Receiving a Notice of Default marks the official beginning of the pre-foreclosure process. This legal document alerts homeowners that they have fallen behind on mortgage payments, providing a final window to resolve the debt before a public auction occurs. Understanding your rights during this critical phase is essential to saving your home. To assist you, below are some ready to use template.

Image cover: Essential Notice of Default and Pre-Foreclosure Letter Templates for Homeowners and Lenders

Letter Samples List

- Notice of Default Warning Letter

- Pre-Foreclosure Initiation Letter

- Mortgage Delinquency Notification Letter

- Intent to Foreclose Notice Letter

- Final Demand for Payment Letter

- Grace Period Expiration Letter

- Reinstatement Amount Quote Letter

- Short Sale Opportunity Letter

- Forbearance Agreement Proposal Letter

- Deed in Lieu of Foreclosure Offer Letter

- Loss Mitigation Options Letter

- Notice of Intent to Accelerate Loan Letter

- Breach of Promissory Note Letter

- Pre-Foreclosure Workout Solution Letter

- Delinquent Account Status Letter

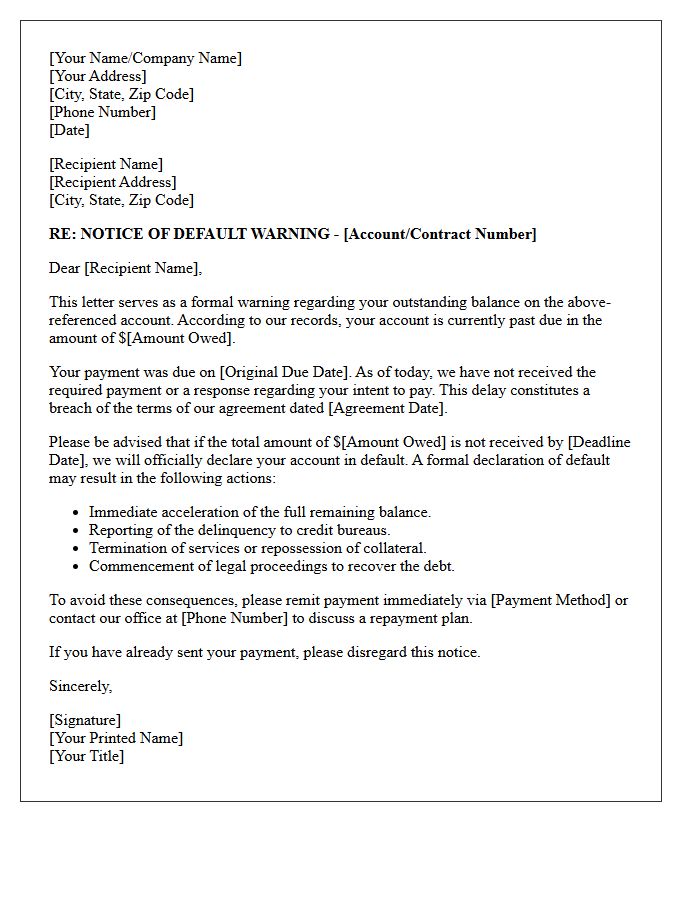

Notice of Default Warning Letter

A Notice of Default is a formal legal warning issued by a lender when a borrower falls behind on mortgage payments. Receiving this letter signifies the beginning of the foreclosure process. It provides a specific timeframe to pay the outstanding balance and legal fees to reinstate the loan. Ignoring this document can lead to the loss of your property. It is crucial to contact your loan servicer immediately to discuss loss mitigation options, such as loan modification or a repayment plan, to prevent further legal action.

Pre-Foreclosure Initiation Letter

A Pre-Foreclosure Initiation Letter, often called a Notice of Default, is a formal legal warning sent by lenders when mortgage payments are missed. This document signifies the beginning of the foreclosure process, outlining the total amount overdue and a specific deadline to pay. It is a critical window for homeowners to pursue loss mitigation options, such as loan modification or a short sale. Receiving this letter does not mean you have lost your home yet, but immediate action is required to prevent a public filing and protect your property rights.

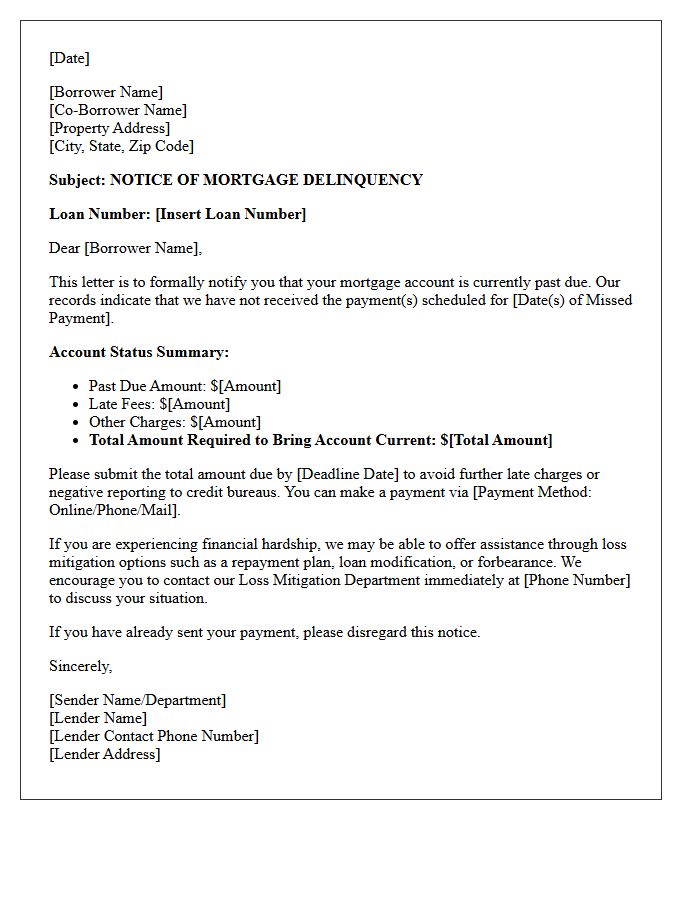

Mortgage Delinquency Notification Letter

A Mortgage Delinquency Notification Letter is a formal notice sent by lenders when a borrower misses a scheduled payment. This document serves as a legal warning that the loan is past due, outlining the total amount owed and any applicable late fees. It is crucial to address this notice immediately to explore loss mitigation options, such as loan modification or repayment plans. Ignoring this communication can accelerate the timeline toward foreclosure, significantly damaging your credit score and risking the loss of your property. Communication with your servicer is key.

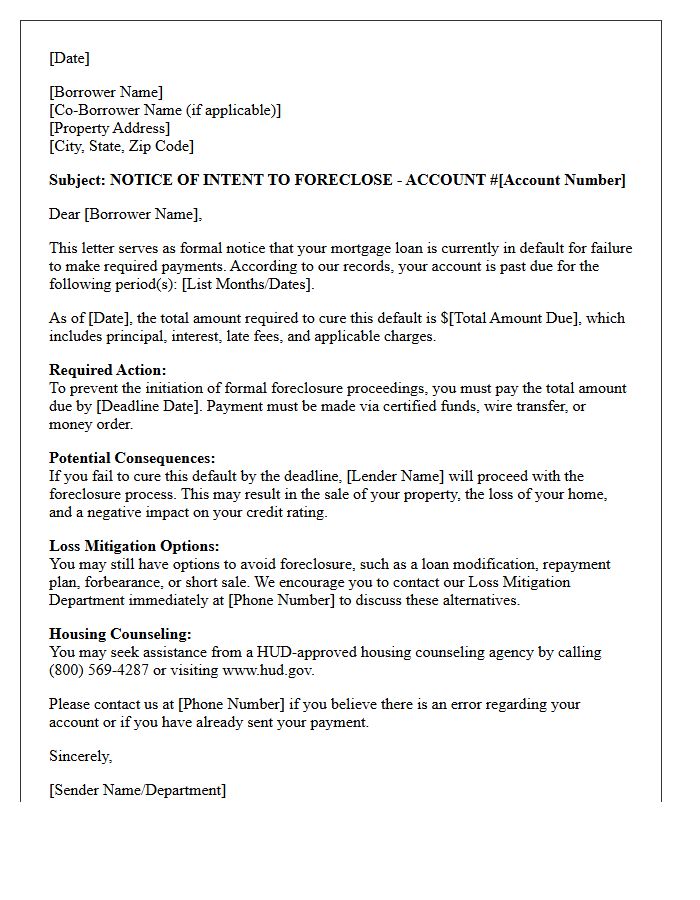

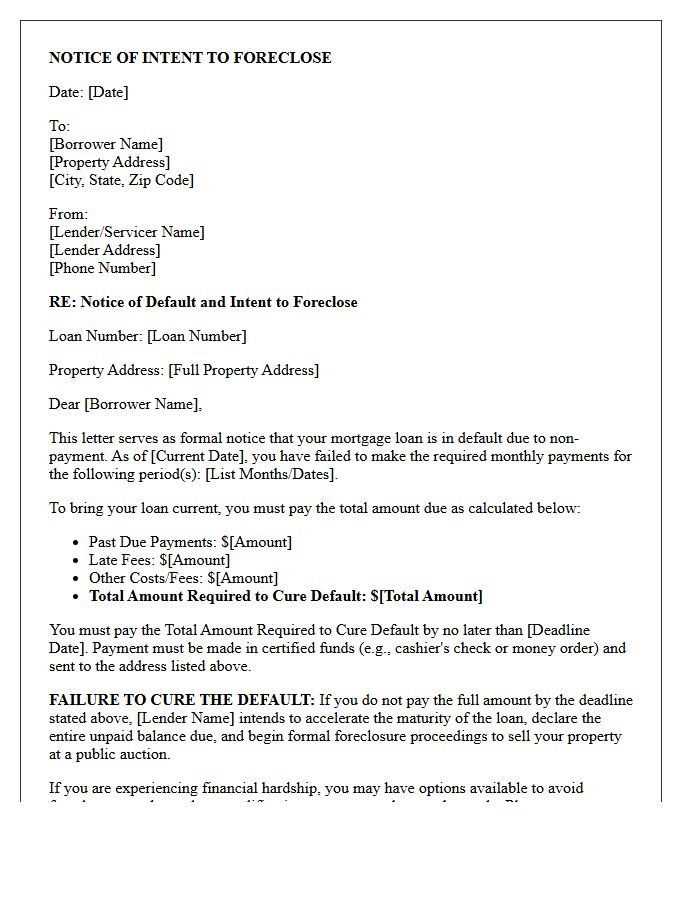

Intent to Foreclose Notice Letter

An Intent to Foreclose Notice Letter is a formal legal warning issued by a mortgage lender when a homeowner defaults on payments. This document serves as the final step before the official foreclosure process begins. It outlines the specific amount needed to cure the default, provides a deadline for payment, and explains your right to seek housing counseling. Receiving this letter is a critical warning; homeowners must act immediately to negotiate a loan modification or repayment plan to prevent losing their property to a public sale.

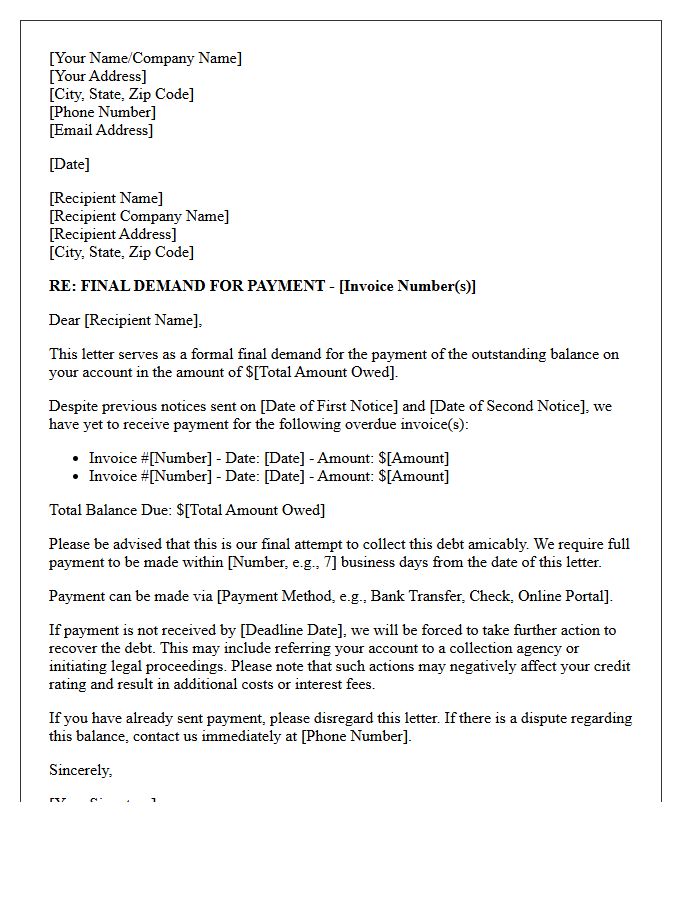

Final Demand for Payment Letter

A Final Demand for Payment Letter serves as a formal pre-legal notice sent to a debtor before initiating a lawsuit. This critical document clearly states the exact debt owed, established deadlines, and the specific consequences of non-payment. By providing a final opportunity to settle the balance, it demonstrates a good faith effort to resolve the dispute out of court. Properly drafted, this letter acts as vital evidence of communication during subsequent legal proceedings or debt collection actions, often motivating immediate payment to avoid costly litigation and legal fees.

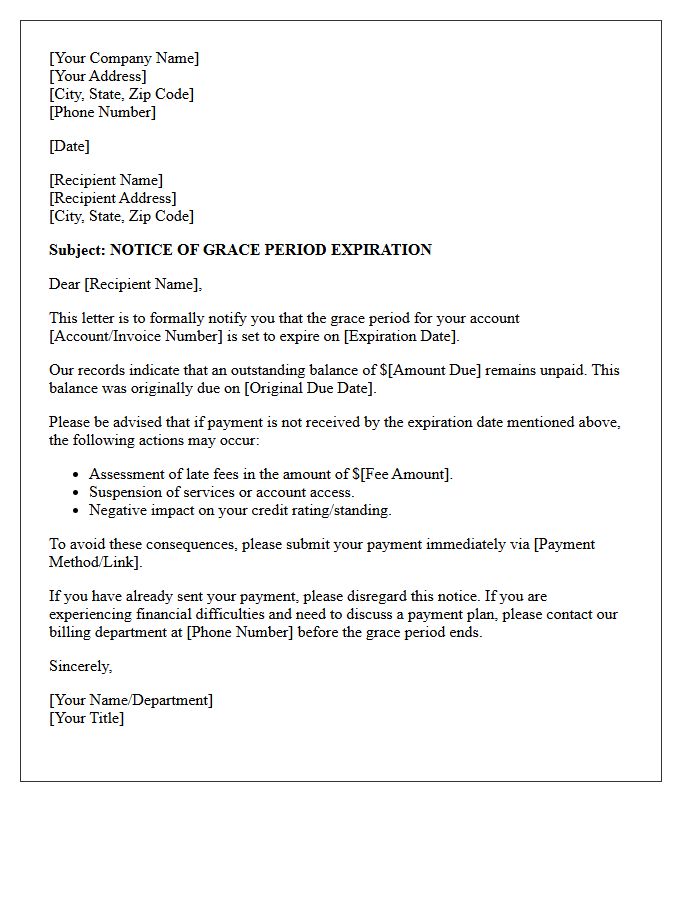

Grace Period Expiration Letter

A Grace Period Expiration Letter is a formal notification sent by lenders or service providers when a temporary payment extension is ending. This document serves as a critical final warning before late fees, interest penalties, or service interruptions occur. It outlines the exact date regular billing resumes and the total amount due to maintain good standing. Receiving this letter means your protected timeframe has concluded, making immediate financial action essential to avoid negative impacts on your credit score or policy cancellation.

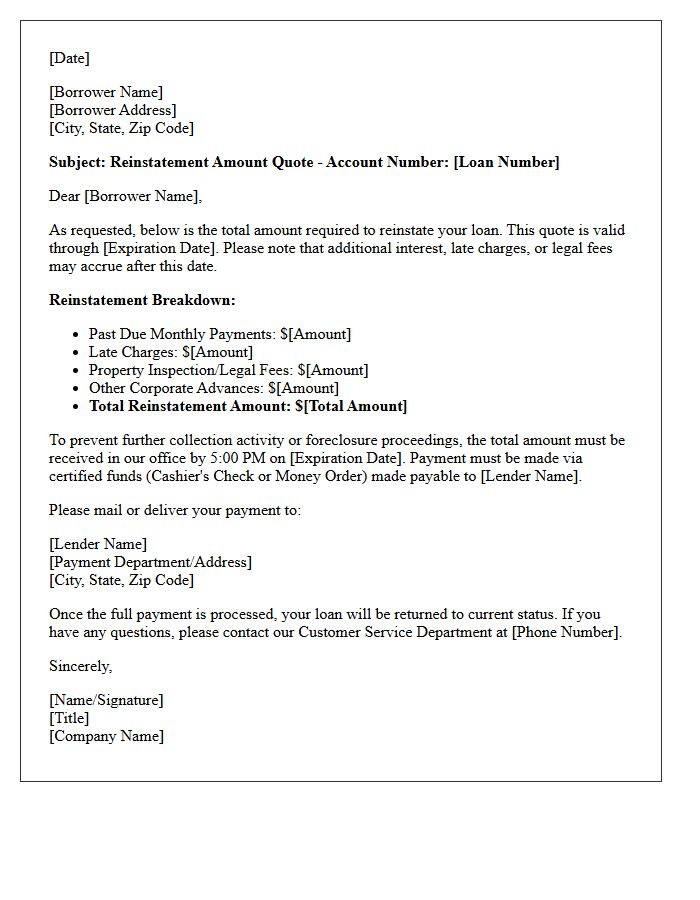

Reinstatement Amount Quote Letter

A Reinstatement Amount Quote Letter is a formal document from a mortgage lender outlining the exact total required to bring a delinquent loan current. It specifies the past-due payments, late fees, and legal costs accumulated during foreclosure proceedings. Homeowners must pay this specific amount by a strict deadline to stop legal action and restore the original loan terms. Obtaining this official quote ensures accuracy, as it prevents further penalties and provides a clear pathway to regaining financial standing and saving the property from a trustee sale.

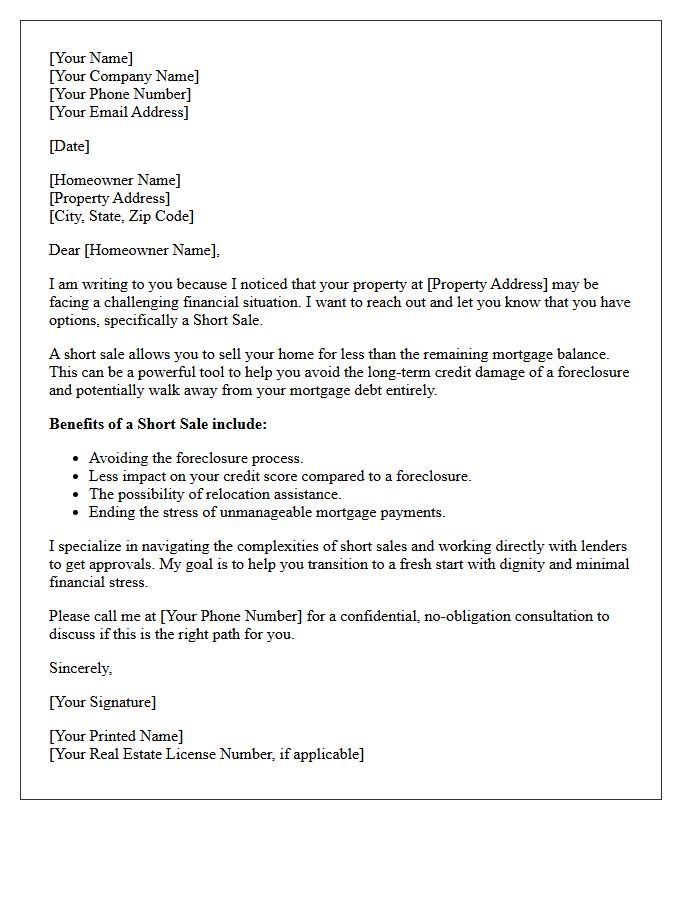

Short Sale Opportunity Letter

A short sale opportunity letter is a formal notification from a mortgage lender inviting a homeowner to sell their property for less than the remaining loan balance. This document acts as a pre-approval for a short sale, helping distressed borrowers avoid the severe consequences of foreclosure. It outlines specific incentives, such as relocation assistance or deficiency waivers, to encourage a voluntary exit. Receiving this letter indicates that the lender is willing to negotiate with buyers, making it a critical distressed property strategy for homeowners seeking debt relief and credit protection.

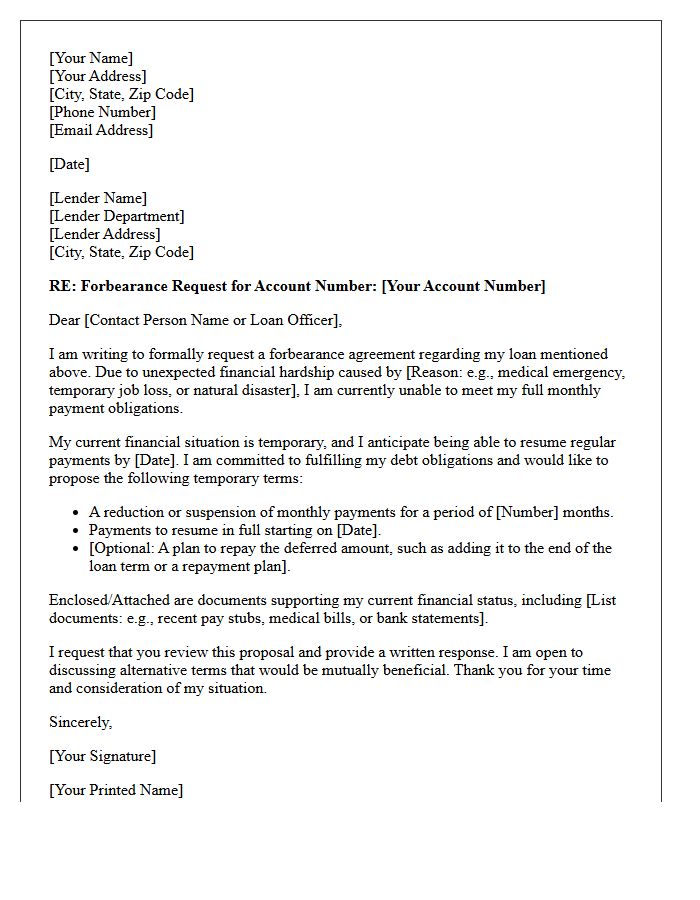

Forbearance Agreement Proposal Letter

A Forbearance Agreement Proposal Letter is a formal request from a borrower to a lender seeking temporary relief from loan payments during financial hardship. This document should clearly outline the financial hardship, propose a specific reduced payment schedule, and state a definitive end date. It serves as a critical first step to avoid foreclosure or default by demonstrating a proactive commitment to resolving debt. Ensuring the proposal is detailed and realistic increases the likelihood of reaching a mutually beneficial repayment plan while protecting the borrower's credit standing.

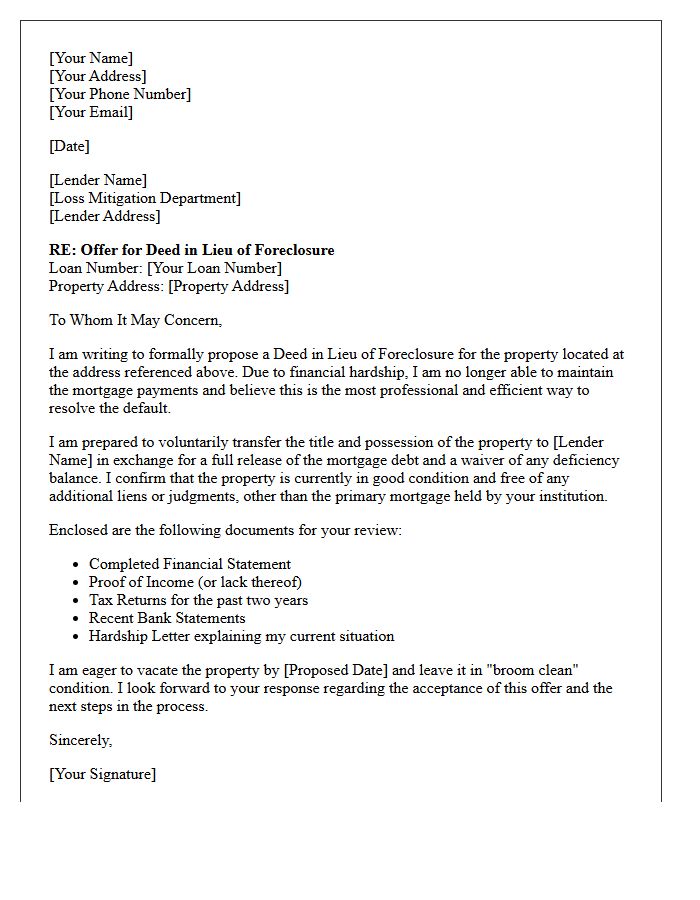

Deed in Lieu of Foreclosure Offer Letter

A Deed in Lieu of Foreclosure Offer Letter is a formal proposal sent to a lender to voluntarily transfer property ownership to avoid legal proceedings. This document highlights the borrower's inability to maintain payments due to financial hardship. If accepted, it helps preserve your credit score more effectively than a standard foreclosure and may release you from personal liability for the deficiency balance. It is essential to clearly state that the transfer is intended to satisfy the debt in full to ensure a complete lien release.

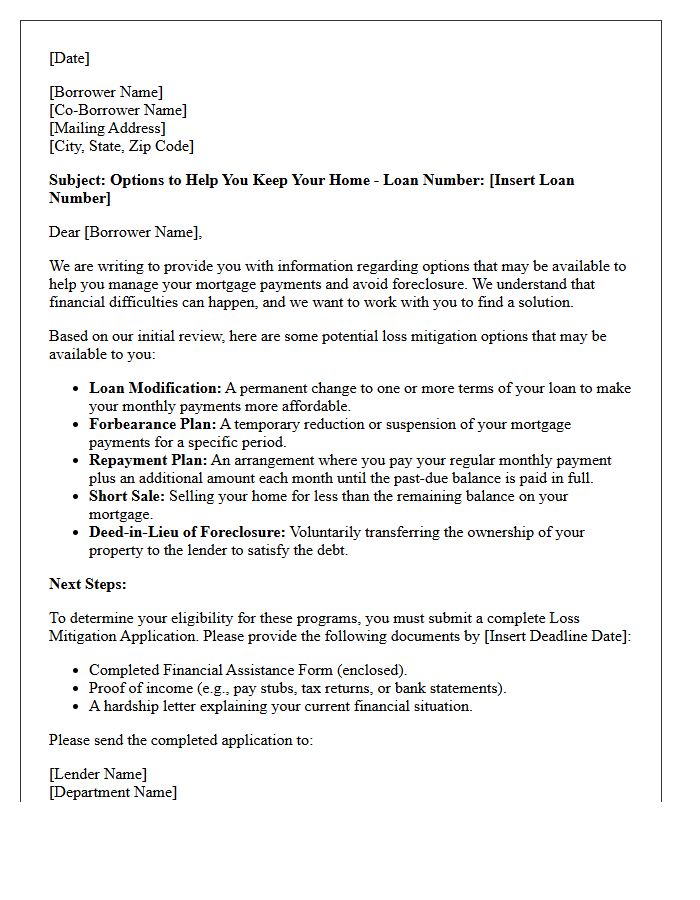

Loss Mitigation Options Letter

A Loss Mitigation Options Letter is a formal notice from your mortgage servicer outlining available alternatives to foreclosure. This document is critical when you face financial hardship, as it details specific solutions like loan modifications, repayment plans, or short sales. Borrowers must review the eligibility criteria and strict deadlines mentioned to protect their homeownership rights. Promptly responding to this letter allows you to initiate the evaluation process and potentially secure a more affordable payment structure, ensuring long-term housing stability and preventing legal action against your property.

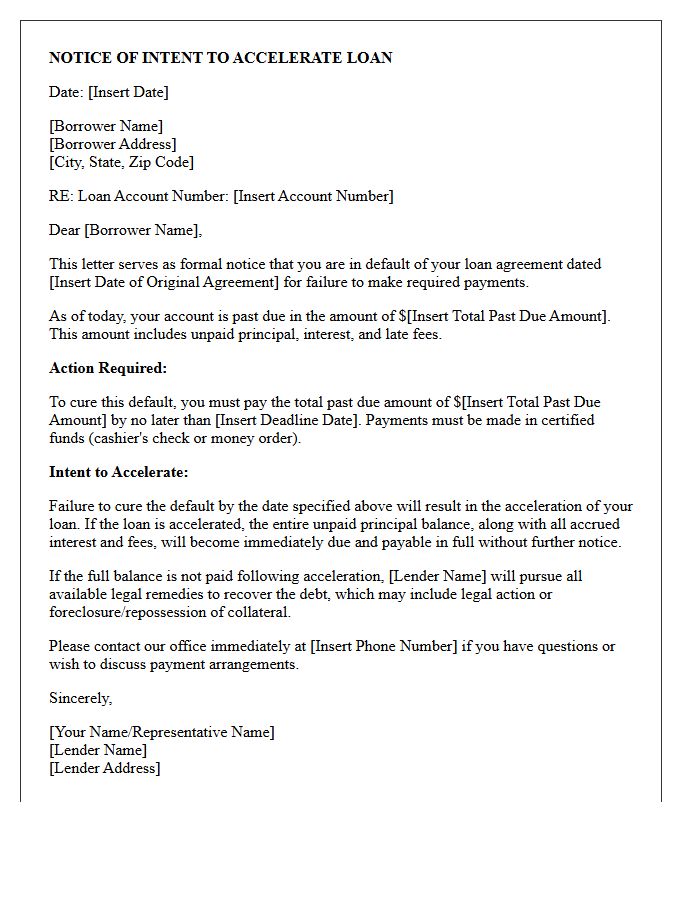

Notice of Intent to Accelerate Loan Letter

A Notice of Intent to Accelerate Loan Letter is a formal warning from a lender indicating that a borrower has defaulted on their mortgage contract. This document serves as a final opportunity to cure the default by paying the total overdue balance plus late fees within a specific timeframe. Failure to resolve the delinquency after receiving this notice typically triggers acceleration, making the entire loan balance due immediately and authorizing the lender to commence foreclosure proceedings against the property. Prompt action is essential to protect homeowner rights.

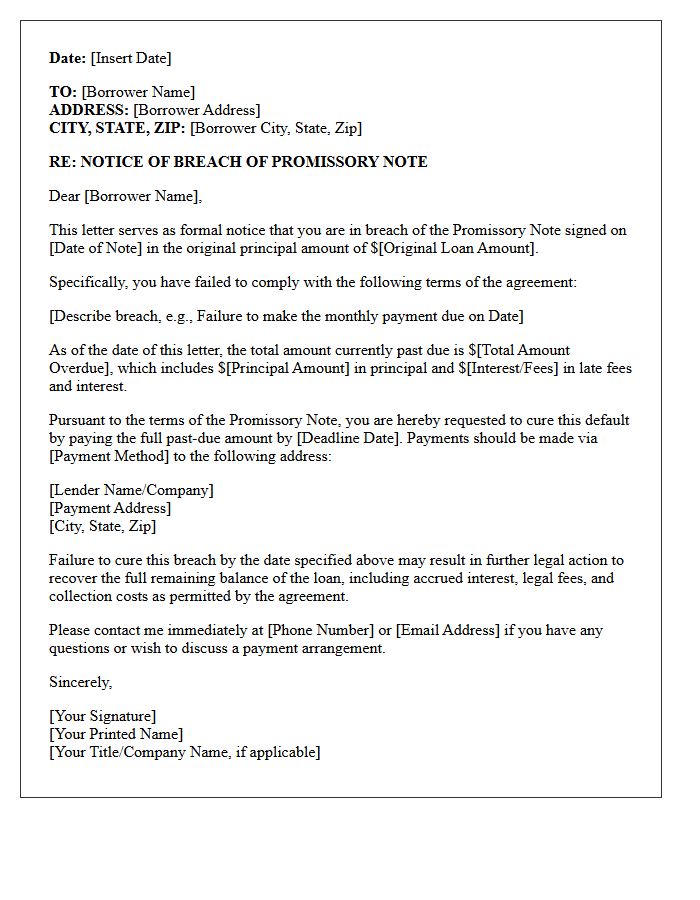

Breach of Promissory Note Letter

A Breach of Promissory Note Letter serves as a formal legal notice issued when a borrower fails to meet repayment obligations. This document officially notifies the debtor of their default, specifying the missed payments, accrued interest, and late fees. It acts as a critical prerequisite for potential litigation, providing evidence that the lender attempted to resolve the debt recovery process amicably. Clear communication regarding the outstanding balance and a final deadline for payment are essential elements to protect the lender's rights and strengthen any future legal claims in court.

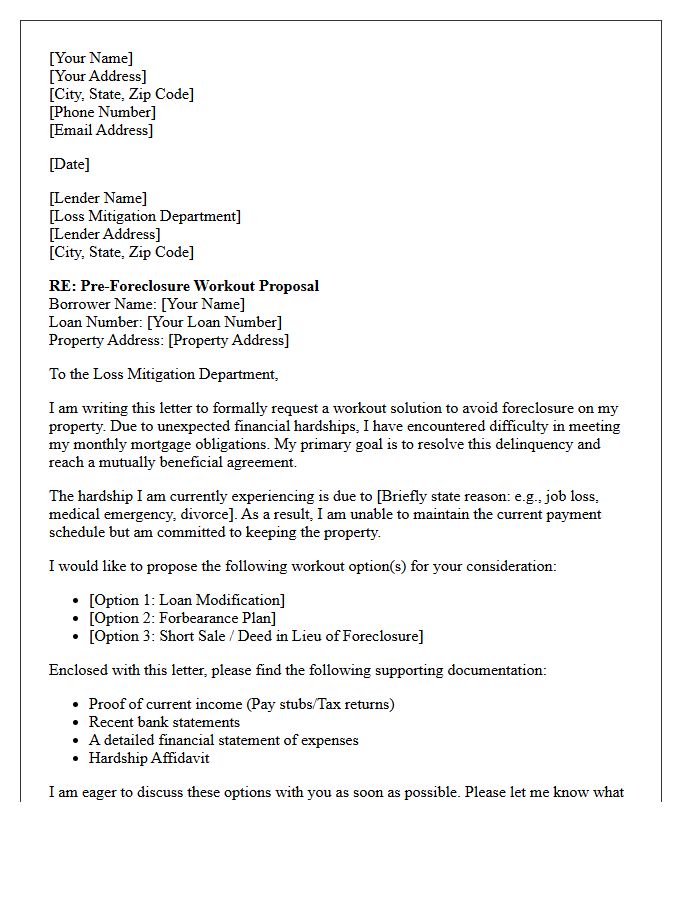

Pre-Foreclosure Workout Solution Letter

A Pre-Foreclosure Workout Solution Letter is a formal proposal sent to a mortgage lender to prevent property repossession. This document outlines the borrower's financial hardship while suggesting viable alternatives like a loan modification, short sale, or forbearance agreement. Its primary goal is to demonstrate a proactive intent to resolve delinquency and reach a mutual settlement. Providing clear financial documentation and a realistic repayment plan within this letter is essential for negotiating terms that allow the homeowner to retain their residence or exit the mortgage gracefully without a final foreclosure.

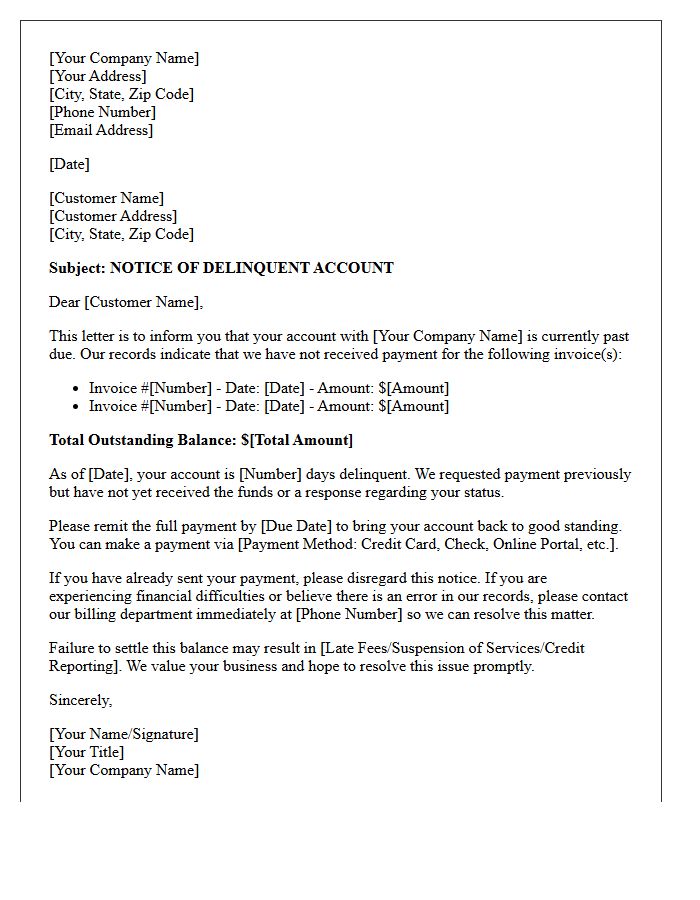

Delinquent Account Status Letter

A Delinquent Account Status Letter is a formal notification issued when a payment obligation remains unsatisfied past its due date. This document serves as a critical legal record of the default, outlining the outstanding balance, accumulated late fees, and a final deadline for remediation. Receiving this notice indicates that the creditor may escalate the matter to debt collection agencies or initiate legal action. To protect your credit score and avoid further financial penalties, it is essential to respond immediately by settling the debt or negotiating a payment arrangement.

What is a Notice of Default (NOD) in the pre-foreclosure process?

A Notice of Default is a formal public notification filed by a lender or trustee indicating that a borrower has fallen significantly behind on mortgage payments. It serves as the official beginning of the legal foreclosure process, warning the homeowner that they must resolve the debt to avoid losing their property.

How long do I have to respond after receiving a Notice of Default letter?

The timeline varies by state law, but homeowners typically have a reinstatement period of 90 days following the filing of a Notice of Default. During this pre-foreclosure window, the borrower can stop the foreclosure by paying the past-due balance, including late fees and legal costs, or by negotiating an alternative with the lender.

Can I sell my home if I have received a Notice of Default?

Yes, you can still sell your home during the pre-foreclosure stage after receiving a Notice of Default. Many homeowners opt for a traditional sale if there is equity in the home or a short sale if the home is worth less than the loan balance, as these options are often less damaging to credit scores than a completed foreclosure.

What are the primary differences between a Notice of Default and a Notice of Sale?

A Notice of Default is the initial warning that legal action has started due to non-payment, whereas a Notice of Sale is a subsequent document that sets a specific date, time, and location for the foreclosure auction. The Notice of Default marks the start of pre-foreclosure, while the Notice of Sale signifies the final stage before the property is sold.

What options are available to stop foreclosure after receiving a default letter?

Homeowners have several options to stop the process, including mortgage reinstatement (paying the full arrears), a loan modification to adjust terms, a repayment plan, or a forbearance agreement. If keeping the home is not feasible, options like a short sale or a deed-in-lieu of foreclosure can help mitigate the impact on the borrower's financial future.

Comments