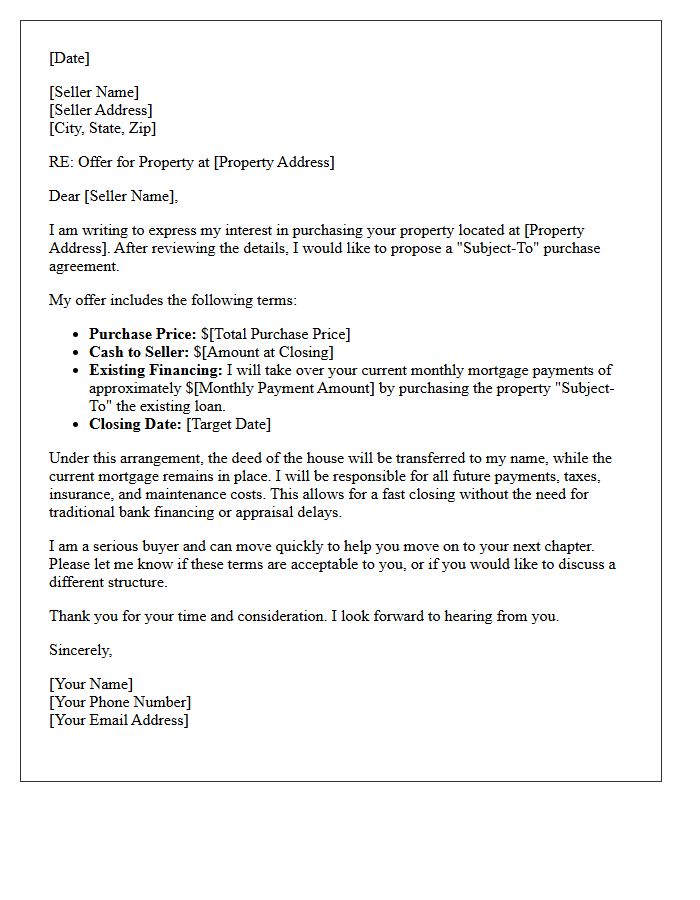

A Subject-to Existing Financing Offer Letter is a formal proposal used by real estate investors to acquire property while keeping the current mortgage in place. This strategy allows you to take over loan payments without needing new bank approvals. Crafting a professional offer is essential for gaining seller trust and securing creative financing deals. Below are some ready to use templates.

Image cover: Winning Subject-To Offer Letter Templates: The Investor's Guide to Professional Financing Proposals

Letter Samples List

- Subject-To Existing Financing Offer Letter Introduction

- Date of Offer Submission

- Seller and Buyer Contact Information

- Subject Property Address and Legal Description

- Total Proposed Purchase Price

- Existing Mortgage Balance Assumption Details

- Monthly Loan Payment and Interest Rate Terms

- Earnest Money Deposit Amount

- Inspection Period and Due Diligence Contingencies

- Closing Date and Escrow Company Information

- Deed Transfer and Risk Acknowledgment

- Formal Expiration Date of Offer

- Buyer and Seller Signature Blocks

Subject-To Existing Financing Offer Letter Introduction

A Subject-To existing financing offer letter introduces a proposal to purchase real estate while keeping the existing mortgage in place. This professional introduction clearly states that the buyer will take over monthly payments without a formal bank assumption. It highlights the seller's relief from debt obligations and ensures a faster closing process. By emphasizing transparency and financial benefits, the letter establishes trust. It serves as a vital tool for creative real estate investors to acquire property with low capital while providing immediate solutions for motivated sellers.

Date of Offer Submission

The Date of Offer Submission is a critical deadline in real estate and procurement cycles. Meeting this specific cutoff time ensures your proposal remains valid for consideration. Missing this date typically results in automatic disqualification, regardless of the bid's quality. It is essential to account for potential technical delays and time zone differences to guarantee your documentation is officially recorded. Timely submission demonstrates professionalism and adherence to contractual requirements, securing your position in the competitive evaluation process.

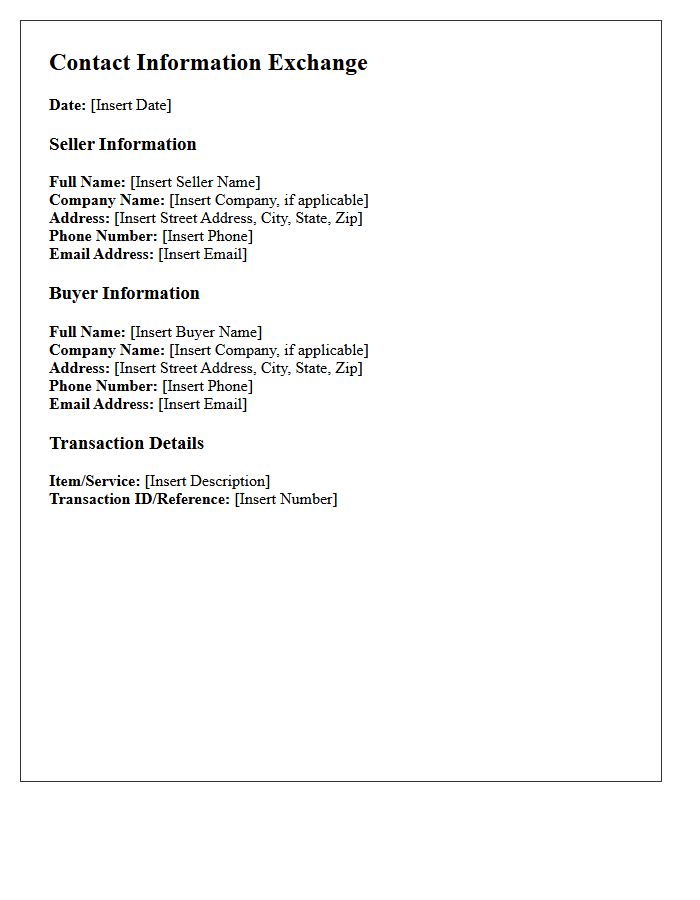

Seller and Buyer Contact Information

In every transaction, accurate Seller and Buyer Contact Information is essential for legal compliance and smooth logistics. This data typically includes full names, verified email addresses, phone numbers, and physical locations. Validating these details prevents identity fraud and ensures that shipping documents or invoices are processed correctly. Maintaining transparent communication channels protects both parties during disputes and builds long-term commercial trust. Always prioritize data privacy by handling sensitive contact details through secure, encrypted platforms to minimize the risk of unauthorized access or information leaks.

Subject Property Address and Legal Description

The Subject Property Address and Legal Description are vital identifiers in real estate. While the address provides a physical location for mail and navigation, the Legal Description is the definitive binding identifier used in court records and deeds. It precisely outlines property boundaries via lot, block, or metes and bounds to prevent ownership disputes. Ensuring both match perfectly on title documents is essential to confirm the exact real estate asset being transferred, as addresses can sometimes be ambiguous or change over time.

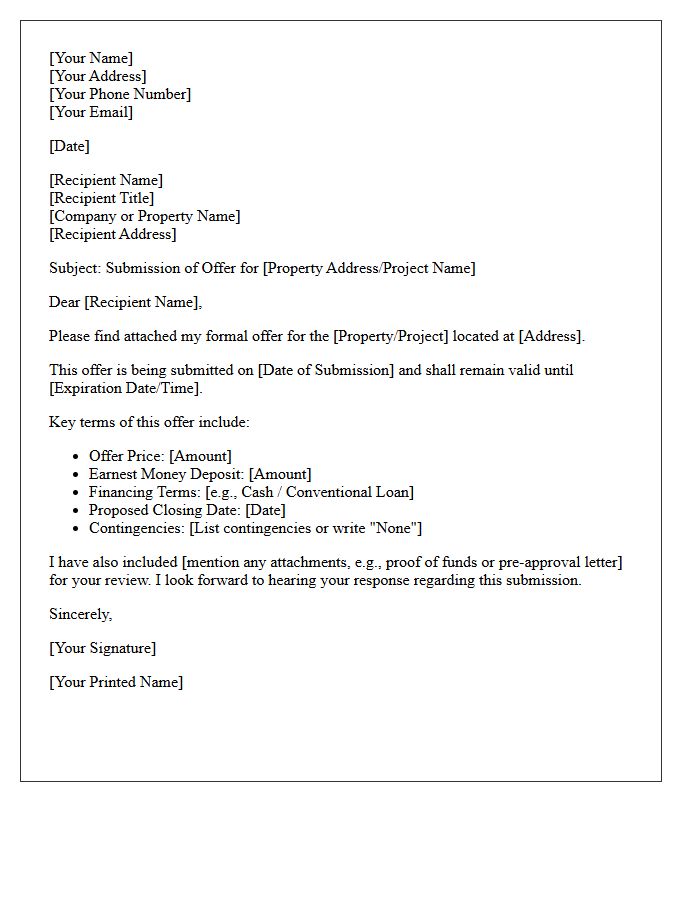

Total Proposed Purchase Price

The Total Proposed Purchase Price represents the comprehensive amount a buyer offers to acquire an asset or business. It is the final valuation that encompasses the base price plus any adjustments, such as debt assumptions or working capital shifts. Understanding this figure is critical during negotiations, as it dictates the financial commitment required and serves as the benchmark for comparing competing bids. Investors must analyze every underlying component to ensure the offer aligns with the actual market value and long-term investment objectives.

Existing Mortgage Balance Assumption Details

A mortgage assumption allows a buyer to take over the seller's existing mortgage balance, including its original terms and interest rate. This process requires lender approval to ensure the buyer meets credit and income requirements. While beneficial in high-rate environments, buyers must often cover the equity gap between the purchase price and the remaining loan balance using cash or a second loan. Most government-backed loans like FHA, VA, and USDA are assumable, whereas conventional loans typically are not due to strict due-on-sale clauses.

Monthly Loan Payment and Interest Rate Terms

Understanding your monthly loan payment requires analyzing the relationship between the principal amount and the interest rate. A higher rate increases the total cost of borrowing and elevates your recurring obligation. Most installment loans use an amortization schedule, ensuring that early payments primarily cover interest while later ones reduce the balance. Terms like APR reflect the true annual cost, including fees. Choosing a shorter repayment term lowers total interest paid but results in a higher monthly commitment, making affordability and rate comparison essential for financial stability.

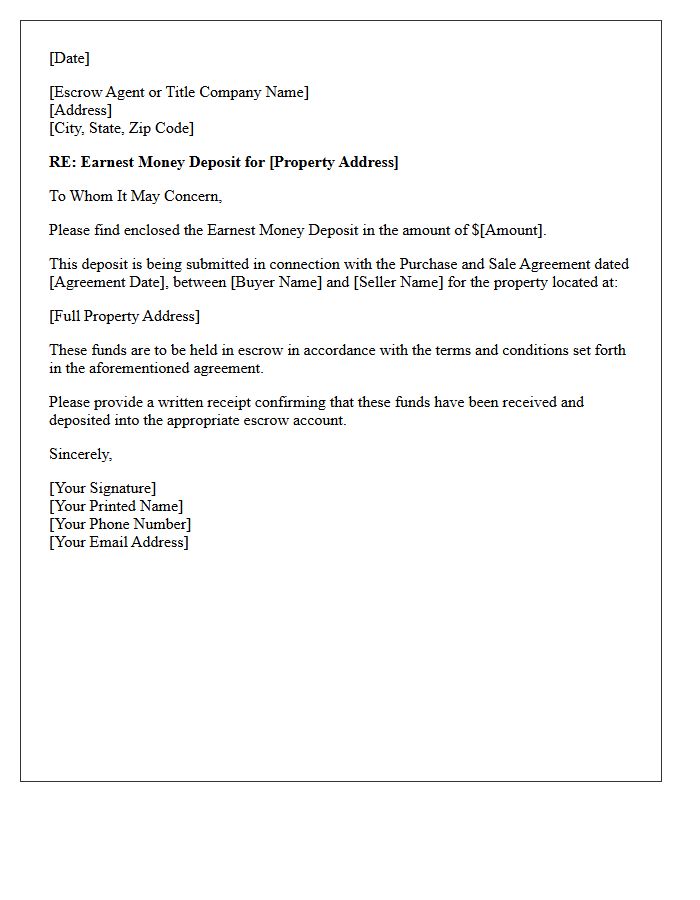

Earnest Money Deposit Amount

The Earnest Money Deposit is a primary indicator of a buyer's commitment to a real estate transaction. Typically ranging from 1% to 3% of the purchase price, this sum acts as "good faith" security held in escrow. A higher amount can make an offer more competitive in multiple-bid situations. It is essential to understand that these funds are credited toward the down payment at closing, but may be forfeited to the seller if the buyer breaches the contract terms without legal justification or contingency protection.

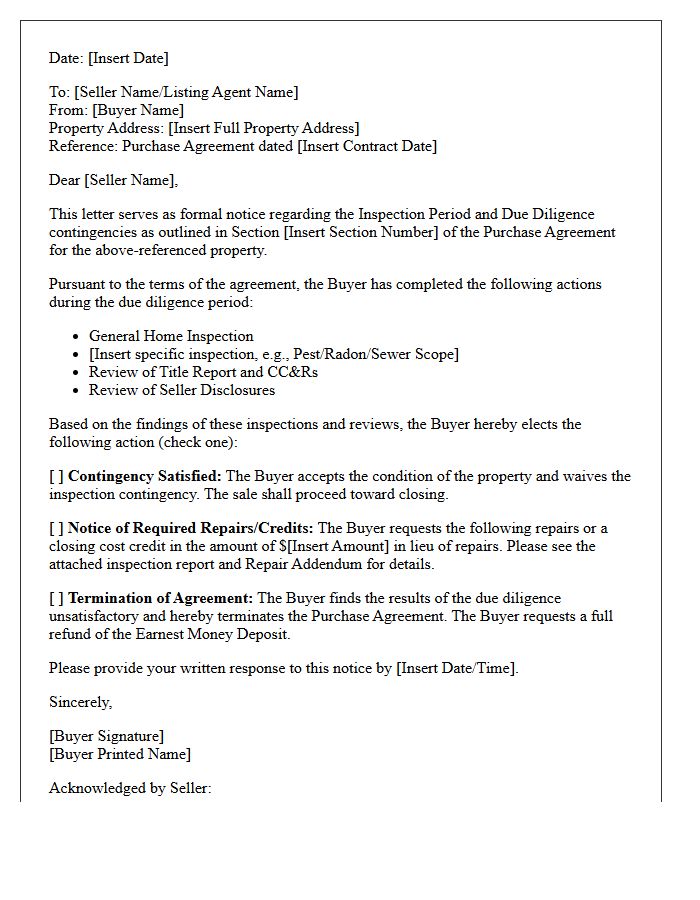

Inspection Period and Due Diligence Contingencies

The Inspection Period is a critical phase in real estate where buyers perform Due Diligence to evaluate a property's condition. During this timeframe, you should hire professionals to uncover structural issues, mold, or mechanical failures. These contingencies provide a legal safety net, allowing the buyer to negotiate repairs, request credits, or cancel the contract without losing their earnest money deposit if significant defects are found. Understanding these deadlines is vital, as failing to act within the specified window typically waives your right to object to the property's physical state.

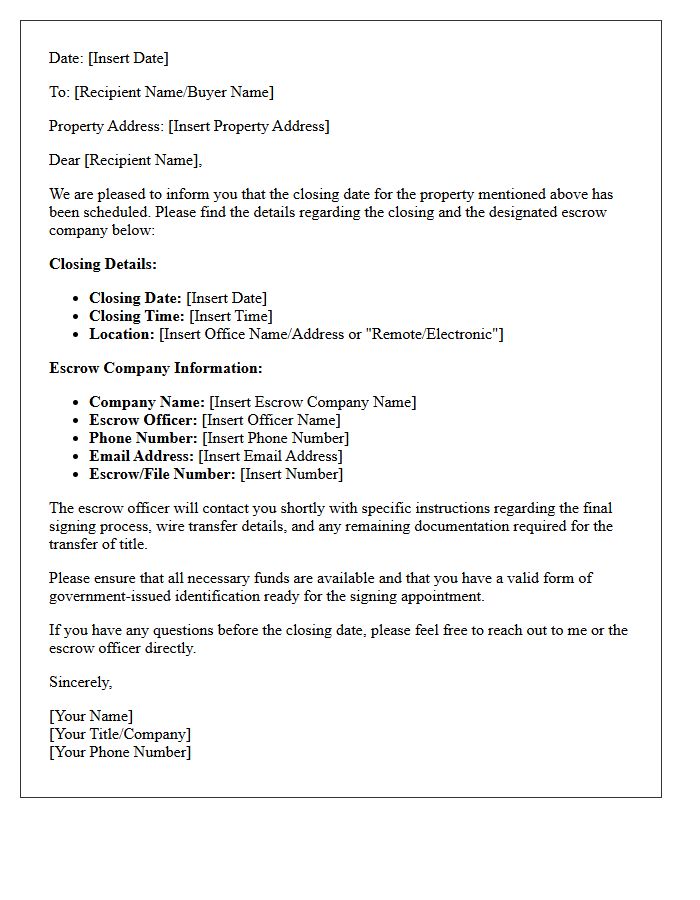

Closing Date and Escrow Company Information

The Closing Date marks the official transfer of property ownership and is legally binding. It is coordinated by the Escrow Company, which acts as a neutral third party to manage funds and documentation. This entity ensures all contractual conditions are met before disbursing payments. Buyers must provide their closing funds via wire transfer or cashier's check as instructed. Timely communication with your escrow officer is essential to prevent processing delays, ensuring a smooth transition and the successful recording of the deed.

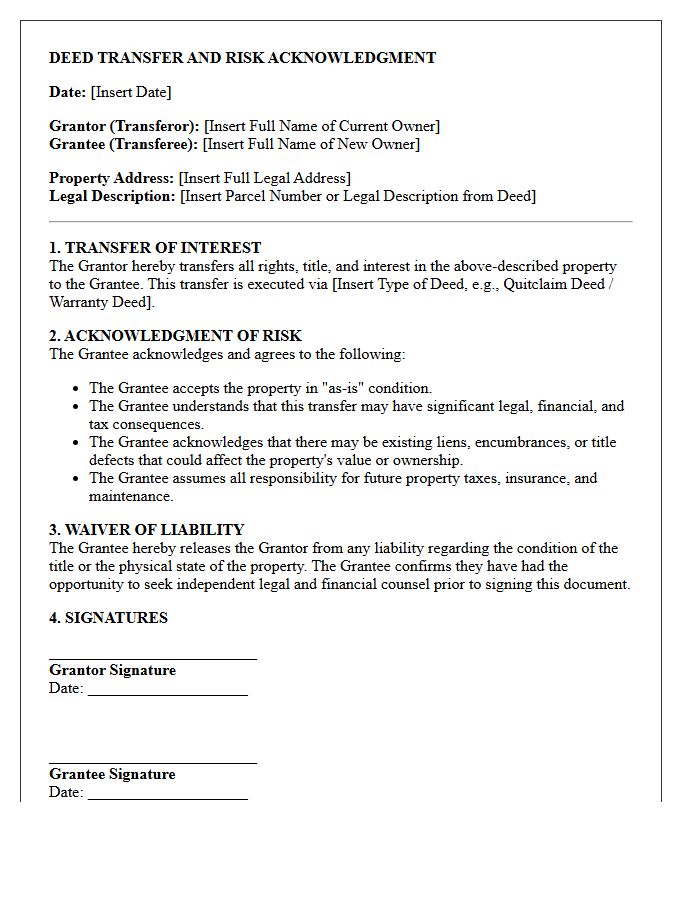

Deed Transfer and Risk Acknowledgment

A Deed Transfer is a legal process that shifts property ownership, often through a quitclaim or warranty deed. It is essential to understand the Risk Acknowledgment involved, as transferring a title can trigger permanent tax implications, impact mortgage "due-on-sale" clauses, and affect title insurance coverage. Before signing, parties must recognize that once recorded, reversing a transfer is difficult and may lead to a loss of control over the asset. Always verify legal descriptions and potential liens to mitigate financial exposure and ensure a secure, valid conveyance of real estate interests.

Formal Expiration Date of Offer

The Formal Expiration Date of Offer represents the legal deadline for a recipient to accept a proposal. Once this precise moment passes, the offer is voided and no longer legally binding. It is critical for both buyers and sellers to track this timeframe, as late acceptance fails to create a valid contract. This date ensures clarity in negotiations, preventing indefinite liability for the offeror. Always verify time zones and specific deadlines to maintain your legal standing and secure potential agreements before the offer permanently lapses.

Buyer and Seller Signature Blocks

The signature block is a legally essential component of a contract that validates the agreement between parties. It must clearly identify the authorized signatories for both the buyer and the seller to ensure enforceability. Key elements include the formal printed name, the specific job title for corporate entities, and the date of execution. Precise formatting prevents future disputes regarding individual liability versus corporate responsibility. Ensuring every field is accurately completed is the final step in establishing a binding commitment and legal accountability for all contractual obligations mentioned within the document.

What is a Subject-to existing financing offer?

A Subject-to existing financing offer is a real estate purchase proposal where the buyer takes over the seller's mortgage payments without formally assuming the loan. The title transfers to the buyer, while the existing financing remains in the seller's name.

Is a Subject-to offer letter legally binding?

Once signed by both the buyer and seller, a Subject-to offer letter becomes a legally binding purchase agreement. It outlines the specific terms of the equity payment, the responsibility for the underlying mortgage, and the closing date.

Does a Subject-to offer require lender approval?

Typically, a Subject-to transaction occurs without formal lender approval. While most mortgages contain a "due-on-sale" clause, the offer letter specifies that the buyer will make payments directly to the servicer or through a third-party escrow company to keep the loan current.

What details should be included in a Subject-to existing financing offer?

The offer should include the purchase price, the current mortgage balance, the monthly payment amount (PITI), the interest rate, the duration of the entry fee or equity payment, and a disclosure regarding the due-on-sale clause.

How does a seller benefit from a Subject-to offer letter?

A Subject-to offer allows a seller to exit a property quickly without paying high closing costs or agent commissions. It is particularly beneficial for sellers with little equity or those who need to stop a foreclosure by having a buyer catch up on arrears and take over future payments.

Comments