A Letter of Instruction to Probate Referee is a formal document used by executors to request a professional appraisal of non-cash estate assets. This essential step ensures accurate valuations for court filings and tax purposes, streamlining the probate administration process. To simplify your legal requirements and ensure all necessary data is included, below are some ready to use template.

Image cover: Formal Templates and Samples: Drafting Your Letter of Instruction to the Probate Referee

Letter Samples List

- Letter of Instruction to Probate Referee for Real Property Appraisal

- Letter of Instruction to Probate Referee for Business Interest Valuation

- Expedited Letter of Instruction to Probate Referee

- Letter of Instruction to Probate Referee for Safe Deposit Box Inventory

- Supplemental Letter of Instruction to Probate Referee

- Letter of Instruction to Probate Referee for Tangible Personal Property

- Amended Letter of Instruction to Probate Referee for Corrected Inventory

- Letter of Instruction to Probate Referee for Partial Inventory and Appraisal

- Letter of Instruction to Probate Referee Regarding Promissory Notes

- Letter of Instruction to Probate Referee for Out of County Assets

- Letter of Instruction to Probate Referee for Trust Asset Appraisal

- Letter of Instruction to Probate Referee Regarding Disputed Assets

- Final Letter of Instruction to Probate Referee for Estate Closure

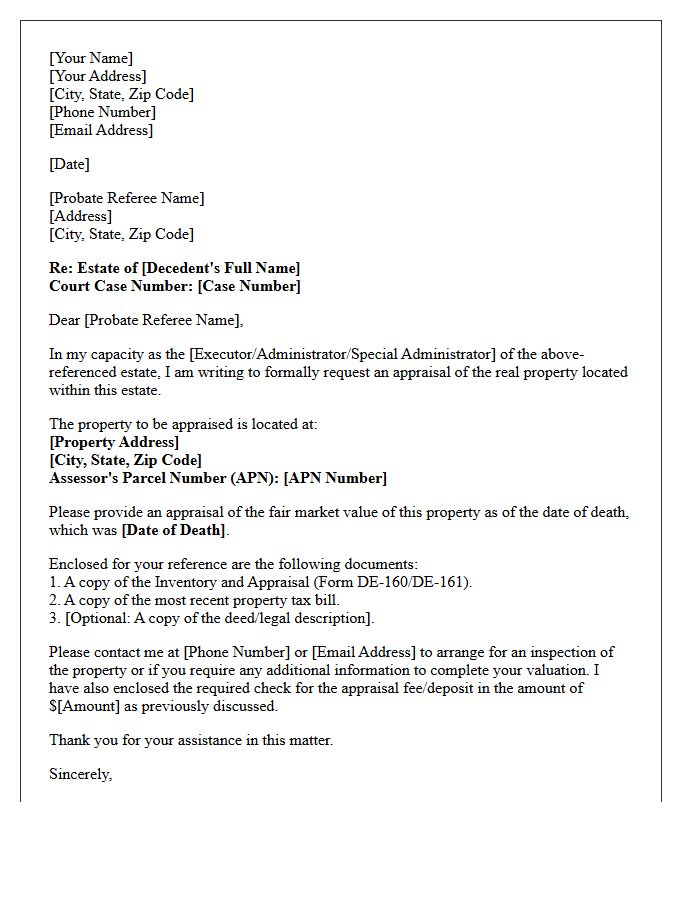

Letter of Instruction to Probate Referee for Real Property Appraisal

A Letter of Instruction is a vital legal document used to request an official inventory and appraisal of real estate during estate administration. You must provide the Probate Referee with the property address, legal description, and the decedent's date of death to ensure an accurate fair market value assessment. This valuation is essential for calculating inheritance taxes, establishing a new cost basis, and obtaining court approval for potential sales. Precise documentation prevents delays in the probate process and ensures compliance with state court requirements and tax regulations.

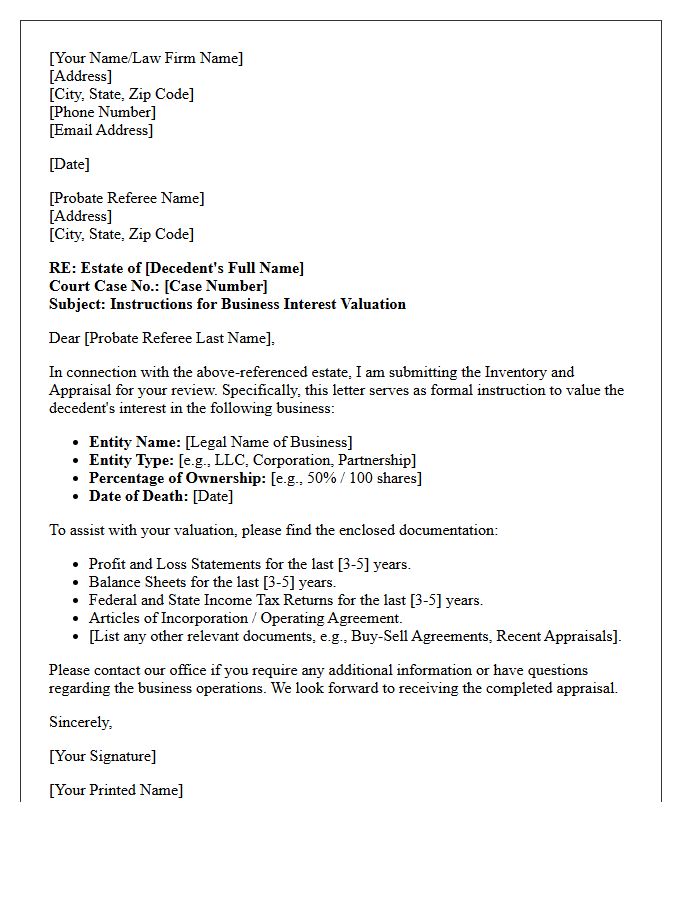

Letter of Instruction to Probate Referee for Business Interest Valuation

A Letter of Instruction provides the Probate Referee with essential details to perform an accurate Business Interest Valuation. It must include the legal name, ownership percentage, and tax returns for the past five years. Clearly stating the date of death ensures the appraisal reflects the fair market value at the time of passing. Providing comprehensive financial statements, buy-sell agreements, and asset lists helps avoid delays in the probate process. Precise documentation is vital for determining the estate's total worth and ensuring compliance with court requirements and potential inheritance tax assessments.

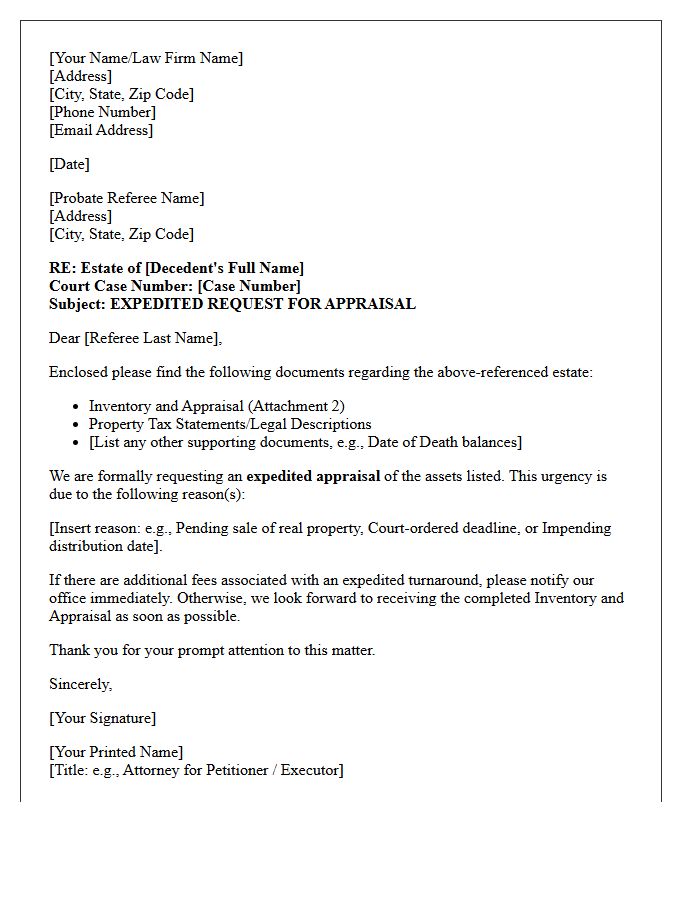

Expedited Letter of Instruction to Probate Referee

An Expedited Letter of Instruction is a formal request sent to a court-appointed Probate Referee to prioritize the appraisal of estate assets. This process is essential for meeting tight legal deadlines or facilitating a real estate sale. By providing clear documentation and valuation data quickly, the personal representative can reduce administrative delays. Timely appraisals are critical to obtaining the Inventory and Appraisal form, ensuring the probate case moves forward efficiently toward final distribution and closure.

Letter of Instruction to Probate Referee for Safe Deposit Box Inventory

A Letter of Instruction authorizes a Probate Referee to perform a formal appraisal of assets. When dealing with a Safe Deposit Box, this document specifies the bank location and box number, granting the referee legal entry to list and value all contents. This step is essential for accurately filing the Inventory and Appraisal form with the court. Ensuring all items are documented prevents disputes and establishes the date-of-death value necessary for tax purposes and the legal distribution of the decedent's estate assets.

Supplemental Letter of Instruction to Probate Referee

A Supplemental Letter of Instruction provides the Probate Referee with specific details required to accurately value non-cash assets. It acts as a formal guidance document, ensuring the appraiser understands unique property characteristics, pending improvements, or encumbrances. Providing clear descriptions and supporting documentation helps avoid valuation errors and prevents costly delays in the probate process. Precise information ensures a more defensible appraisal for tax filings and final estate distribution within the court system.

Letter of Instruction to Probate Referee for Tangible Personal Property

A Letter of Instruction to a Probate Referee is a formal document used in estate administration to request a professional appraisal of non-cash assets. For tangible personal property, such as jewelry, art, or vehicles, this letter provides the necessary descriptions and locations to ensure an accurate fair market value assessment. Properly listing these items is essential for completing the Inventory and Appraisal form required by the court. Providing detailed information helps avoid delays in the distribution of assets and ensures compliance with state probate codes and tax requirements.

Amended Letter of Instruction to Probate Referee for Corrected Inventory

An Amended Letter of Instruction is essential when a Corrected Inventory and Appraisal is required due to initial valuation errors or omitted assets. This formal document directs the Probate Referee to reassess specific items, ensuring the court record reflects the estate's true fair market value. Providing precise documentation, such as updated financial statements or property descriptions, facilitates an accurate revaluation process. Timely submission is critical to maintain legal compliance and ensure the equitable distribution of assets among heirs during the probate proceedings.

Letter of Instruction to Probate Referee for Partial Inventory and Appraisal

When filing a Letter of Instruction to Probate Referee, you must clearly identify assets for a partial inventory. This legal document directs the court-appointed referee to value specific items, such as real estate or business interests, while excluding cash accounts. Providing precise property descriptions and supporting documentation ensures an accurate appraisal. Timely submission is vital for meeting court deadlines and facilitating the efficient distribution of estate assets. This step allows executors to process portions of the estate valuation incrementally rather than waiting for a complete final filing.

Letter of Instruction to Probate Referee Regarding Promissory Notes

A Letter of Instruction provides the Probate Referee with essential details to accurately value a promissory note within an estate. It must include the unpaid principal balance, interest rate, and payment history. Highlighting any defaults or collateral security is crucial, as these factors significantly impact the note's current fair market value. Proper documentation ensures the Inventory and Appraisal reflects the true financial worth of the debt asset for tax and distribution purposes, preventing legal delays during the probate process.

Letter of Instruction to Probate Referee for Out of County Assets

When handling an estate with property outside the primary county, you must submit a formal Letter of Instruction to the appointed probate referee. This document explicitly identifies out-of-county assets that require valuation. It authorizes the primary referee to coordinate with a sub-referee in the secondary jurisdiction to ensure accurate appraisals. Providing precise legal descriptions and parcel numbers is essential for an efficient probate inventory. This coordination prevents valuation delays and ensures the court receives a comprehensive appraisal of all real property and tangible holdings regardless of their physical location.

Letter of Instruction to Probate Referee for Trust Asset Appraisal

A Letter of Instruction is a critical document used to request a formal inventory and appraisal of non-cash assets held within a trust. It provides the Probate Referee with essential details, including property addresses, account descriptions, and the specific date of death. This formal request ensures an accurate valuation for tax purposes and equitable distribution among beneficiaries. Providing clear documentation helps the referee establish the fair market value required to settle the estate efficiently and comply with legal fiduciary duties.

Letter of Instruction to Probate Referee Regarding Disputed Assets

A Letter of Instruction to a Probate Referee is a vital legal document used to clarify the status of disputed assets within an estate. It directs the court-appointed referee to provide a formal appraisal or valuation, even when ownership is contested. This ensures all property is accurately inventoried on the Inventory and Appraisal form. By explicitly identifying items under dispute, the personal representative protects the estate's legal standing, maintains transparency with beneficiaries, and establishes a clear financial baseline essential for resolving litigation or achieving a court-ordered settlement.

Final Letter of Instruction to Probate Referee for Estate Closure

The Final Letter of Instruction to the Probate Referee is a critical document for finalizing an estate. It formally requests a comprehensive inventory and appraisal of all non-cash assets, such as real estate and jewelry. This valuation establishes the date-of-death fair market value required for tax filings and distribution. To avoid delays, ensure all supporting documentation, including property deeds and account statements, is attached. Once the referee completes Form Inventory and Appraisal, the personal representative can proceed with the final accounting to ensure a smooth estate closure.

What is a Letter of Instruction to a Probate Referee?

A Letter of Instruction is a formal document sent by an estate executor or administrator to a court-appointed Probate Referee, providing the necessary data and documentation required to value non-cash estate assets for the inventory and appraisal process.

What information must be included in a Letter of Instruction to a Probate Referee?

The letter should include the decedent's name, date of death, court case number, contact information for the personal representative, and a detailed description of assets such as real estate, business interests, or jewelry that require professional valuation.

When should the Letter of Instruction be sent to the Probate Referee?

The letter should be sent as soon as the personal representative has identified all non-cash assets and the court has issued the "Letters" (Testamentary or Administration) granting the authority to manage the estate.

What supporting documents should accompany a Letter of Instruction?

Accompanying documents typically include a copy of the legal property description (Grant Deed), current property tax bills, recent appraisals (if any), and a completed Inventory and Appraisal form (often Judicial Council Form DE-160).

Why is a Letter of Instruction necessary for the probate process?

It is necessary because it initiates the statutory appraisal process required by law, ensuring that non-cash assets are assigned a fair market value for tax purposes and the final distribution of the estate.

Comments