship causing the default and propose realistic repayment terms or extension periods. Demonstrating transparency and a willingness to settle obligations helps preserve the professional relationship and may prevent immediate foreclosure or legal action, providing a structured pathway toward restoring the loan to good standing.

Counsel to Counsel Letter Proposing Mortgage Forbearance Agreement

A counsel to counsel letter proposing a Mortgage Forbearance Agreement serves as a formal legal negotiation to prevent foreclosure. This document outlines specific terms where a lender agrees to temporarily reduce or suspend payments due to a borrower's financial hardship. Key elements include the duration of the relief period, repayment structures for deferred amounts, and a waiver of immediate legal action. It is essential to clearly define reinstatement terms to ensure both parties understand the future obligations once the temporary arrangement expires, protecting the interests of the mortgagor and mortgagee.

Secured Property Forbearance Agreement Request Letter

A Secured Property Forbearance Agreement Request Letter is a formal proposal sent to a lender to temporarily pause or reduce mortgage payments during financial hardship. This document must clearly state the reason for distress and provide a specific timeline for resuming regular installments. Including financial documentation demonstrates transparency and a commitment to resolving the delinquency. Successfully negotiating this agreement prevents immediate foreclosure and preserves your legal rights to the property while you stabilize your finances. It is essential to ensure all modified terms are documented in writing to maintain clear legal protection.

Mortgage Default Remediation Letter Proposing Forbearance

A mortgage default remediation letter proposing forbearance is a critical formal request to pause or reduce payments during temporary financial hardship. This document should clearly outline the hardship reason, such as job loss or medical emergency, and provide a specific timeline for recovery. By proactively submitting this proposal, homeowners demonstrate a good-faith effort to avoid foreclosure. It serves as a vital negotiation tool to stabilize your housing situation while transitioning back to regular payment schedules through a structured repayment plan or loan modification later.

What is a good faith communication in the context of a mortgage forbearance request?

A good faith communication is a formal notification from a borrower to a lender that honestly discloses financial hardship, demonstrates an intent to repay the debt, and proposes a realistic plan to pause or reduce payments through a forbearance agreement.

How do I document financial hardship when proposing a forbearance agreement?

To establish good faith, provide clear documentation such as recent pay stubs, bank statements, medical bills, or an employer termination notice, accompanied by a hardship letter explaining why you are currently unable to meet your monthly mortgage obligations.

What should be included in a formal proposal for a mortgage forbearance agreement?

Your proposal should include your account information, a specific explanation of the temporary hardship, the requested duration of the forbearance, and a proactive suggestion for how you intend to catch up on missed payments once the period ends.

Does requesting a forbearance agreement stop the foreclosure process?

While a request alone does not legally halt foreclosure, initiating good faith communication often triggers loss mitigation protocols where lenders may voluntarily stay foreclosure proceedings while they evaluate your eligibility for a formal forbearance plan.

What are the typical repayment options following a mortgage forbearance period?

Common repayment structures include a reinstatement (lump sum), a repayment plan where extra amounts are added to monthly bills, or a loan modification which may extend the loan term or move the deferred payments to the end of the mortgage.

Comments