A pre-foreclosure negotiation letter is a formal request sent to lenders to discuss alternative repayment options before legal action begins. This essential document helps homeowners propose loan modifications or short sales to avoid losing their property. Crafting a professional proposal can save your credit score and your home. To help you get started, below are some ready to use templates.

Image cover: Proven Pre-Foreclosure Negotiation Letter Samples and Templates

Letter Samples List

- Initial Contact Pre-Foreclosure Inquiry Letter

- Cash Offer Pre-Foreclosure Negotiation Letter

- Short Sale Hardship Explanation Letter

- Notice of Intent to Purchase Pre-Foreclosure Letter

- Urgent Pre-Foreclosure Solution Proposal Letter

- Third-Party Authorization and Negotiation Letter

- Pre-Foreclosure Equity Purchase Offer Letter

- Homeowner Relief and Assistance Negotiation Letter

- Subject-To Assumption Pre-Foreclosure Letter

- Lender Direct Pre-Foreclosure Settlement Letter

- Stop Foreclosure Real Estate Investment Letter

- Pre-Foreclosure Workout Agreement Proposal Letter

Initial Contact Pre-Foreclosure Inquiry Letter

An Initial Contact Pre-Foreclosure Inquiry Letter is a formal notice sent by a lender to a borrower who has missed mortgage payments. This document serves as a preliminary warning before the official legal foreclosure process begins. It outlines the amount past due and provides information on available loss mitigation options. Understanding this letter is crucial because it offers a final opportunity for homeowners to discuss loan modifications or repayment plans. Responding promptly is the most important step to prevent losing your property and to protect your credit score from long-term damage.

Cash Offer Pre-Foreclosure Negotiation Letter

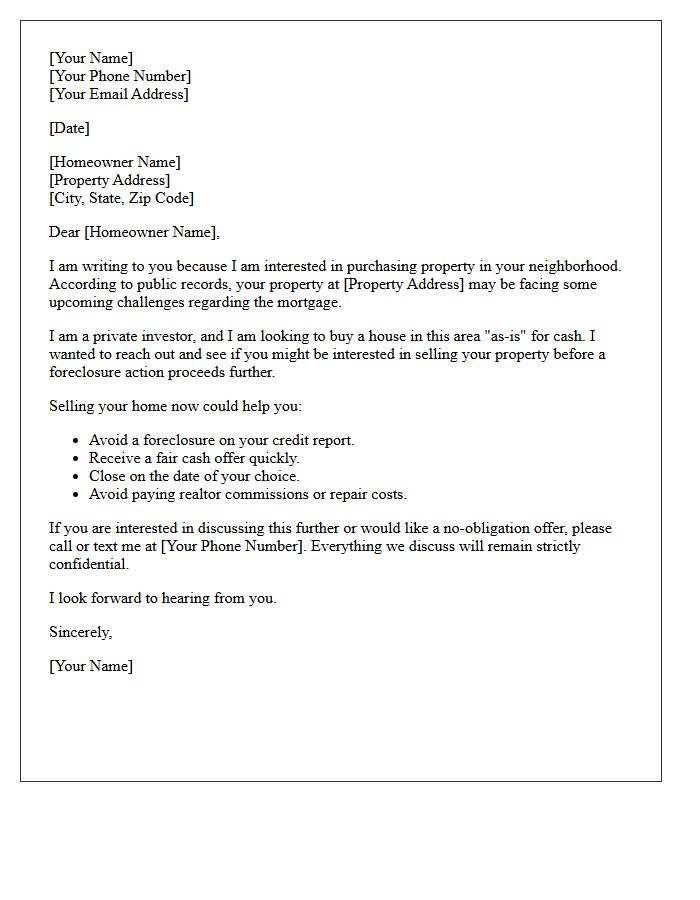

A Cash Offer Pre-Foreclosure Negotiation Letter is a strategic document sent to homeowners facing default. It proposes a quick liquidity solution to stop the legal foreclosure process immediately. The letter must emphasize a fast closing timeline and the ability to purchase the property as-is, removing the burden of repairs. By offering a direct cash buyout, the investor helps the owner avoid a deficiency judgment and permanent credit damage. Clear communication of mutual benefits is essential to successfully negotiating a deed transfer before the bank auctions the home.

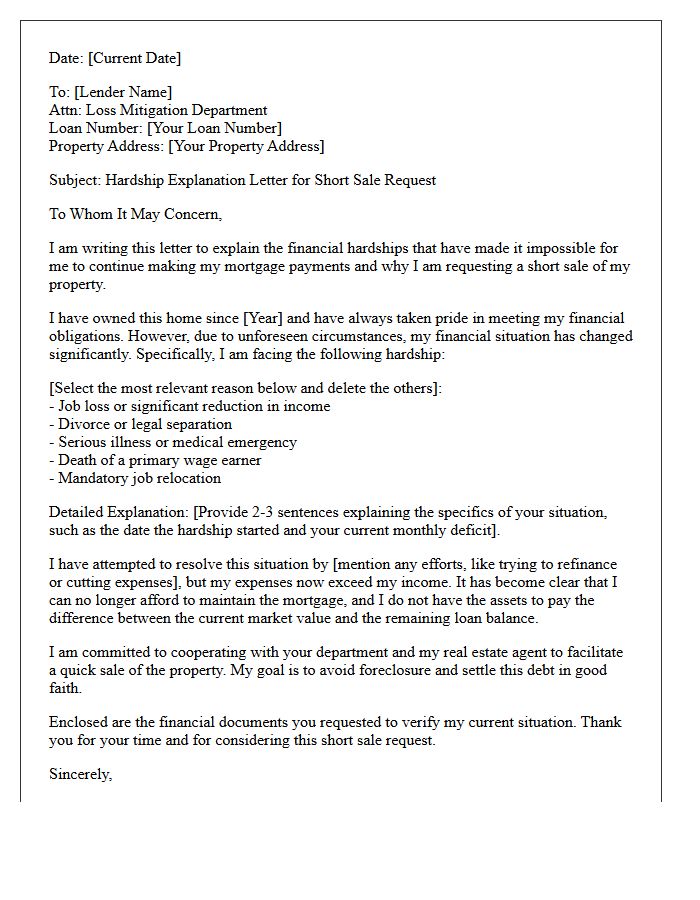

Short Sale Hardship Explanation Letter

A short sale hardship explanation letter is a legal narrative used to persuade lenders to accept a payoff less than the total mortgage balance. To succeed, you must provide a sincere description of your financial distress, such as job loss, medical emergencies, or divorce. It should clearly outline why you can no longer afford monthly payments and emphasize that the situation is permanent. Including specific dates and supporting documentation ensures the lender views your request as a legitimate necessity rather than a strategic default, facilitating smoother approval for the property sale.

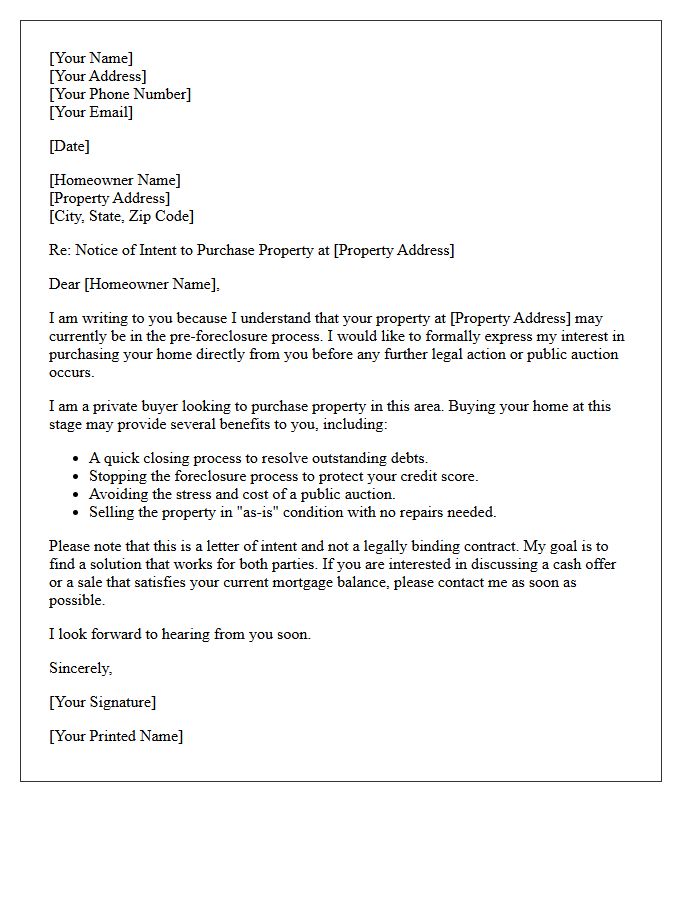

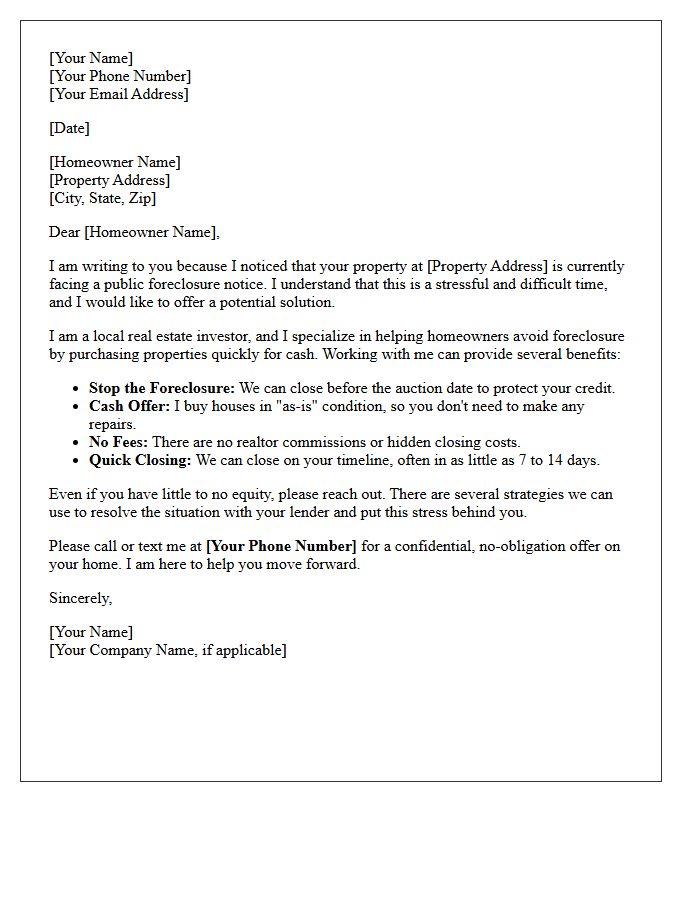

Notice of Intent to Purchase Pre-Foreclosure Letter

A Notice of Intent to Purchase is a strategic formal letter sent to homeowners in pre-foreclosure. This document expresses a professional interest in acquiring the property before a public auction occurs. It provides a distressed seller with a potential exit strategy to avoid a credit-damaging foreclosure entry. For investors, this letter is a vital tool for direct-to-seller marketing, opening negotiations for a private sale. Key components include a clear offer, proof of funds, and a timeline to resolve the mortgage default, offering a mutually beneficial solution for both parties involved.

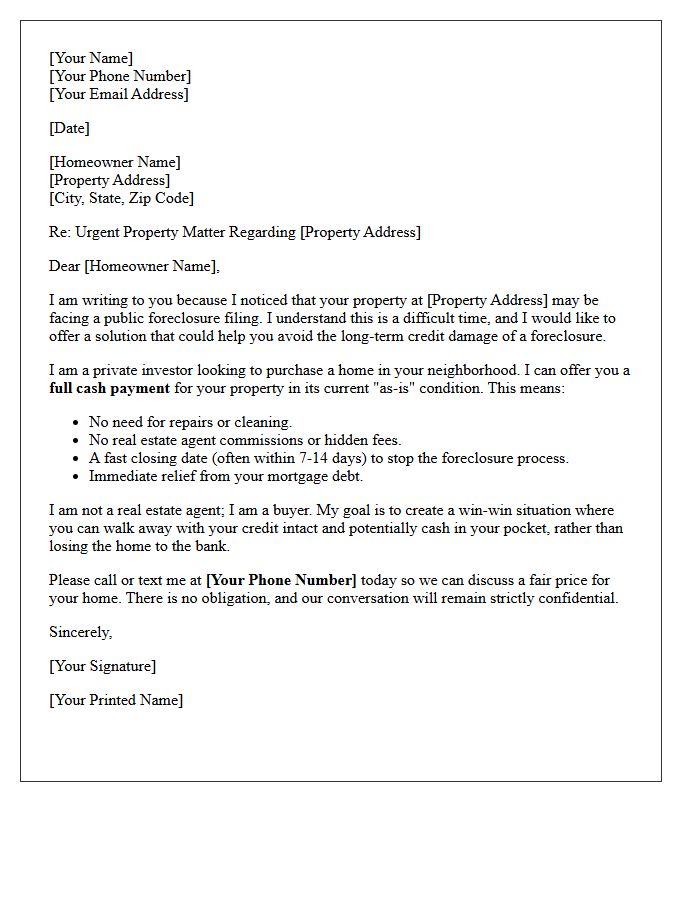

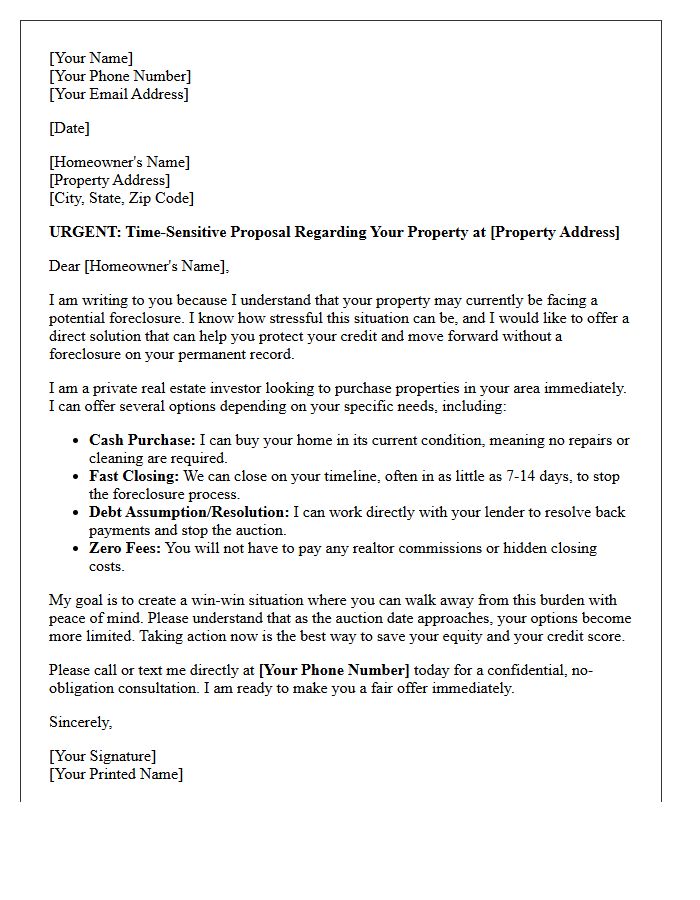

Urgent Pre-Foreclosure Solution Proposal Letter

An Urgent Pre-Foreclosure Solution Proposal Letter is a professional document designed to help homeowners avoid property seizure. Its primary goal is to present a formal request to lenders for a short sale, loan modification, or deed in lieu. This letter must clearly outline the homeowner's financial hardship and provide a viable plan to settle the debt. Acting quickly is essential to halt the foreclosure process, protect credit scores, and secure a mutually beneficial resolution that prevents the total loss of home equity.

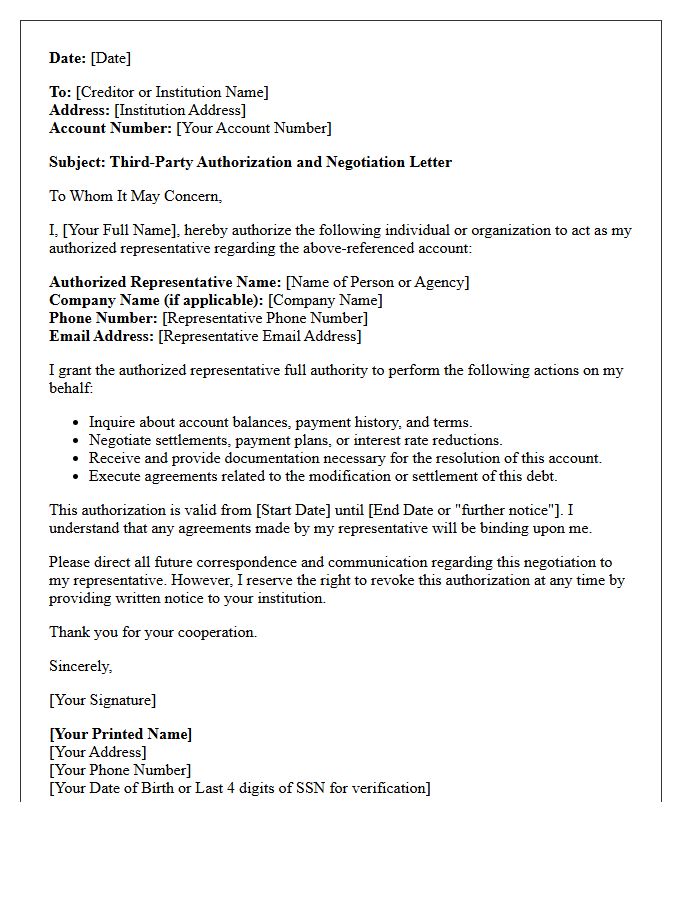

Third-Party Authorization and Negotiation Letter

A Third-Party Authorization and Negotiation Letter is a legal document that permits a designated individual or agency to act on your behalf. This letter of authority grants specific permissions to discuss sensitive account details and settle debts with creditors. It is crucial for debt settlement processes, allowing professional negotiators to reach favorable agreements. By formalizing this representative relationship, you ensure legal compliance and privacy protection while delegating complex financial negotiations. Always define the scope of power clearly to maintain control over final decisions regarding your personal or business liabilities.

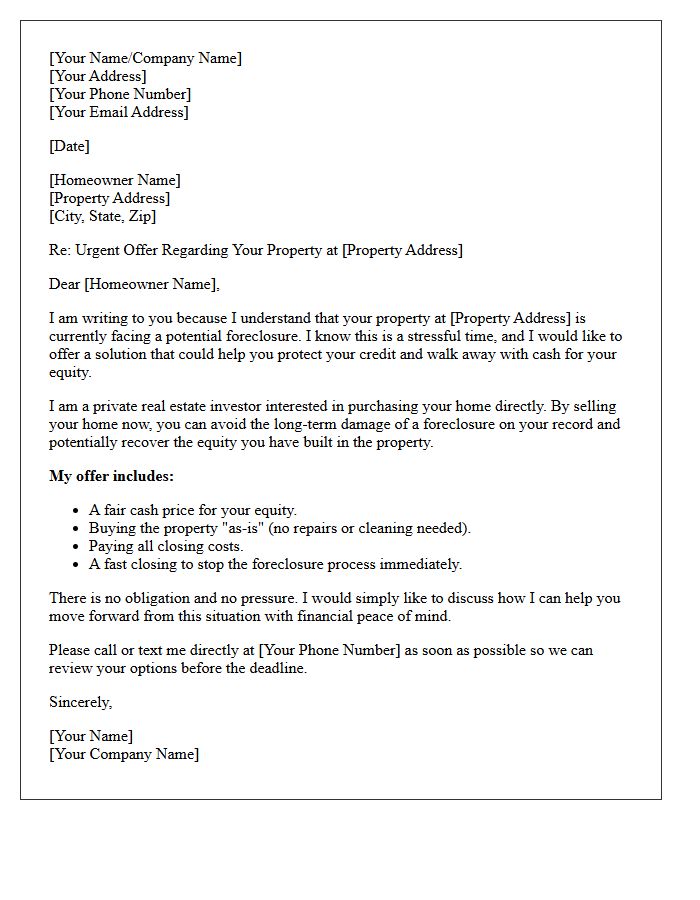

Pre-Foreclosure Equity Purchase Offer Letter

A Pre-Foreclosure Equity Purchase Offer Letter is a formal proposal sent to homeowners facing default. It highlights the opportunity to sell their property before a public auction, allowing them to preserve their credit score and extract remaining cash value. The primary goal is to provide a mutually beneficial solution where the buyer acquires the home at a discount while the seller avoids the legal consequences of a foreclosure judgment. This document must clearly state the offer price, closing timeline, and the intent to resolve outstanding mortgage debts immediately.

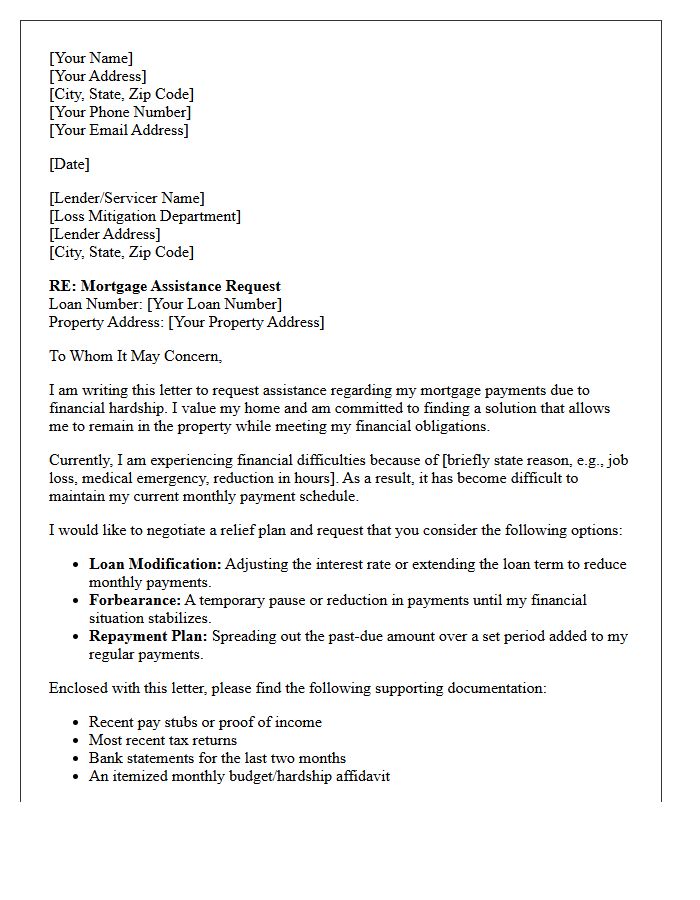

Homeowner Relief and Assistance Negotiation Letter

A Homeowner Relief and Assistance Negotiation Letter is a formal request sent to lenders to modify mortgage terms during financial hardship. The most critical component is the hardship letter, which clearly explains your situation and intent to pay. Highlighting your financial transparency by providing proof of income and expenses is essential for success. This document serves as the foundation for loan modification or forbearance requests. Proactively communicating through this letter helps prevent foreclosure by initiating a legal record of your efforts to find a mutually beneficial repayment solution with your servicer.

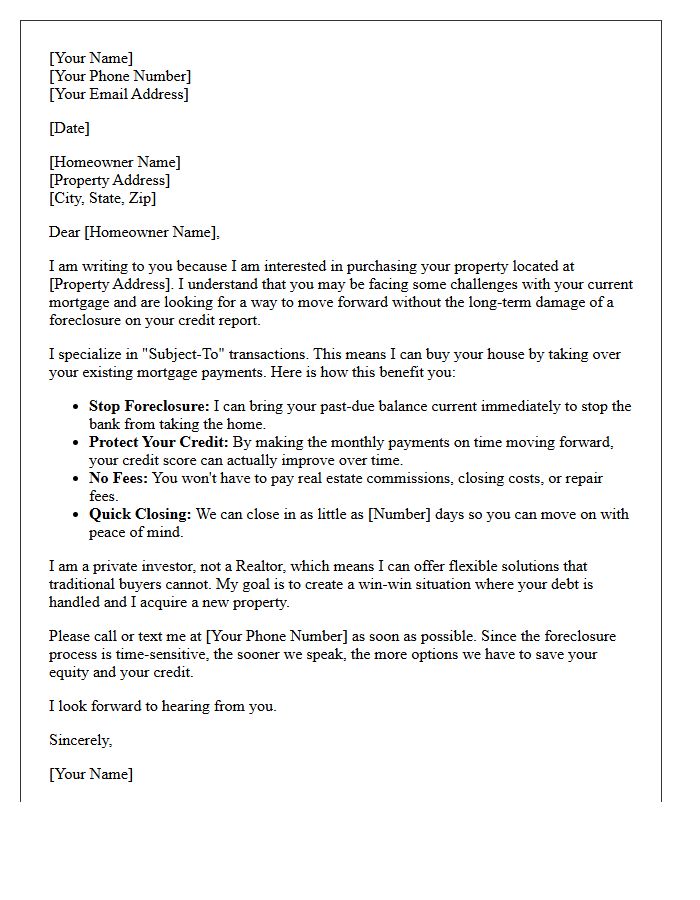

Subject-To Assumption Pre-Foreclosure Letter

A Subject-To Assumption Pre-Foreclosure Letter is a strategic proposal sent to homeowners facing default. It offers to bring the mortgage arrears current and take over future monthly payments while leaving the existing loan in the seller's name. This exit strategy allows the homeowner to avoid a foreclosure mark on their credit report while providing the investor with low-interest financing. It is crucial to address the due-on-sale clause, as lenders may technically accelerate the loan if they discover the title transfer occurred without their formal approval.

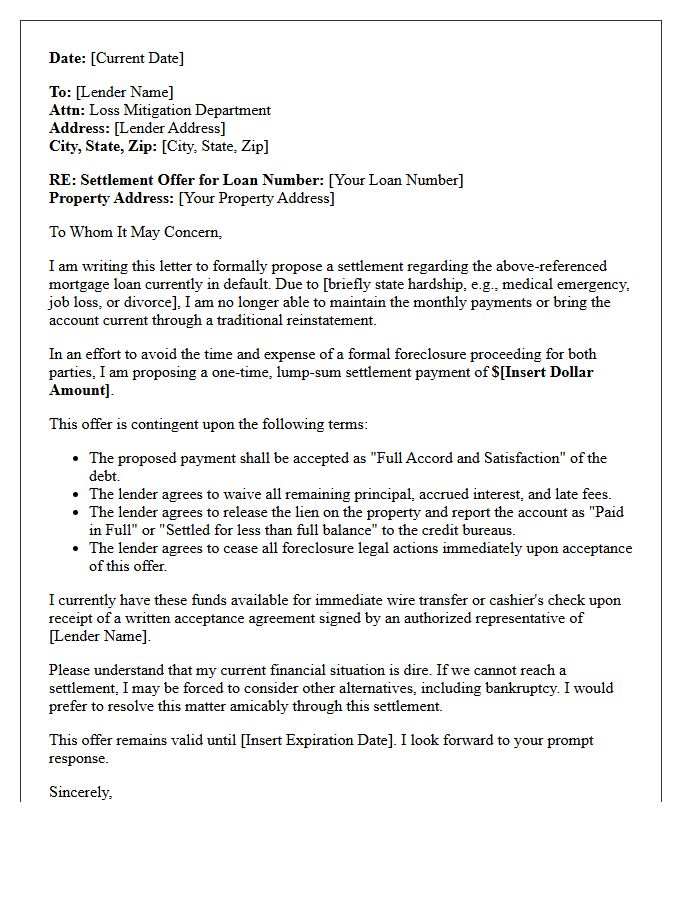

Lender Direct Pre-Foreclosure Settlement Letter

A Lender Direct Pre-Foreclosure Settlement Letter is a formal proposal sent by a homeowner to their mortgage servicer to resolve delinquent debt before a final auction. This document typically requests a short sale or a deed-in-lieu of foreclosure to avoid legal proceedings. It highlights financial hardship and outlines a plan to satisfy the lien, often for less than the total balance. Securing an approval letter in writing is essential to protect your credit and confirm the lender's agreement to waive remaining deficiency balances during the settlement process.

Stop Foreclosure Real Estate Investment Letter

A stop foreclosure real estate investment letter is a professional outreach tool used to connect with distressed homeowners facing legal action. The primary goal is to offer a mutually beneficial solution, such as a cash offer or short sale, before an auction occurs. To be effective, the content must be empathetic, urgent, and clearly explain how the investor can provide immediate financial relief. Highlighting benefits like credit protection and a quick closing process is essential to building trust and securing a profitable property acquisition in a competitive market.

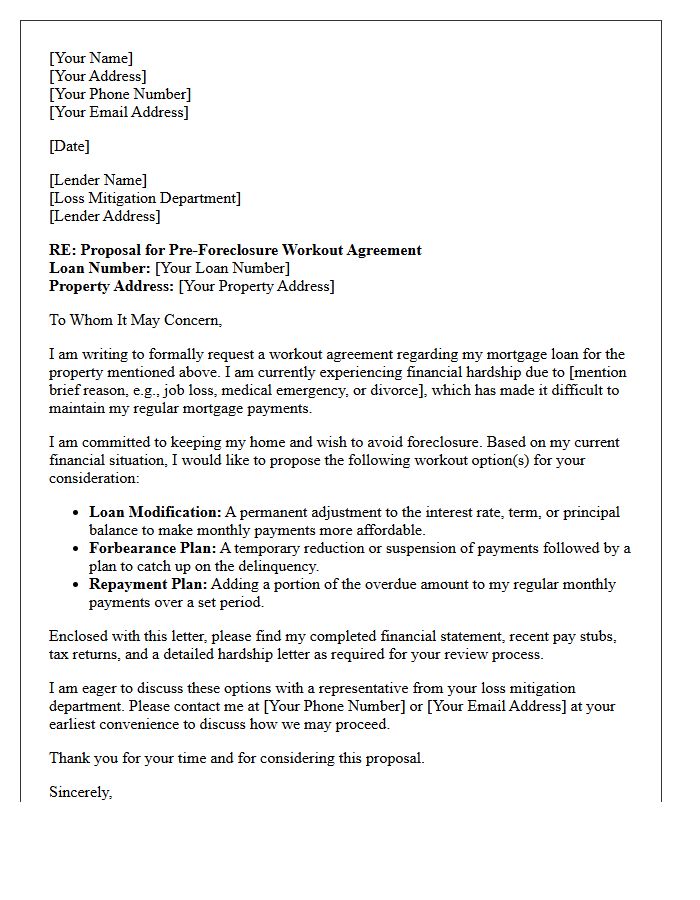

Pre-Foreclosure Workout Agreement Proposal Letter

A Pre-Foreclosure Workout Agreement Proposal Letter is a formal request sent to a mortgage lender to prevent foreclosure. This document outlines your financial hardship and proposes specific alternatives, such as a loan modification, short sale, or repayment plan. Providing clear evidence of your ability to sustain future payments is essential for approval. A well-structured proposal serves as a vital negotiation tool, helping homeowners reach a mutually beneficial agreement with the bank to save their credit and retain property ownership before legal proceedings finalize.

What is a pre-foreclosure negotiation letter?

A pre-foreclosure negotiation letter is a formal written proposal sent by a homeowner to their mortgage lender requesting an alternative to foreclosure, such as a loan modification, short sale, or deed-in-lieu, to resolve a payment delinquency.

When should I send a negotiation letter to my mortgage lender?

You should send a negotiation letter as soon as you receive a notice of default or realize you can no longer meet your monthly mortgage obligations. Early communication increases the likelihood of the lender approving a workout option before the formal foreclosure process concludes.

What key information should be included in a pre-foreclosure hardship letter?

The letter should include your loan account number, a detailed explanation of your financial hardship (such as job loss or medical emergency), proof of income, and a specific request for a loss mitigation option like a repayment plan or principal reduction.

Can a negotiation letter stop the foreclosure process?

While sending a letter does not automatically stop legal proceedings, it often initiates "dual tracking" protections or a formal review process where the lender may voluntarily pause the foreclosure sale while evaluating your application for a loan workout.

What are the most common outcomes of a pre-foreclosure negotiation?

Successful negotiations typically result in a loan modification to lower monthly payments, a forbearance agreement to temporarily pause payments, or a short sale approval, which allows the homeowner to sell the property for less than the remaining mortgage balance.

Comments