An Agency Request for Underwriting Reconsideration is a formal appeal submitted when an insurance carrier issues a non-renewal notice. This process allows agents to present new information, clarify risk improvements, or rectify misunderstandings to maintain coverage for their clients. Proactive communication is essential to reversing unfavorable decisions. To assist your advocacy efforts, below are some ready to use templates.

Image cover: Winning Appeals: Agency Templates and Samples for Underwriting Reconsideration of Non-Renewals

Letter Samples List

- Letter Requesting Reconsideration Due to Completed Property Repairs

- Letter Highlighting Implementation of New Loss Control Measures

- Letter Emphasizing Favorable Long-Term Agency and Insured Relationship

- Letter Addressing and Mitigating Prior Claims Frequency

- Letter Clarifying Changes in Business Operations and Risk Profile

- Letter Providing Proof of Updated Management and Safety Protocols

- Letter Disputing Inaccurate Inspection Report Findings

- Letter Requesting Reconsideration Based on Increased Deductible Acceptance

- Letter Demonstrating Correction of Prior Administrative Deficiencies

- Letter Proposing Reduced Coverage Limits for Renewal Approval

- Letter Appealing Non-Renewal Due to Isolated Severe Weather Losses

- Letter Presenting New Risk Management Training Certification

- Letter Requesting Underwriting Exception for High-Value Commercial Account

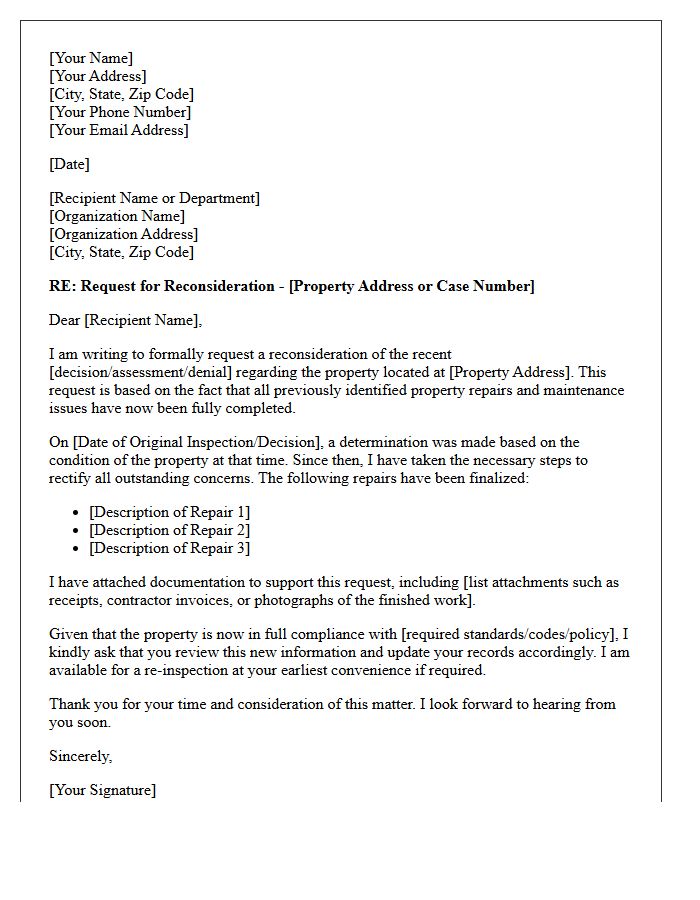

Letter Requesting Reconsideration Due to Completed Property Repairs

A letter requesting reconsideration due to completed property repairs is essential for updating your property valuation or insurance status. This formal document notifies assessors or lenders that previously noted defects are resolved, potentially lowering tax assessments or improving loan terms. You must include itemized receipts, building permits, and before-and-after photographs to substantiate the improvements. Clearly state how these specific repairs enhance the property's safety and market value. Timely submission ensures your records accurately reflect the current condition of your real estate asset, protecting your financial interests through verified maintenance compliance.

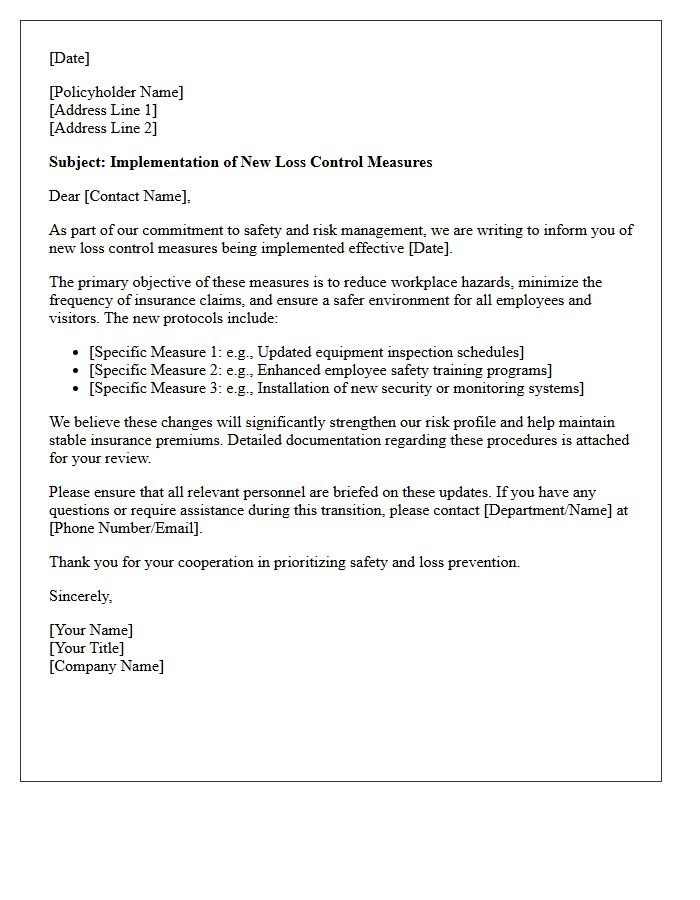

Letter Highlighting Implementation of New Loss Control Measures

The Letter Highlighting Implementation for new loss control measures signifies a strategic shift in risk management protocols. This system uses visual cues to prioritize critical safety data, ensuring stakeholders immediately identify high-risk areas. By emphasizing specific text, organizations can streamline corrective actions and improve compliance oversight. This method reduces cognitive load, allowing safety officers to focus on mitigation strategies that prevent financial and operational losses. Understanding these markers is essential for maintaining robust safety standards and achieving long-term organizational resilience through proactive hazard identification.

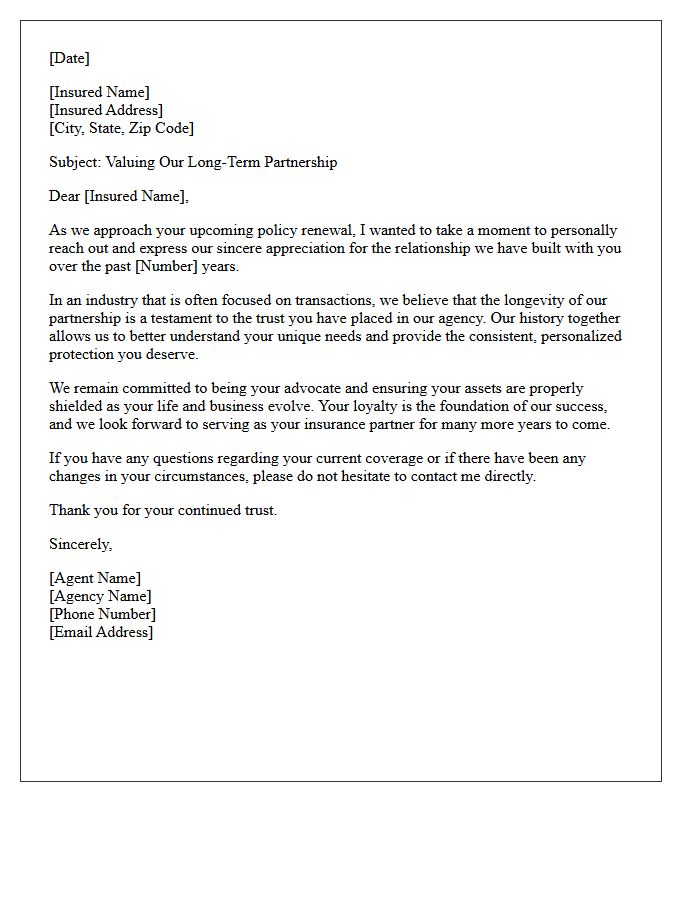

Letter Emphasizing Favorable Long-Term Agency and Insured Relationship

A letter emphasizing a favorable long-term agency and insured relationship serves as a vital tool for policy retention. It acknowledges the history of trust and loyalty established between the parties, reinforcing the value of professional guidance. Highlighting this enduring partnership can lead to preferential underwriting considerations and improved renewal terms. By documenting a consistent track record of reliability, the agency demonstrates its commitment to the client's ongoing protection, fostering mutual stability and securing future growth within a competitive insurance market through personalized advocacy and dedicated service.

Letter Addressing and Mitigating Prior Claims Frequency

Accurate letter addressing is essential for optimizing logistics and reducing operational errors. Precise delivery data directly mitigates prior claims frequency by ensuring mail reaches intended recipients without delays or misrouting. Implementing standardized formatting and verifying zip codes minimizes return-to-sender incidents and financial losses. Consistent data hygiene practices protect sender reputation and enhance customer trust. By prioritizing address integrity, organizations streamline distribution networks and effectively lower the volume of insurance or service claims associated with lost correspondence.

Letter Clarifying Changes in Business Operations and Risk Profile

A letter clarifying changes in business operations and risk profile is a formal disclosure sent to financial institutions or stakeholders. It highlights significant shifts in operational scope, such as new revenue streams, geographic expansion, or ownership changes. Providing accurate details ensures compliance with Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations. Transparent reporting helps maintain banking relationships by allowing institutions to reassess risk levels accurately. Timely communication prevents account freezes and ensures your business profile reflects current activities, mitigating potential regulatory non-compliance risks and maintaining financial trust.

Letter Providing Proof of Updated Management and Safety Protocols

A letter providing proof of updated management and safety protocols serves as official verification that an organization complies with current regulatory standards. This document highlights enhanced operational procedures and risk mitigation strategies to ensure the well-being of employees and clients. It is essential for building trust with stakeholders, securing insurance, and maintaining compliance during audits. By detailing specific improvements in oversight and emergency response, the letter demonstrates a proactive commitment to workplace safety and professional accountability in an evolving regulatory landscape.

Letter Disputing Inaccurate Inspection Report Findings

A formal dispute letter is essential for correcting errors in a property or vehicle assessment. You must clearly identify each inaccurate finding and provide objective evidence, such as photos or repair receipts, to support your claims. Submit the document via certified mail to ensure a legal paper trail. Formally challenging these discrepancies protects your financial interests and ensures the final inspection report reflects the true condition of the asset. Acting quickly is vital, as most agencies enforce strict deadlines for filing a formal disagreement regarding their initial results.

Letter Requesting Reconsideration Based on Increased Deductible Acceptance

When drafting a Letter Requesting Reconsideration, your primary goal is to lower insurance premiums by agreeing to a higher deductible. This formal proposal demonstrates your willingness to share more financial risk, which incentivizes the insurer to provide more affordable rates. Clearly state your policy number, the specific deductible increase you are accepting, and request a revised quote. This strategy is an effective way to maintain comprehensive coverage while reducing immediate monthly costs through a proactive premium adjustment request.

Letter Demonstrating Correction of Prior Administrative Deficiencies

A Letter Demonstrating Correction of Prior Administrative Deficiencies is a formal document used to verify that compliance gaps or procedural errors identified during an audit have been rectified. It serves as official evidence that an organization has implemented corrective actions to meet regulatory standards. This letter is essential for restoring good standing, mitigating legal risks, and preventing future penalties. By clearly outlining the improvements made, it demonstrates accountability and a commitment to operational integrity, ensuring that administrative processes now align with mandatory governance requirements.

Letter Proposing Reduced Coverage Limits for Renewal Approval

When an insurer issues a renewal approval contingent on a reduction of coverage limits, it signifies a shift in risk assessment. This formal proposal often occurs due to increased claims history or changing market conditions. Policyholders must carefully evaluate these lower liability thresholds to ensure they maintain adequate financial protection. Reviewing the premium adjustments alongside decreased limits is essential before formal acceptance, as it directly impacts your overall indemnity safety net and potential out-of-pocket exposure during future claims.

Letter Appealing Non-Renewal Due to Isolated Severe Weather Losses

When drafting a letter appealing non-renewal, emphasize that claims were strictly caused by isolated severe weather events beyond your control. Clearly document that these losses are non-recurring and not indicative of a high-risk property profile. Provide evidence of any mitigation efforts or repairs made to prevent future damage. Since catastrophic weather is often classified differently than negligence-based claims, highlight your long-term policyholder loyalty and request a formal underwriting reconsideration to maintain your essential coverage and protect your property's insurability.

Letter Presenting New Risk Management Training Certification

This official letter announces the launch of our Risk Management Training Certification, a program designed to enhance organizational resilience. Candidates will gain expertise in proactive threat assessment and mitigation strategies. This credential validates your ability to navigate complex regulatory landscapes and minimize operational vulnerabilities. Completion of this course ensures that professionals remain compliant with evolving global standards. We invite you to enroll today to elevate your professional profile and strengthen your company's strategic security framework through comprehensive, industry-recognized expertise and risk governance excellence.

Letter Requesting Underwriting Exception for High-Value Commercial Account

When drafting a letter requesting an underwriting exception for a high-value commercial account, focus on risk mitigation. Clearly articulate the account's long-term profitability, exceptional loss history, and strategic importance. Provide specific evidence or compensating factors that justify deviating from standard guidelines, such as enhanced safety protocols or superior financial stability. A persuasive, data-driven narrative demonstrates that the policy represents a calculated risk rather than a standard non-compliance issue. Professional transparency and strong supporting documentation are essential to securing approval from senior decision-makers in the insurance hierarchy.

What is an Agency Request for Underwriting Reconsideration of Non-Renewal?

It is a formal appeal submitted by an insurance agency to an underwriting department, providing new information or evidence to challenge a carrier's decision to terminate a policy at its expiration date.

What supporting documentation is needed for a non-renewal reconsideration?

Effective requests should include proof of hazard mitigation (such as photos of repairs), updated loss control reports, a "no loss" letter if applicable, or evidence of significant improvements in the insured's risk profile.

How long does the underwriting department have to respond to a reconsideration request?

While timelines vary by carrier, most underwriting departments aim to provide a formal decision within 5 to 10 business days, depending on the complexity of the risk and the proximity to the policy expiration date.

Can a non-renewal be reversed if the reason was a high loss ratio?

Yes, underwriters may reconsider if the agency demonstrates that the losses were non-recurring "shock losses" and that the insured has implemented new safety protocols or increased their deductible to prevent future claims.

What are the most common reasons an underwriting reconsideration is approved?

Approvals typically occur when the agency proves the initial non-renewal was based on outdated data, when a required inspection has been successfully completed, or when the policyholder has corrected specific underwriting concerns.

Comments